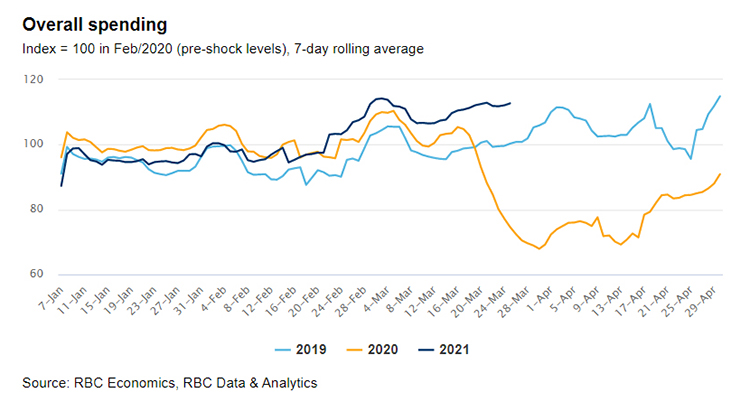

- Overall spending continued to improve in March. Year-over-year comparisons are now being heavily influenced by exceptionally weak spending a year ago, but overall spending is still tracking ~2% above February levels on a seasonally adjusted basis by our count.

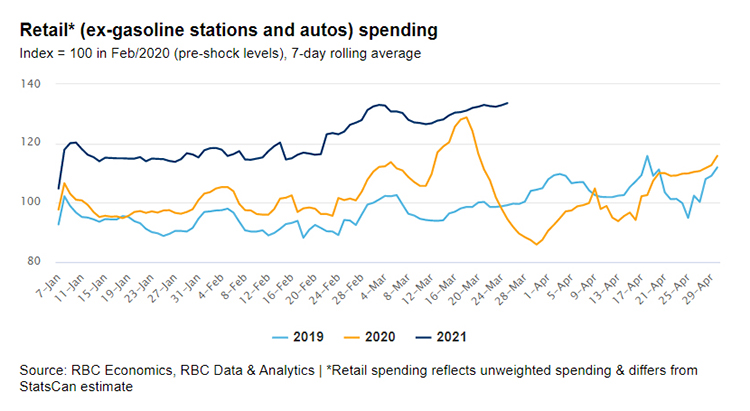

- Spending on retail products continued to edge higher – the data is consistent with another economy-wide increase in retail spending in March, albeit likely smaller than the 4% bounce-back in retail spending Statistics Canada already reported for February.

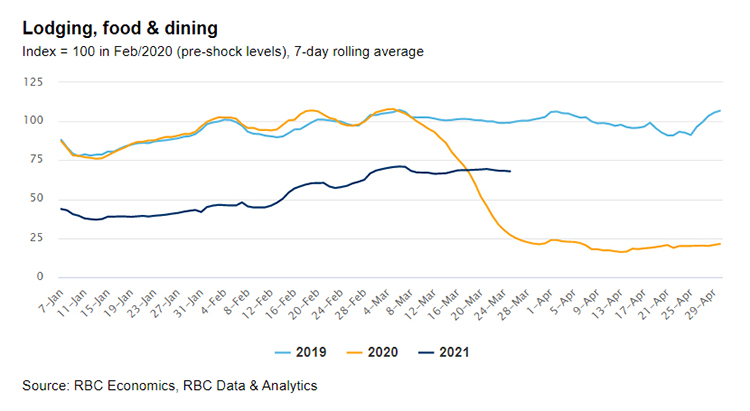

- Early indicators pointed to some recovery in the hard hit food and accommodation sectors as containment measures eased. Notwithstanding, there is still a huge spending shortfall in these sectors and we continue to expect that this deficit will not be eliminated until vaccines are distributed to the broader Canadian population.

- Growing optimism among consumers led to broad based increase in spending. Notably entertainment spending and clothing continues to show upward trends.

- Virus resurgence has prompted some regions to re-impose containment measures that will once again weigh particularly on spending in the hospitality sector in April. But vaccine distribution is also ramping up, and that is expected to pave the way for less restrictions and more household spending in those hardest-hit sectors over the summer.

To view past reports, please visit the COVID Consumer Spending Tracker.

RBC’s consumer spending tracking report uses RBC Data & Analytics’ proprietary database of anonymized card transactions by Canadian clients. The data are an accounting of merchant transactions that are divided into various spending categories covering tens of millions of weekly card transactions worth billions of dollars each week. Transactions, both in person and online, are classified into 11 broad spending groups: Dining, Education, Finances, Groceries, Health, Household, Shopping, Transport, Travel, Utilities, and Other. Within each group, the data are further classified: for example, shopping covers merchants classified as clothing stores, hobby shops, electronics stores, and jewellers, among others. We exclude purely financial transactions such as cash advances and insurance from spending.

We examined changes in the value of all transactions in these areas for 7-day periods starting January 1st, comparing spending to the same period one year ago. To examine the impact of important events, we looked at how spending changed on specific days, both on a daily basis and on an annualized basis relative to that same weekday a year ago.

Online spending volumes are estimated based on the presence of an RBC card at the time of the authorization. Pre-COVID averages are calculated as the average of the first 11 weeks of 2020, and post-COVID averages are averages of subsequent weeks.

Protecting your privacy and safeguarding your personal information is a cornerstone of our organizational ethics and values and will always be one of our highest priorities. The underlying data for this analysis was aggregated based on transaction date, region and merchant category, and cannot be used to identify any individual client or merchant. For additional information please visit www.rbc.com/privacy.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.