Deep dive: How to monitor U.S. inflation in 2026

Published February 3, 2026

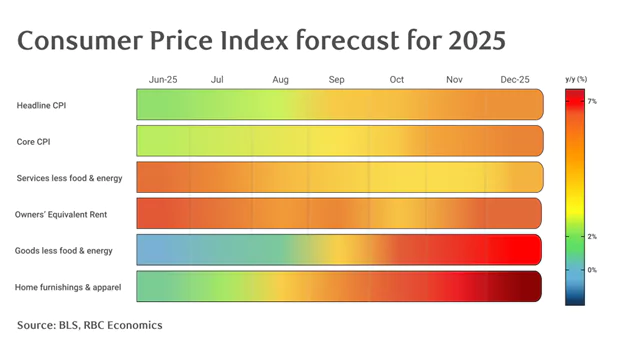

As we approach the five-year mark of inflation running above the Federal Reserve’s 2% target, we remain concerned about the likelihood it remains stuck closer to 3% throughout 2026. The combination of a tight labor market, strong consumer spending, tariff pass through, and a lagged housing inflation measure is a recipe for sticky inflation.

Recent developments have suggested some moderation in the inflation profile—in particular—a slowdown in core services and motor vehicle prices. But we’re not convinced these deflationary trends will continue in the coming year. That said, monitoring inflation is particularly challenging right now. Data distortions and disruptions, uncertain tariff policies, and structural shifts related to demographics are adding crosscurrents in inflation’s path, and our ability to read it.

The 2025 US federal government shutdown disrupted data collection—with monthly data largely missing for October and collected over a condensed window in November. Ongoing distortions complicate high conviction interpretation of month-over-month inflation prints. Meanwhile, the Owners’ Equivalent of Rent (OER) component of the Consumer Price Index (CPI) continues to distort the picture, exerting outsized influence on the CPI basket, though its impact on the Fed’s preferred measure, core PCE, is more limited.

Click here for our full guide on how to monitor inflation data in the months ahead.

Trade Zone: Smashing down the trade barriers within

Published January 30, 2026

Two of Canada’s top CEOs—Tracy Robinson of CN Rail and Max Koeune of McCain Foods—recently joined Sean Strickland of Canada’s Building Trades Unions for a discussion with the Business Council of Canada’s Goldy Hyder, on the big changes that Canada needs to make to infrastructure development, business regulation and immigration.

Robinson said we need to review our approach to labour negotiations to ensure the economy doesn’t get shut down as often as it does, especially in a world when other countries are happy to see that happen.

Strickland pushed for better labour force planning, to ensure we’re recruiting the right people and right numbers for the right needs in our economy. We’ve talked about that for years. It’s solvable.

Koeune called for immigration reforms that would give permanent residency applicants a clearer view of how long it will take, and where their application is at. He called the system a “black box,” which I’ve heard from plenty of other employers in recent months.

Davos ’26: Making sense of a new world order

Published January 25, 2026

Last year, a day after his second inauguration, Donald Trump spoke by video to the Forum and promised a golden age for America. This time, he came in person to proclaim victory. With five cabinet secretaries and hundreds of American CEOs in tow, the President spent an extraordinary two days in the Swiss Alps projecting a 21st century version of American power.

This is no stay-at-home superpower. In Trump’s vision, the world will trade and prosper more than ever, on America’s terms. Close to three-quarters of global trade is still compliant with WTO rules. Inventory build-ups helped many companies escape the initial tariffs. A greater impact may come this year. But for the most part, “it’s still holding,” said Christine Lagarde, head of the European Central Bank, arguing the global economy is so intricate and intertwined even the U.S. cannot unravel it.

Trump’s more mercantile Pax America is not just economic. He came with an unsolicited bid for Greenland that was rejected by his closest NATO allies. He left with a Board of Peace, supported by an unlikely collection of 19 countries with a combined GDP of $5 trillion, roughly equal to Germany. Only four (Albania, Bulgaria, Hungary, Turkiye) are in NATO, and only four (Argentina, Indonesia, Saudi Arabia, Turkiye) are in the G20. Will Trump be able to expand America’s reach without stronger partners? Or is this the new geometry of power?

Earnings season offers U.S. equity investors a chance to refocus

Published January 16, 2026

There were four big takeaways for us in last week’s update from EPFR on U.S. equity funds flows. First, passive retail flows to U.S. equity funds have been solid in recent weeks, suggesting to us that retail investors have been helping to support the rally in U.S. equities to start the year.

Second, when we zoom out, we see that flows to U.S. equity funds as a whole have been choppy in recent weeks, though flows to global equity funds have been strong. We see the former as a headwind to U.S. equity market performance and the latter as a tailwind given the heavy market cap representation of the U.S. in global benchmarks.

Third, funds flows are showing a slight improvement for Western European equity funds, pointing to the possibility that some geographic rotation was occurring within the global equity community as 2025 wound down and 2026 began. We will be keeping a close eye on this data, along with investor conversations, to gauge whether a new “Sell America” trade may be returning to the equity market. This is an issue that we have seen as a key risk/headwind to monitor and one that could reasonably be viewed as having grown/strengthened in the aftermath of recent geopolitical and central bank developments (though RBC’s Rates Strategy team has argued that recent events related to the Fed can be viewed as actually having strengthened perceptions of Fed independence).

Fourth, at the sector level we note improving flows for Financials and Industrials, two of the cyclical workhorses of the U.S. equity market, along with continued strength in Energy and Materials/Commodities funds.

Overall, we think these trends in funds flow data highlight the complex dynamics underpinning U.S. equities today – renewed and growing optimism on the U.S. economy, but within the context of a global investor community that has become more open to geographically diversifying their equity exposure and has been presented with some new reasons to potentially do so as the new year has gotten underway.

Global economic outlook

Published December 16, 2025

Canada is technically avoiding recession this year, with improving data heading into 2026. The labor market shows extraordinarily low layoffs, though unemployment is rising due to weak hiring that disproportionately affects young people. Mortgage renewal pressures are easing, household balance sheets are strengthening, and business confidence is beginning to improve. While certain economy segments struggle and the country remains worse off than without trade tensions, the trade impact from U.S. tariffs has proven far less severe than widely anticipated.

The effects of tariffs remain concentrated in specific sectors and regions. Steel, aluminum, various auto sector segments, and softwood lumber continue facing substantial tariffs, while tariffs on canola and aquatic products add pressure. The 10% of trade affected by tariffs is predominantly located in southwestern Ontario, where unemployment ranges from 9 to 11%, contrasting sharply with areas maintaining very low unemployment rates. As 2026 approaches, this regional divide will likely intensify, creating significant challenges for policymakers.

Several risks warrant monitoring into 2026. In the U.S., the trade shock from tariffs is likely only beginning to materialize. A potential pullback in spending by the wealthiest 10% could impact the labor market and consumption patterns. The 2026 election cycle presents an underappreciated risk during a fragile economic transition. AI investment currently supports growth and creates jobs, though much of this value may prove transitory.

2026 Outlook: Macro, monetary policy & rates

Published December 15, 2025

Treasury yields and curves are expected to remain range-bound throughout 2026, with temporary upward yield shocks possible from tariff-related developments. Potential stimulus measures ahead of the 2026 midterm elections, including possible tariff rebate discussions, could generate headlines around tariff revenues and their impact on supply-demand dynamics.

One of the bearish risks for rates centers on inflation expectations. Continued gradual pass-through of tariff costs, combined with easy fiscal policy and fading uncertainty around trade tensions, could collectively push inflation expectations upward in 2026. This represents the most significant downside risk to monitor.

Canada faces a fundamentally different growth landscape entering 2026 due to the transition to a new trade environment. Third-quarter GDP growth masked weakness in final domestic demand, while net trade benefited primarily from reduced imports.

CUSMA Deal and U.S. Rate Cut

Published December 11, 2025

The U.S. could carve out separate deals with Canada and Mexico. U.S. Trade Representative Jamieson Greer said Wednesday that the Trump administration is keeping all options on the table for the future of the Canada-U.S.-Mexico Agreement (CUSMA), which comes up for renewal in 2026. "Our economic relationship with Canada is very, very different than our economic relationship with Mexico," Greer said at an event in Washington. Meanwhile, Kirsten Hillman, Canada’s ambassador to the U.S., is stepping down as the country’s top diplomat in Washington in the New Year.

FOMC Decision: Fed ends 2025 with a cut but dissents reflect growing divide

Published December 10, 2025

The Federal Reserve delivered a widely expected 25-basis point cut at its December meeting. The critical unknown is how tariff policies will shape the economy in 2026, with concerns shifting toward the inflation backdrop as the year approaches.

"There is no risk-free path for policy as we navigate this tension between our employment and inflation goals," Powell stated. "A reasonable-based case is the effects of tariffs on inflation will be relatively short lived, effectively a one-time shift in the price level."

The full extent of tariff impact on inflation has yet to be felt, and delayed government data releases continue to limit visibility into inflation's trajectory. PPI data has been delayed until January, further obscuring the tariff picture. Absent a notable acceleration in December inflation data, a window may remain open for one more rate cut early next year.

However, monetary policy will have limited impact on addressing tariff pressures in 2026. If tariff passthrough results in narrowed margins and consequent layoffs, monetary policy can do little to resolve a policy-induced price level shock. The risks are becoming increasingly asymmetric toward inflation, and as more FOMC voters dissent, an extended pause appears increasingly likely as the Fed's next decision.

Driving into the fog

Published December 8, 2025

2025 was largely a year of treading water amid stagflationary currents, and 2026 may prove more of the same. Expect sluggish hiring, slightly below-trend growth, and inflation stubbornly above target but lacking upward momentum.

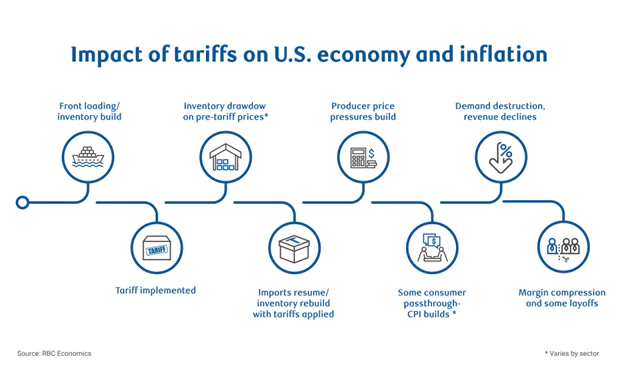

Trade policy dominated 2025 but will take a backseat in 2026. The Liberation Day uncertainty spike served as an inflection point, though full tariff pass-through impacts remain outstanding. Growing comfort with the trade war should allow hiring demand and corporate activity to thaw. A court ruling on IEEPA could alter trade policy trajectory, and risks lean toward relaxation as the administration seeks to boost sentiment ahead of mid-term elections.

Beyond trade, a still-large deficit, robust tax refunds, and possible fiscal stimulus should limit demand deterioration. Fed rate cuts and neutral monetary policy should add marginal support. Replacement demand from elevated retirements and declines in foreign-born workers should maintain a soft floor under hiring.

Five themes for the US economy in 2026

Published December 3, 2025

Heading into 2026, we see a US economy that is increasingly on track for a stagflation lite scenario: GDP growth running below the typical 2% trend, while inflation remains uncomfortably high. The inflation story extends beyond tariffs – core services inflation runs hot at 3.5%, driven by housing and sticky wages, while tariff passthrough to consumer goods is expected to peak in Q2 2026.

The US consumer is becoming increasingly fragmented. The top 10% of households drive a near majority of consumer spending, benefiting from favorable tax policies and non-labor income sources like dividends and rent. Middle-income households face the greatest inflation pinch, while lower-income groups benefit from government transfers and cost-of-living adjustments.

The labor market has loosened but remains historically tight at 4.4% unemployment. Demand-side weakness concentrates in trade-reliant sectors, while supply constraints from immigration policy and record retirements remove nearly 3 million workers from the labor force since 2024, keeping unemployment capped around 4.5% for most of 2026.

Data center investment has driven recent growth but hasn't yet generated meaningful productivity gains. AI remains an infrastructure investment awaiting workforce skills development.

Finally, massive government deficit spending at 6% of GDP provides economic guardrails—limiting downside while constraining upside growth potential.

For a comprehensive analysis, read the full report here.

Tariff talk from last week’s earnings calls

Published October 27, 2025

Overall, many of the companies that reported last week seemed to lean towards the idea that tariff impacts are stabilizing, while some continued to remind investors of the potential for future changes and continued to highlight the situation as dynamic.

Margin impacts were cited by some, but companies generally continued to highlight how they are managing through with discussions of their mitigation efforts.

Taking additional price increases was something we read about for several companies in different industries last week in the context of tariff discussions. We also took note of comments on the timing of tariff impacts, with one company noting they were halfway through the incremental tariff impacts on a year-over-year basis.

To access the full report, “The Pulse of the Market – Early Learnings from Earnings”, please contact your RBC representative.

U.S. and China develop “very successful framework”

Published October 27, 2025

U.S. – China developed a “very successful framework” during trade talks. While a deal wasn’t reached, both sides emerged from two days of “candid and in-depth discussions,” on everything from tariffs to rare earth metals, feeling confident with where things are headed.

The framework paves the way for a meeting in South Korea later this week between U.S. President Donald Trump and Chinese President Xi Jinping, the first face-to-face between the leaders of the world’s two biggest economies since Trump’s second term began.

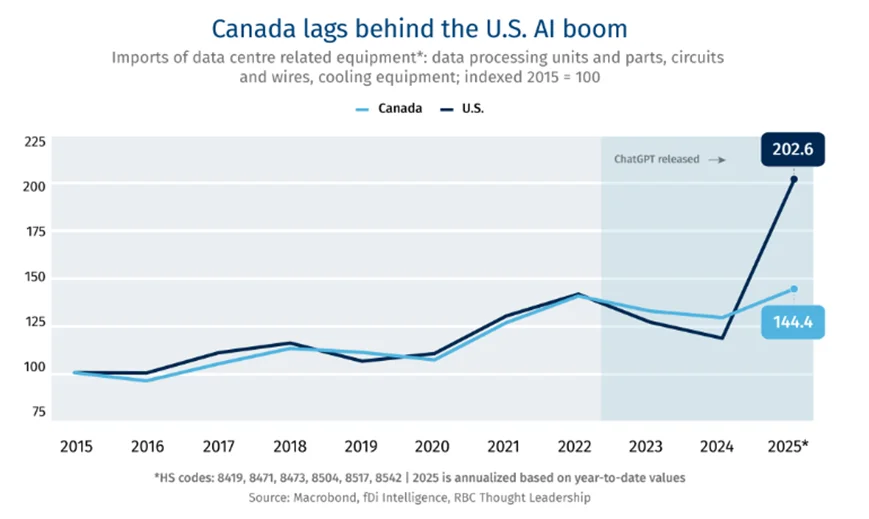

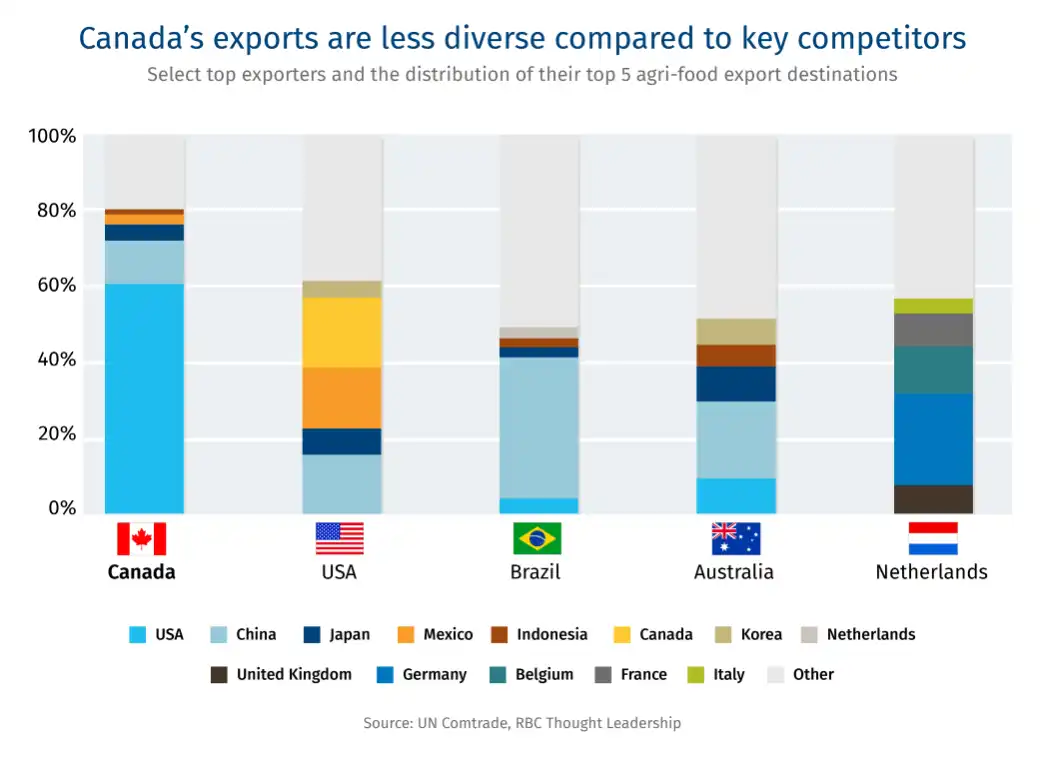

Missing the AI boom

Published October 26, 2025

AI-related investments may have masked the impact of the U.S. trade war on global growth so far, the IMF notes in the latest World Economic Outlook.

Since the release of ChatGPT in late 2022, U.S. firms have quadrupled data-centre construction spending to nearly US $40 billion. There are now 5,000 data centres dotted across the U.S. Imports of data centre related equipment is up 50% over the same period. Taiwan accounted for half of the growth when it comes to U.S. imports of digital processing units.

Canada, as the chart below indicates, has remained on the sidelines of the AI boom despite a growing number of data centre applications. Demand for related equipment has shown only a small uptick in recent years. Click here to read more on RBC’s ‘The Trade Zone’.

10% tariff on Canadian goods over ad

Published October 25, 2025

Donald Trump slapped an additional 10% tariff on Canadian goods over ad. The 60-second spot, sponsored by the Ontario government and featuring former U.S. President Ronald Reagan denouncing tariffs, had already prompted President Trump to call off all trade talks with Canada last week.

The Ontario government had said it would pull the spot, which aired during the World Series broadcast, on Monday. But Trump, who didn’t provide a date or what goods the increase would impact, demanded the hike on Saturday because the ad wasn’t removed immediately.

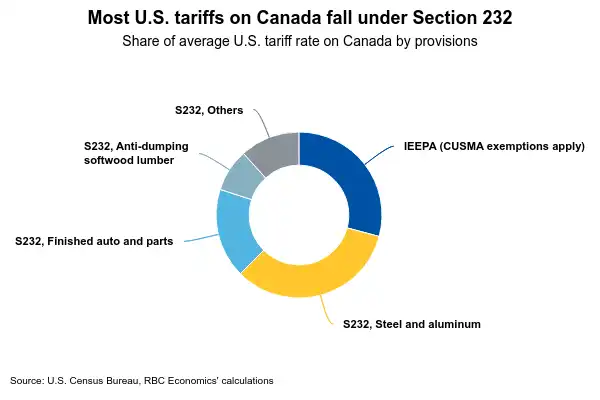

Softwood, Cabinets, and Beyond

Published October 14, 2025

Trade tensions between Canada and the U.S. continue to brew with new tariffs hitting key Canadian exports this month. U.S. duties on Canadian softwood lumber and kitchen cabinets kicked in on Oct. 14, and additional tariff threats loom over other critical exports, including pharmaceutical products and medium and heavy-duty trucks.

From our vantage point, these new tariffs are unlikely to significantly alter our baseline economic projections. The measures will raise the U.S. average effective tariff rate on Canadian imports by a modest 0.2%, nudging it closer to 6% from 5.5%. Yet the impact on specific industries – particularly forestry, logging, and wood manufacturing – will be far more pronounced.

What raises greater concern is the U.S.’s increasing use of Section 232 tariffs. These product-specific tariffs fall outside the exemptions provided by CUSMA. This effectively leaves more Canadian products and industries exposed to higher trade barriers.

To better understand the implications of these tariffs and their potential impact on the Canadian economy, click here to read our latest report.

Softwood, Cabinets, and Beyond

Flying Blind

Published October 6, 2025

We still think the Fed is going to skip a cut by the end this year – but an October skip now looks a lot less likely. More broadly, our views still lean more hawkish than market pricing does. If you want a pretty perfect summation of where our own view currently stands, we found ourselves vigorously nodding along as we read this passage from President Lorie Logan’s recent speech:

“As I consider the path ahead, three features of the economy stand out to me at this time: 1) even setting aside temporary effects of this year’s increases in tariff rates, inflation is not convincingly on track to return all the way to 2 percent; 2) aggregate demand remains resilient, supported by consumption, business investment and buoyant financial conditions; 3) while the labor market has undeniably slowed, with meaningful costs to workers, not all of the weakness represents economic slack that less-restrictive monetary policy can ameliorate ….

There may be relatively little room to make additional rate cuts without inadvertently moving to an inappropriately accommodative stance.”

We see softness in labor market demand largely as a product of tariff-related uncertainty in the months following Liberation Day. We see that as distinct from a more cyclical hit to aggregate demand, which would see businesses actively reduce headcount to protect falling profits. We don’t think that really describes what we’re seeing in the data. While hiring has dropped off sharply since Liberation Day, businesses aren’t resorting to layoffs, and we see the data post-April as more of a “deer in headlights” moment for businesses than a response to falling demand for their products/services.

To access the full report from our U.S. Rates Strategy team, contact your RBC Representative.

PM Carney to meet with President Trump

Published October 6, 2025

Mark Carney will meet Donald Trump on Tuesday. The Prime Minister will be in Washington in a bid to reduce U.S. tariffs or seek a deal with the U.S. President. The meeting “will focus on shared priorities in a new economic and security relationship,” Carney’s office said.

Washington has imposed punitive 50% tariffs on steel and aluminum and 35% of all Canadian goods traded outside the CUSMA trade deal. President Trump recently noted that the tariffs are hurting the Canadian economy and diverting investment to the U.S.

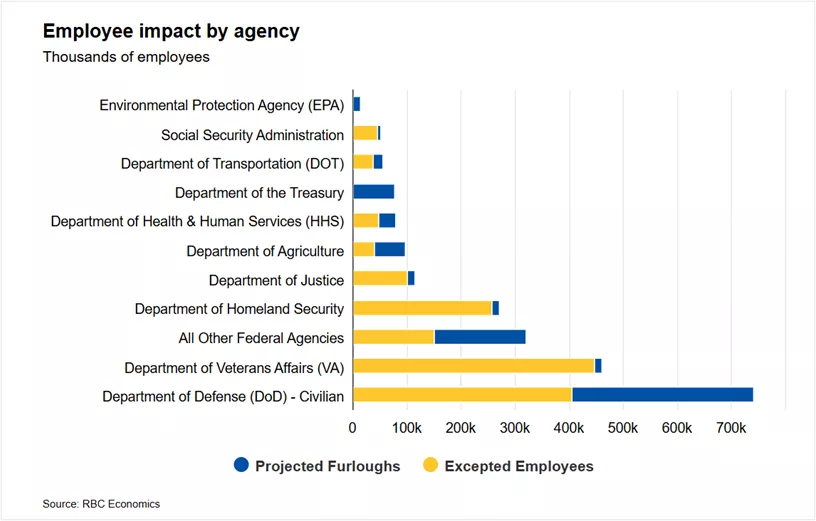

How to navigate the U.S. government shutdown

Published October 1, 2025

As widely expected, the U.S. government shutdown started at midnight on October 1st. The U.S. federal fiscal year runs from October 1st to September 30th and government funding is allocated on a fiscal year by fiscal year basis. This means that for the government to fully re-open, Congress must pass 12 separate appropriation bills that allow for U.S. federal agencies to allocate and spend funds on their operations.

Until those bills are passed, an estimated 750,000 Federal workers will be furloughed, comprising nearly all employees who collect and analyze economic statistics. As such, the widely watched employment report, CPI, retail sales, and GDP, among others, will not be reported until the government reopens.

Click here to read our latest report where we outline what this shutdown could mean for the economic data and growth moving forward, as well as some alternative, private data sets we will be monitoring in the absence of government data.

U.S. trade developments

Published September 26, 2025

Over the past week, the U.S. announced a series of trade developments across sectors impacting robotics, industrial machinery and medical equipment to trucks, furniture, pharmaceuticals and more.

Over the past week, a series of developments occurred in the Trump administration’s efforts to advance its tariffs and trade agenda. According to the latest Sullivan & Cromwell Tariffs Tracker, these include development that impact a range of sectors, affecting robotics, industrial machinery, medical equipment, trucks, furniture, pharmaceuticals and more.

Key developments:

- On September 26, 2025, the U.S. Department of Commerce published notices in the Federal Register requesting public comments in connection with recently commenced investigations into (i) robotics and industrial machinery and their components and (ii) personal protective equipment, medical consumables, and medical equipment, including devices.

- On September 25, 2025, President Trump announced on Truth Social that the U.S. will impose the following tariffs as of October 1, 2025: (i) a 25% tariff on heavy-duty trucks; (ii) a 50% tariff on kitchen cabinets and bathroom vanities and a 30% tariff on upholstered furniture; and (iii) a 100% tariff on branded or patented pharmaceutical products, unless the company is currently building drug manufacturing plants in the United States.

- On September 25, 2025, the U.S. Court of Appeals for the Federal Circuit issued a decision resolving a long-pending challenge to the first Trump administration’s modification of certain tariffs on Chinese goods under Section 301 of the Trade Act of 1974.

Tapping Indonesian nickle

Published September 26, 2025

After four years of negotiations, Canada signed a Comprehensive Economic Partnership Agreement (CEPA) with Indonesia last week.

The deal is expected to increase Canadian exports by $447 million–a paltry 0.04% increase over current figures. Still, it provides Canada with a call option on Indonesia’s economic growth. The country is expected to become a Top 5 global economy by mid-century and a vast market for Canadian agriculture, food products, machinery, services and even nuclear technology.

The announcement follows on the heels of the Trump Administration’s reciprocal trade deal with Indonesia, moving quickly to secure valuable critical mineral market access and resources—notably nickel. Indonesia agreed to remove its export restrictions on ore, allowing raw and semi-processed nickel to be shipped to the U.S. for refining and keeping the supply chain out of Chinese-operated Indonesian smelters.

Click here to read more about Canada’s big critical minerals push.

Canada-Mexico partnership

Published September 19, 2025

Canada agrees to a “strategic comprehensive partnership” with Mexico. During Prime Minister Mark Carney’s visit to Mexico City yesterday, he and Mexican President Claudia Sheinbaum announced an agreement to increase trade between the two countries in several areas, including energy, agriculture and critical minerals.

The two leaders also committed to work more closely on security and climate issues. The partnership between Canada and Mexico follows the news from earlier this week that the U.S. formally kicked off the CUSMA review process with public consultations.

A risk management cut

Published September 17, 2025

As was widely expected, the FOMC went ahead with a 25 basis-point cut in today’s meeting. But this meeting wasn’t about a cut (or two). It felt more like a reset of expectations for what the Fed sees ahead and how they will navigate this ongoing uncertainty surrounding their dual mandate.

We expect the biggest challenge going forward will be inflation and the uncertainty surrounding the pass-through of tariffs to consumers. Even before accounting for the impacts of tariffs, we expect to see inflation accelerating into year-end off the back of (i) goods prices rising (ii) services prices remaining sticky viz a viz wages and (iii) a floor under housing prices.

Before the next meeting, we expect the September CPI data will continue to show early signs of tariff pressures building, but we likely will not see material passthrough until we get closer to the December meeting, at which point, we expect core CPI to have reached 3.4%. We think the Fed's preferred measure (core PCE) will be telling the same story. That’s going to make a full-blown easing cycle more difficult but not impossible.

We saw a large dispersion in the 2026 dot plot – with significant uncertainty surrounding timing and magnitude of tariff passthrough to prices and the extent to which this weighs on growth. And while the weaker labor market data is currently giving the FOMC an opening to cut, we expect that justification will become more difficult in the months ahead.

For more economic forecasts, analysis and insights, visit rbc.com/economics.

FOMC recap: Muddled in, muddled out

Published September 17, 2025

Outside of the widely expected 25bp cut, it was a bit of a confusing FOMC day. Powell seemed to struggle a bit justifying today’s cut and the slightly more dovish stance of the rate dots. He looked particularly uncomfortable on questions regarding the upside risks to inflation. Even on the labor side of the mandate…Powell’s answers seemed a bit muddled.

But in our view, none of this is an indictment on Powell. His comments around the outlook and stance of policy sounded muddled today, because the outlook and case for cuts IS muddled.

Powell is dealing with two-way risks that, as mentioned above, aren’t clearly leaning in one direction or the other. Some of the biggest of those risks could be upended with the bang of a gavel or stroke of a pen (i.e. tariffs). Like us, he doesn’t really know:

- How to interpret NFP prints given a wide and uncertain range around the NFP “breakeven” (he cited 0-50k).

- He has no historical roadmap for understanding how tariffs this broad or severe are going to work their way into inflation, inflation expectations, or growth.

- He doesn’t seem particularly convicted on where short-run neutral is right now – always says you will “know neutral by its works”.

- He is dealing with a split committee – apparent in the very atypical bi-modal distribution for the 2025 dots (despite being two meetings away from those dots being realized).

Lastly, while he may not admit it, there has to be some concern at the back of his mind about how every sentence might put the long-term independence of the Fed at risk.

Five disruptors to the U.S. economic cycle

Published September 15, 2025

The U.S. economy seems in many ways an anomaly.

Interest rates are in “restrictive” territory, and yet the unemployment rate remains quite low. The economy is in the midst of a historic trade shock with 100-year high tariffs, but the impact from inflation appears limited so far. The housing market, historically a solid leading indicator, is experiencing very limited activity on par with the aftermath of the global financial crisis, and yet home prices and rents continue to rise.

The answer to the disconnects, in our view, lies in a series of medium to long-term disruptions that are distorting an economy’s typical responses, and muting the standard “economic cycle.”

These disruptions make clarity on the U.S. outlook more difficult, but not impossible. They necessitate a shift in the way we think about the business cycle, cyclical versus structural trends, and even the way we absorb monthly economic data.

Ready, set, slow

Published September 12, 2025

The outlook for global central bank policies continues to evolve, and particularly for the Fed, it could have significant implications for global asset markets. On RBC’s Macro Minutes podcast, the team delved into the key macro themes driving monetary policy decisions and discussed when/if policy easing cycles will re-start, how fast they could go, and how low terminal rates might get.

Listen to the full episode below or on Apple, Spotify or YouTube Music.

“…right now, we’re facing upside inflation pressure or a lot of unknowns around how this tariff passthrough is going to hit the inflation side of the Fed’s mandate. If you look at the breakdown between the ‘doves’ and the ‘hawks’ on the FMC…

The doves are seemingly very confident that this inflation is a) entirely tariff-related and b) going to be a one-time shock. It’s a one-time price level adjustment and then we return to 2% inflation.

The hawks are saying if they look at both the labor and inflation side, we’re currently missing our inflation target by a fair amount. We’ve got a three handle on core CPI and moving in the wrong direction. Meanwhile, labor levels that historically would be considered very healthy…

I think the administration wants it, the markets have priced it in, a third of the committee wants to start cutting…so a cut this month seems like the path of least resistance. I still think there could be a pause in October.” – Blake Gwinn, Head of U.S. Rate Strategy

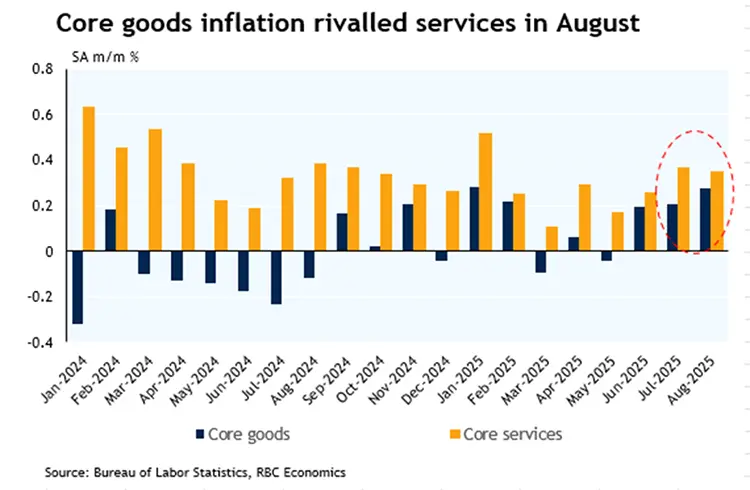

US CPI: Core goods and services pressures mounting

Published September 11, 2025

Inflation data from August continues to paint a concerning picture of uncomfortable services sector inflation that is now compounding goods sector pressures that are building. Core inflation landed in-line with consensus, at 0.3% m/m (3.1% y/y). This month marked the first month in which core services has not significantly outpaced core goods (both at +0.3% m/m) since January 2022.

We witnessed a widening breadth of inflation pressures in August and saw upticks in some trade-exposed sectors for the first time (new motor vehicles) – setting a concerning precedent for the inflation trajectory in the months ahead and when coupled with cyclically weak labor market data, serve as mounting evidence that tension is building on both sides of the Fed's mandate.

We have consistently been watching inflation through two lenses:

1) Tariffs notwithstanding, inflation was unlikely to reach target this year. We expected to see upward pressure building in services inflation through a variety of channels and this materialized in the August data, with core services inflation +0.3 m/m (stuck at 3.6% y/y).

Wage growth is still well-above pre-pandemic trend – and higher wages will continue to fuel services sector price pressures. If tariffs continue to translate to higher core goods prices – as we expect they will – these pressures will compound pre-existing services sector inflation.

2) Tariffs are starting to build on uncomfortable services sector inflation. Core goods inflation rose +0.3% m/m in August (at 1.5% y/y). Pressures mounted in most tariff exposed sectors this month.

For more economic research, visit rbc.com/economics.

Canadian aluminum market; companies absorbing tariff costs

Published September 10, 2025

Europe emerges as a new market for Canadian aluminum. The continent accounted for 18% of Canadian aluminum exports in the second quarter, compared to just 0.2% in the previous quarter, as Canadian producers redirected metal exports to avoid punitive U.S. tariffs.

The U.S. now accounts for 78% of Canada’s aluminum exports, compared to 95% before, according to S&P Global Market Intelligence. The data highlights how the 25% U.S. tariff on Canadian aluminum has disrupted trade in North America’s highly integrated market.

Canadian companies are absorbing tariff costs. Third quarter data from Statistics Canada’s Canadian Survey on Business Conditions showed 42% of businesses didn’t pass along tariff-related cost increases to their customers in the past six months.

But that could change soon as around 40% of firms said it’s very likely or somewhat likely they’ll need to increase prices to cover tariff costs over the next year.

Nearly a fifth of businesses also reported higher sales of Canadian products, with around 21% of businesses changing their marketing to highlight Canadian-made goods.

How CUSMA strengthens both U.S. and Canadian economies

Published September 2, 2025

Amid the ongoing trade war, the Canada-United States-Mexico Agreement (CUSMA) has been a crucial backstop.

While product specific tariffs on goods including steel and aluminum, copper, and non-U.S. content in auto products remain, most Canadian exports have continued to cross the border duty free under a broad exemption from tariffs for trade compliant with CUSMA rules of origin.

Preserving that exemption is critically important for Canadian producers and exporters – and negotiations to extend CUSMA beyond 2036 are scheduled to kick off next year.

While U.S. trade policy remains highly unpredictable, there are good reasons to be hopeful that the CUSMA free-trade agreement could and should remain intact.

Click here to read the full report “How CUSMA strengthens both U.S. and Canadian economies”, published by RBC Economics.

Trade court ruling highlights risks of importing

Published September 2, 2025

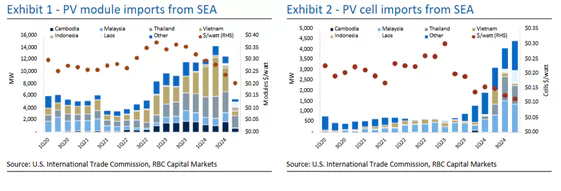

Trade court ruling affirms solar duties under Biden administration. This past week, the ITC ruled that the Biden administration exceeded its statutory authority in its two-year moratorium (June 6, 2022 to June 6, 2024), preventing the U.S. Customs and Border Protection agency (CBP) from collecting duties related to Chinese companies circumventing AD/CVD tariffs by finishing products in Vietnam, Cambodia, Malaysia, and Thailand.

The Auxin v. U.S. decision allows the CBP to immediately begin retroactively collecting duties on cell and module imports from Cambodia, Malaysia, Thailand, and Vietnam during that time period. During this period ~88.2 GW of solar cells and panels were imported from these SEA countries with a total import value of ~$26.5 billion. Applying existing tariff rates (15.25% CVD and 238.95% AD) to this would equate to nearly $70 billion in retroactive tariffs that the importer of record will likely be responsible for.

Our view: We believe this has limited implications on industry as panel stock is already in the country either installed or in warehouses and will face duty charges whether installed or not. This could bias pricing higher near term as importers try to pass along some of the duty charges, though we think price will be dictated by supply/demand dynamics and that limits the opportunity.

U.S. equity markets – weekend tariff thoughts

Published September 1, 2025

On Friday, the U.S. Court of Appeals for the Federal Circuit ruled against the reciprocal tariffs. We anticipate questions on the implications for the US equity market outlook, so here are some of our initial thoughts.

In the short term, our initial instinct when the news first came out was that U.S. equity markets were unlikely to react much, and that remains our view ahead of Tuesday’s open. U.S. equity investors have generally moved to a “wait and see” mentality when it comes to various geopolitical and domestic policy/political developments over the summer.

On a more intermediate term basis, we think corporate uncertainty around tariffs will remain elevated, though lower than late spring levels. One of our biggest takeaways from 2Q25 reporting season was that companies continued to view the tariff backdrop as dynamic, evolving, and uncertain, despite the general dialing down of tariff levels from those announced April 2nd.

There are both positives and negatives associated with the continuation of elevated uncertainty.

- On the positive side, the potential for a further dialing down of overall tariff levels (beyond the obvious hope that tariff cost pressures could ease and the short-term boost to earnings estimates that would provide) is that it could keep corporates from taking more drastic actions to offset tariff costs.

- On the negative side, even if it’s due to hope for improvement, continuation of elevated uncertainty could contribute to further caution or delays in corporate customer decision-making that a number of companies continued to refer to during the last reporting season.

U.S. tariffs ruled illegal

Published September 1, 2025

The U.S.’s “Liberation Day” tariffs are illegal. That’s the verdict of a federal appeals court, upholding a ruling from the Court of International Trade, which had also rejected President Donald Trump's argument that his global tariffs, including on Canada, were permitted under the International Emergency Economic Powers Act (IEEPA).

Trump called the appeal courts’ 7-4 decision “highly partisan” and vowed to appeal, suggesting the U.S. Supreme Court will have the final word. The IEEPA tariffs are separate from the U.S. steel, aluminum and auto levies on Canada.

Not your 2024 Jackson Hole

Published August 15, 2025

Top tier data hasn’t added any clarity to the Fed outlook heading into Jackson Hole. Tension between the two sides of the mandate is going to make it difficult for Powell to signal a rate cut as clearly as he did last year. We still see a hold in September and first cut in December.

Labor risks are being oversold - we have basically been chopping sideways in a soft, low-hiring low-firing mode for some time.

Inflation level and trend – tariff impact or no – isn’t great. The Fed’s Musalem put it well: “…we are missing on our inflation target. We are not missing on our employment mandate.”

- It’s fine to want to “look through” tariff impacts – but it’s becoming clear that these impacts are going to be extremely tough to identify in the data and may take many more months to be fully realized. This is because of the breadth of tariffs, the long and uneven rollout, and varying and delayed corporate responses. Past tariff experiences, with a clear “switch” turned on for specific regions and products, are much easier to track and analyze.

- The risks that tariffs aren’t a one-off are still very real, yet there seems to be much more focus on the risks that labor deteriorates significantly.

- Aside from tariffs, let’s not forget inflation numbers weren’t exactly great before Liberation Day – the downward trend in core PCE basically flatlined above 2.6% in June 2024.

As for the Fed, many of the recent speakers seem unconvinced on need for a cut right now. We think a majority of the FOMC participants are truly going into the NFP print without having made up their minds on a September cut or pause.

This is an excerpt from “Ahead of the Curve: Not your 2024 Jackson Hole” published by our U.S. Rates Strategy team. To access the full report, please contact your RBC representative.

U.S. CPI: Core services surge sets concerning trend in July

Published August 12, 2025

Three core themes stood out in today’s report:

1. Core services surprised to the upside in July

A notable uptick in core services pressure in July (+0.4% m/m) showed that core services continue to outpace core goods price growth. This is a concerning precedent as we continue to expect mounting pressures from both core goods and services.

Tariff pressures are only one ingredient of the upward trajectory in our inflation forecast through the back half of the year. Long-term demographic trends mean wage growth will limit the degree to which core services inflation can moderate, and if today’s print sets a precedent, it is a concerning one.

2. Stagflation lite scenario is taking hold

This morning’s inflation print was an indication that we are continuing to see mounting evidence of our “stagflation lite” scenario taking hold. Today’s print taken with recent NFP revisions signals a scenario is evolving where both sides of the Federal Reserve’s mandate may soon be at odds – as trade policy bolsters price pressures while firms freeze hiring.

Still, it takes time for tariffs to flow through to consumer prices and this print is just an initial uptick that likely signals the start of a broader trend.

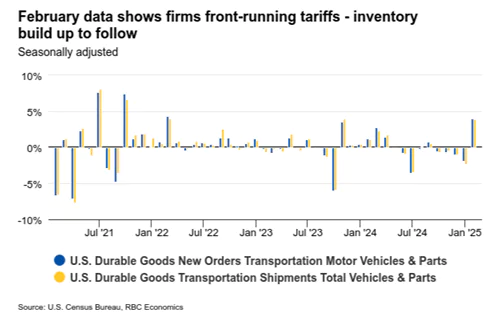

3. We are still waiting for tariff pressures to show up in some trade-exposed sectors

While we saw notable pressures in some sectors, others were still unaffected for now. This is unsurprising given the notable inventory build ahead of tariff implementation. We have reason to believe that in many sectors, an inventory drawdown is still taking hold.

For more U.S. economic commentary, visit rbc.com/economics or contact your RBC representative.

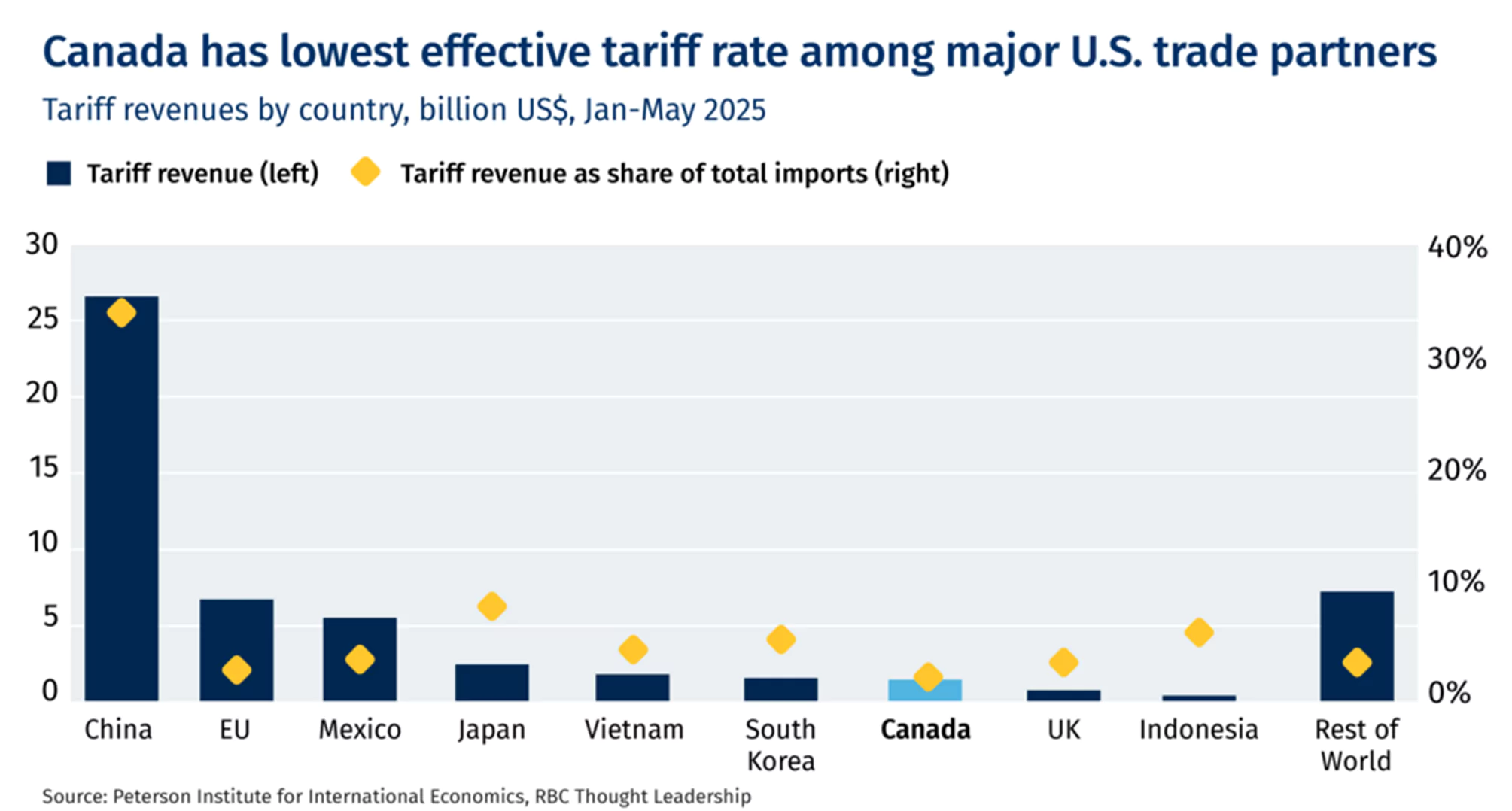

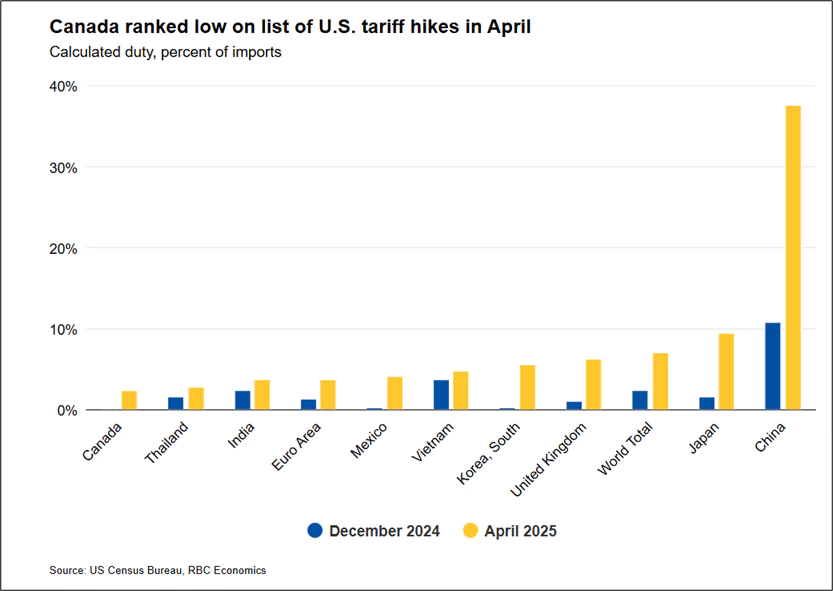

Tariff revenues by country

Published August 12, 2025

U.S. sets sights on pharma and chips

Published August 11, 2025

President Trump said tariffs on imports of semiconductors and drugs could come “within the next week or so” and eventually reach 250%, as the U.S. aims to boost domestic production in both sectors.

In July, Trump sent letters to 17 drug companies urging them to lower U.S. drug prices by Sept. 29 to “most favored nation” amounts paid by other countries. U.S. stocks were bogged down by the latest tariff threats.

We have no decisions about September meeting: Powell

Published July 30, 2025

Blake Gwinn, Head of U.S. Rates Strategy at RBC Capital Markets joined BNN Bloomberg: The Close to discuss The Federal Reserve’s path forward after leaving rates unchanged, how tariffs may impact inflation, the latest labor market data and more.

Click here to watch Blake in action.

FOMC Recap: Powell playing the waiting game

Published July 30, 2025

Powell justified their decision to hold rates steady today in two ways. First, he talked about what we can observe now, which is an economy that is still generally healthy (i.e., what the labor data is telling us) along with stubborn inflation. Powell stated, “we think policy should be restrictive because inflation is above target. When we have risks to both goals, one of them is farther away from goal than the other and that’s inflation… That means policy should be tight because tight policy is what brings inflation down.”

But what stood out the most is Powell’s assessment of inflation – even without tariffs, he views the path of inflation as “running a bit above 2%…even excluding tariff effects.” Interestingly, he went onto describe some of the catch-up inflation we are still seeing following the Covid supply-chain shock, namely auto insurance costs. In that light, we wonder if they expect to see a similar transmission of inflationary pressures in the insurance and broader services space as a result of tariff shocks. He also mentioned risk of added price pressures resulting from the cover of tariffs, specifically citing the rise in dryer prices despite washing machines being tariffed.

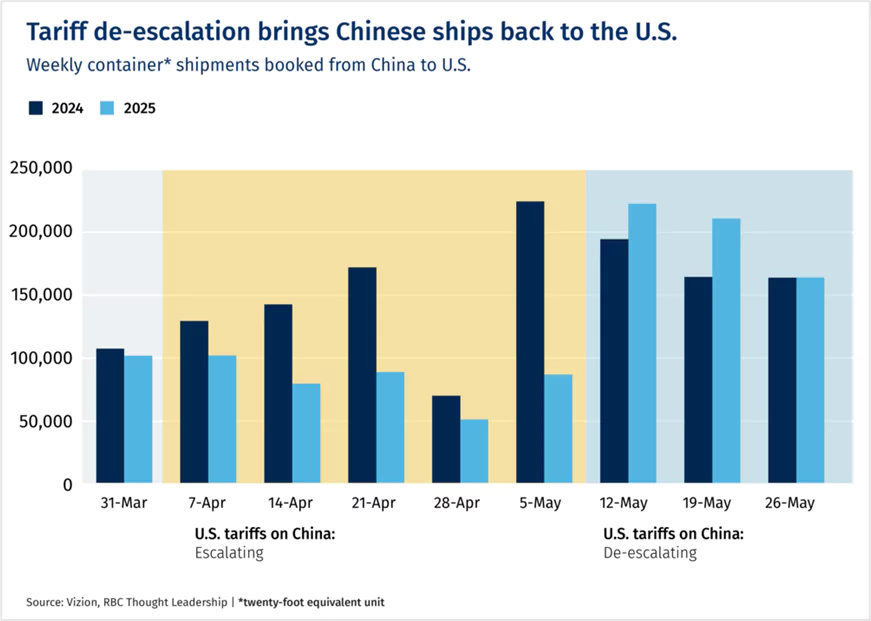

U.S.-China trade talks gain momentum

Published July 30, 2025

After two intense days of “constructive” talks in Stockholm this week, U.S. and Chinese trade representatives hinted at progress, agreeing to work toward extending the pause on tariffs set to expire on August 12. U.S. Trade Representative Jamieson Greer declined to weigh in on the likelihood of a deal but noted that conversations are “going in the right direction.” No word yet on whether U.S. President Donald Trump will meet Chinese President Xi Jinping, although Trump claimed that the Chinese leader has extended an invitation.

“I think this is the biggest deal ever made”

Published July 28, 2025

That’s how U.S. President Donald Trump framed the U.S. trade deal with the EU, which includes 15% tariffs on most goods from Europe and US $600 billion worth of EU investments into the U.S.

The framework closely resembles the U.S.-Japan deal announced last week. As far as coming to an agreement with Canada before the August 1 deadline, Trump said he isn’t sure it will happen and added that the U.S. may simply impose a tariff on its neighbor.

Q2 earnings takeaways on tariffs

Published July 28, 2025

Our overall impression from 2Q25 reporting season is that companies are managing through tariffs fairly well so far, but it’s still too early to assume tariffs won’t generate inflation pressures. A number of companies pointed to the 2nd half of 2025 as when tariff impacts are likely to kick in.

Here are four takeaways on what we learned in 2Q25 reporting season:

- The overall tone still seems “fine but not fabulous” as we observed last week. Overall, companies seem to be managing through headwinds, though some are doing so better than others or sound more confident about their ability to do so going forward.

- Second, on demand – our impression coming into last week was that tariffs and policy uncertainty generally had been accompanied by no meaningful impact to demand for some companies, a pause in activity or delay in decision making for others, and a pull-forward of purchases or activity for others, though the exact mix between the three seemed unclear to us. That generally remains our impression after going through last week’s transcripts.

- On the consumer, we spent some time focusing on what the consumer companies, who we think give a more boots on the ground read for what’s going on than the Financials, had to say about the health of the consumer. We continued to get descriptions of the consumer as cautious yet resilient, while highlighting pressures on the low end and value-seeking behavior generally. Some companies are also highlighting the consumers’ sensitivity to pricing.

- The timing of tariff impacts that’s worth noting. We took note of five different companies from the consumer goods and industrials sectors that discussed how tariff impacts were set up to hit in the 2nd half of the 2025. This helps to keep us in the camp that it’s too early to write off potential inflation impacts from tariffs as many investors have done. This also keeps us nervous heading into the fall, as U.S. equities tend to be strong over the summer, if you look at the past five years, but weak in the September-October time frame.

For more commentary, listen to the latest episode of the Markets in Motion podcast. To access the full report, please contact your RBC representative.

Listen and subscribe on Apple, Spotify and YouTube Music.

U.S. inflation ‘a squeeze higher’ in second half 2025

Published July 24, 2025

RBC Economics current U.S. outlook can be characterized as “stagflation-lite” – growth running below trend coupled with inflation that is uncomfortably heading higher into year-end. The latter is less of a shared view, particularly as recent inflation prints have suggested price pressures are calming. Looking ahead, however, we see the headline and core CPI reaching above 3% by the end of 2025.

Importantly, our view of higher inflation is only partly fueled by our assumptions around the impact of tariffs. Core inflation slightly above 3% is a long cry from the more disastrous price shock during the pandemic. However, it will likely continue to weigh on most households, encourage the perspective that inflation is structurally higher post-pandemic, and further complicate the Fed’s dual mandate of price stability and full employment. We see four relevant areas worth monitoring for upside inflation pressures.

Read the full report – US inflation outlook: A squeeze higher in second half of 2025

U.S. and Japan agree to deal, lowering tariffs to 15%

Published July 24, 2025

As part of the trade pact, Japan will allow more imports of American cars and rice, and invest $550 billion in the U.S. Tariffs on Japanese cars, which make up most of its trade surplus with the U.S., were lowered from 25% to 15%.

The deal comes at a time of political uncertainty in Japan—an upper house election loss by the ruling Liberal Democratic party has led many to call for Prime Minister Shigeru Ishiba’s resignation.

How tariffs will flow through the U.S. economy

Published July 21, 2025

Economists are making a range of assumptions about how tariffs may work their way through the economy without relevant historical precedent. Using our own set of assumptions, we expect tariffs will weigh on the labor market and put upward pressure on inflation, exacerbating our view that the US economy is in a stagflation-lite scenario.

But, when and where those pressures show up will ultimately come down to two core questions: How much inventory has accumulated in the system ahead of the implementation of tariffs, and how much of the cost of tariffs businesses will pass to consumers.

As policies continue to evolve in the coming months and data begins to show evidence of the impact of tariffs, RBC Economics will be using a transmission framework as a roadmap to monitor the fallout.

Read the full report – Transmission framework: How tariffs will flow through the US economy

US CPI: Tariff pressure building under the hood

Published July 15, 2025

Bottom line: Our key takeaway is that tariff pressures are starting to show up in core goods, but cooling auto prices are masking the full extent. June provided another modest core inflation print (0.2% m/m) despite the threat of tariff pressures. Core services prices showed continued signs of moderating as consumer demand for services has waned in recent months. While core goods did rise 0.2% m/m, there were notable declines in both new and used auto prices despite the tariffs put in place on the sector itself, as well key inputs like steel and aluminum.

We continue to expect the import/inventory buildup will provide a buffer to high prices in durables goods, delaying the full impact of tariffs until later this year. But signs of tariff pressures are showing up in other goods, notably recreation and household furnishings and supplies (i.e., appliances).

The rise in the goods space will likely weigh on consumer demand in the coming months – and we do expect to see a pullback in goods spending as a result. But a bigger risk comes from demand destruction in the services space – if consumers continue to pull back meaningfully on spending there, we would expect to see job losses materialize.

Industrials sector: Tariffs still a fluid situation

Published July 14, 2025

Tariffs still a fluid situation but de-escalating vs. 1Q25; FX tailwind; geopolitical pressures. Though slightly varying across the industrial sub-sectors, we believe the significant de-escalation in tariff dynamics since the last earnings season implies a better-than-feared operating backdrop and room for margin/earnings upside as we head into 2Q25 and get 2H25 outlook updates.

FX has become a meaningful tailwind for U.S.-based companies.That said, as recent short-cycle indicators suggest, contractors and project managers could remain wary of pushing forward with project activities on tariff uncertainties (i.e., who pays the cost), and geopolitical turmoil also weighs on CEO confidence.

High-level industrial subsector commentary:

- Multis – Tariffs have been de-emphasized in recent conversations, likely creating a bias for “beat and raise” in 2Q25, but management teams could “bank the upside” for now.

- Transport/Rail – 2Q25 cargo volumes came in better than expected, with upside in bulk products (coal and grain). Chemicals, metals, forestry, and motor vehicle cargo volumes were largely as expected.

- Aerospace & Defense – In Aerospace, resiliency in aftermarket, especially in engines, remains the decided positive. Within Defense, excitement is building up for key programs including the Golden Dome.

- Clean Energy – Have held relatively well, though the “One Big Beautiful Bill” creates some uncertainties around clean energy tax credits.

- Auto & Auto Parts – One industrial sub-sector that is likely to feel the brunt of tariffs during 2Q25 due to its “just-in-time” manufacturing and companies’ reluctance to hike prices during the quarter. We expect carmakers to respond with higher prices starting in 3Q25, weighing on volume in 2H25.

- Paper & Forest Products – Top-of-mind remains ongoing reduction in capacity against weaker demand backdrop, with roughly 5% of capacity expected to come offline in 2025.

- European Industrials – There is excitement around European stimulus including an investment upcycle in Germany, though we caution the upcycle is likely at a nascent stage, and we expect early investment benefit in 2026/2027.

Investor sentiment on tariffs

Published July 10, 2025

RBC’s Lori Calvasina, Head of U.S. Equity Strategy, joined CNBC’s ‘Closing Bell Overtime’ this morning to talk about investor sentiment around the impact of tariffs, whether the market is overbought at the current levels and more.

Click here to watch Lori in action.

Risks to later cutting cycle start have grown

Published July 9, 2025

We still see a first cut in September. That could come on either continued softness in inflation, growing cracks in labor data, or a little bit of both.

But the pushback of tariff deadlines means another 30-days of uncertainty and could mean companies stalling further on tariff responses (passing on costs to consumers, accepting margin compression, cutting costs, etc.). This could also serve to keep the Fed locked in “wait-and-see” mode longer than we expect.

The current state of labor data isn’t enough to pull the Fed out of “wait-and-see” on its own, and overall, we think the labor data is barely reaching Defcon 4 in the Fed’s eyes.

A hot CPI next week could upend near-term cut expectations as well. This would reinforce tariff-related inflation concerns among FOMC participants and push market pricing of the first cut further out (as it has already been doing over the last week or so). In contrast, if CPI is soft, the Fed just turns their eyes towards July data.

Overall, we still think the next two months of labor data could show some increased softening. As long as the inflation data doesn’t also pop, this could still be enough for the Fed to start cutting in September. But if inflation data starts coming in hot, July labor data sees a repeat of June, or if the Fed starts mentioning potential delays in tariff impacts due to the deadline extension, it will be very easy to push our cut call out to November or even December.

To access the full report from our U.S. Rates Strategy team, please contact your RBC representative.

Liberation delay (2/x?)

Published July 9, 2025

With the delays in implementation of reciprocal tariffs to August 1st, the administration is (again) extending the deadline for countries to reach new trade “deals” with the U.S.

Despite some limited volatility immediately following the announcements, rate markets seem to have brushed these headlines off. Short-expiry volume has declined across tenors and overall, there doesn’t seem to be a lot of fear that these tariffs will be going into effect in August either.

We are reminded of a similar learning curve in Trump’s first term, where the market reaction to “tape bombs” seemed to become more and more muted over time (see diminishing reactions to multiple rounds of infrastructure “announcements”).

U.S. plans 50% copper tariff

Published July 8, 2025

Our view: This could cause a short-term push to get more copper into the U.S. ahead of the tariff. However, once this ends, the risk is the London Metal Exchange (LME) price falls as the pull to the U.S. stops and the U.S. (7% of global demand) is left in surplus in the near term. The prospect of the tariff has already left inventory levels in the LME and Shanghai exchanges low and supported prices in all markets.

We expect further short-term volatility in copper and copper equity prices and this could be a negative for the majority of copper miners once the tariff is implemented, although the resulting low inventories provide downside support. Post tariff implementation, we think the market can revert to fundamentals and believe supply constraints and improving demand can support prices.

To access this report and our global research team’s copper outlook, please contact your RBC representative.

After Independence Day comes Liberation Day 2.0

Published July 7, 2025

Markets are bracing for the more consequential American spectacle on July 9 when the 90-day pause on Liberation Day tariffs comes to an end. Will there be more pyrotechnics or a fizzle out?

“About 10 to 12 countries are very close to a deal,” said Joseph Lavorgna, an advisor to U.S. Treasury Secretary Scott Bessent, with another 20 negotiating in good faith. “And Secretary Bassett highlighted that many deals could be done by Labor Day.” Is that a tell that the administration is looking to push past July 9? Who knows.

While Canada has an eye on that date, Prime Minister Carney has marked his own red circle in the calendar: the July 21 deadline to conclude a security and economic deal with the U.S. To facilitate talks, Ottawa scrapped its digital services tax on Big Tech, which was an irritant to President Trump. Canada is now back in the “front of the line” in trade negotiations, assured Pete Hoekstra, U.S. Ambassador to Canada.

While Trump recently said his administration has “all the cards” in its negotiations with Ottawa, Carney has a few aces up his sleeve, too.

U.S. week ahead: Sparse data week shifts focus to tariff deadline

Published July 3, 2025

While we have a few data prints coming in next week, the central focus will be on the July 9th trade deadline, which marks the end of the Administration’s 90-day pause on Liberation Day tariffs.

Regardless of what is announced next week, two facts hold true:

1. The current average effective tariff rate in the U.S. (currently near 14%) is at a level for which we have no recent precedent and even with the 90-day pause in place, current trade policy is going to drive core inflation notably higher by the end of the year.

If the 10% average tariff on imports from most countries is maintained alongside higher tariffs on steel and aluminum and motor vehicles and parts, we could see core inflation surpass 3% and approach 3.5% by Q4, and this will result in slower growth. If Liberation Day tariffs are re-instated and sustained (at a similar magnitude to what was announced on April 2nd), this would result in an even worse outcome for core inflation.

2. Regardless of next week’s outcome, that “on-again off-again” tariff policy is disruptive and puts consumers and businesses in a position of uncertainty paralysis.

This weighs on consumption as households defer major purchases and it weighs on hiring and business investment, as firms avoid making major decisions in a vacuum. A deferral of the 90-day deadline would be a continuation of the status quo, and the status quo is immense uncertainty that will continue to hamper activity this year.

The rapidly evolving bull thesis

Published July 2, 2025

We spent last week on the road seeing institutional U.S. equity investors in several different states. While it did not appear to us that they were uniformly bullish on U.S. equities, some came across as downright excited and most of those who had been more tempered in their outlooks appeared to be talking themselves into a more bullish stance. Based on what we heard last week, the bullish thesis seems to have evolved a bit.

While tax cuts and deregulation are still seen by many as stimulative, the focus on tax in particular has narrowed, with many investors making the case for a ramp-up in capex spend due to some provisions in the tax law (this has gone hand in hand with a high degree of bullishness on the extremely expensive Industrials sector).

The cooler inflation data that has been seen recently also appears to have caused many investors to believe that there simply will not be any inflationary impacts from tariffs, and several also expressed doubts about any adverse impacts coming to labor or the broader economy.

Instead of displaying a willingness to power through any tariff-related potholes, U.S. equity investors seem to be gravitating towards the idea that there simply will not be any potholes.

To be fair, not everyone we spoke with agreed with this rosy assessment, but we ended the week thinking that overall conditions in U.S. equities didn’t seem frothy quite yet but were headed down that path.

This is an excerpt from The Pulse of the Market – Mid-Year Market Musings written by Lori Calvasina, Head of U.S. Equity Strategy. Contact your RBC representative to access the full report.

CNBC Fast Money: China’s economic struggles

Published July 1, 2025

Lori Calvasina, Head of U.S. Equity Strategy at RBC Capital Markets, joined Fast Money as a guest trader for the 5 p.m. hour to discuss where the U.S. is in the equity market snapback, the AI evolution, China and tariffs, what recent M&A may be signaling for corporate confidence and more.

Click here to watch Lori in action. You can also watch the full episode here and listen here.

RBC U.S. Equity Capital Markets tariff update

Published June 30, 2025

Risk-taking has been encouraged by transient policymaking, including a declaration on Thursday by Trump that the July 9th deadline on the 90-day extension of tariffs is ‘not critical’ along with the growing possibility of an early replacement of Fed Chair Powell in favor of a more dovish appointment.

President Trump’s decision to end all trade discussions and threat to impose a fresh tariff rate on Canada Friday afternoon caused the recent rally to pause heading into the weekend. Trump’s decision came after Canada implemented a new digital services tax on technology companies, with the first round of payments due Monday, June 30th.

Consumer crosscurrents

Published June 26, 2025

What’s your read on the health of the US consumer?

Nik Modi: We’ve been cautious, and last earnings season confirmed consumer strain. They’re grappling with lingering inflation, job pressures, lower savings, rising debt—and now tariffs. February marked a significant pullback, and many categories remain soft.

Steve Shemesh: Consumers have shown more resilience than expected, but balance sheets are being drawn down. Tariffs and global instability have made them cautious, especially on discretionary items. Unless tariffs reverse materially, we see a slow deceleration in spending.

Who’s most exposed to tariffs, and how are companies responding?

Nik Modi: Everyone’s exposed to some degree, but those with China exposure are hit hardest. CPG companies are turning to productivity gains to offset costs. Pricing is hard to push through and risks further volume loss.

Steve Shemesh: Many companies in our coverage source overseas, creating risk—especially in furniture, home furnishings, and general merchandise. We expect more diversified sourcing, cost-cutting (including AI tools), and some price hikes.

30-day deadline

Published June 17, 2025

Canada and the U.S. are eyeing a trade deal in 30 days. A statement from the Canadian side announced the deadline after U.S. President Donald Trump and Prime Minister Mark Carney met on the sidelines of the G7 summit in Kananaskis, Alberta. The White House has not issued a statement. The readout from the Canadian side noted that the leaders also spoke about collaborating on priorities like critical minerals, illegal drugs, border security, and co-operation on defence. Trump has left the G7 meeting early to address the Middle East crisis

Canadian firms are looking beyond the U.S. for growth. Two-way cargo traffic with China surged 77% over the past few months, according to Port of Montreal data. China is now the port’s second-largest export market after India, up from fifth place last year, statistics show. Cargo volumes from Montreal to Spain surged 147% and 10% with the Netherlands, while two-way trade with African and South American countries was also on the up. While overall cargo volumes dipped 2%, container tonnage rose 14% in May compared to the same period last year.

FOMC Preview: Wait-and-see – now with dots!

Published June 16, 2025

We expect yet another quiet FOMC meeting this week, with little changes to the statement, dots, or Powell’s language, and their overall “wait and see” stance still intact. The data (and the trade policy outlook) since the Fed last met have moved in a slightly dovish direction on net, but we would heavily emphasize the word “slightly”.

Labor market data certainly shows a continued cooling relative to last year, and the recent trends in claims and payroll revisions are worth keeping an eye on, but none of the data has shown the type of deterioration that would be needed to override the Fed’s concerns about upside inflation risks.

We continue to see a first cut at the September meeting, with 25bp cuts at each subsequent meeting until May 2026 (i.e. terminal rate at 2.75%-3.00%). The risks around that call are skewed towards later.

While not our base case, the biggest market risk would likely come from a hawkish shift in the 2025 median dot.

To access the full report, contact your RBC representative.

The U.S. and China have a tentative deal

Published June 12, 2025

Beijing’s agreement to temporarily restore rare-earth licences was one of the major breakthroughs in its latest round of intense trade talks in London. But the reportedly six-month limit illustrates how Beijing wants to hold certain aces up its sleeves if tensions flare up again with Washington. In return, the U.S. agreed to relax restrictions on products such as jet engines and ethane, a vital component to make plastics. Market reaction was muted as details on the agreement were limited.

U.S. inflation and Canadian industry sales for May

Published June 6, 2025

Economic data in the coming week will continue to highlight on how trade disruptions in its early stages are impacting the Canadian and U.S. economies.

Inflation reports in the U.S. so far have failed to show the impact of tariffs on consumer prices. Core goods inflation in April was the first positive yearly reading since December 2023, mostly due to larger monthly increases earlier this year with a relatively subdued 0.06% month-over-month rise in April.

Nevertheless, tensions are brewing. Read more.

US jobs report: Trade headwinds have yet to derail services payroll growth

Published June 6, 2025

This morning’s nonfarm payroll report came in above consensus for May (+139K). The unemployment rate held steady yet again in May at 4.2%. A slew of retirements resulted in a lower labor force participation rate (down to 62.4% from 62.6%).

It was evident in this morning’s print that tariff uncertainty has yet to meaningfully grind payroll growth lower, with the impact of the current policy backdrop on employment limited to trade-reliant sectors. Manufacturing and retail suffered from an environment in which businesses and consumers remain in limbo, paralyzed by uncertainty. But services activity continues to drive payroll growth forward at a pace that is supported by demographic tailwinds.

We continue to highlight the dissonance between cyclical and structural themes. While monthly trends remain robust, the current trade situation (if it remains status quo) will translate to job losses later this year, which we expect to nudge the unemployment rate up near 4.5%.

Read the full report to find out what else stood out to us in the May data.

Trade talks: PM Carney speaking to Trump, U.S. reengages China

Published June 6, 2025

Mark Carney and Donald Trump have been talking directly on trade. The two leaders have been "laying out the perimeters" of a trade and security deal, Peter Hoekstra, the U.S. Ambassador to Canada, confirmed. An agreement could come by September—without CUSMA member Mexico. Sources told CBC/Radio-Canada that Ottawa is hoping to land a deal in time for the G7, being held in Alberta in mid-June. The news comes as Canada’s trade deficit hit a record high $7.1 billion, led by a 15.7% decline in exports to the U.S.

U.S. and China to revive trade talks. Following a "very good" 90-minute call with China's President Xi Jinping, Donald Trump announced that the two trade-warring nations would soon get back to the table. In recent weeks, Washington and Beijing have accused the other of violating the terms agreed upon in Geneva in May, a truce that lowered the triple-digit tariffs each had levied on the other for 90 days. The recent escalation was focused largely on access to critical minerals from China and new U.S. restrictions on computer chips.

Three questions with RBC’s VP of Trade Finance

Published May 30, 2025

Q: How are Canadian businesses diversifying—both in terms of sourcing and selling?

A: Two key observations: In April, we had a record number of customers and prospective new users of our RBC Global Connect tool, which provides resources such as best countries to buy and sell and other trade intelligence. Secondly, some clients have found better margin opportunities in Europe for products historically shipped to the U.S. And importers are ensuring resiliency of supply by finding new suppliers.

Q: How have things changed in the past couple of months for companies that have maintained their business with U.S. customers?

A: Compliance with CUSMA rose to 50% in March from 33% in February. From client discussions, we expect this will be much higher now based on the noted estimate that 94% Canadian exports to U.S. are likely to comply. Clients have maximized U.S. inventory storage and distribution channels to meet short-term demand and minimize tariff impacts. They are also regularly reviewing timing of shipments and location of delivery to navigate U.S. tariffs. Some clients have been able to pass on higher tariff costs where alternative supply is unavailable, and demand persists. Others are pausing transactions to ensure certainty of pricing and demand, especially if they can’t cover tariff costs.

Q: What advice do you have for companies navigating the uncertainty?

A: We are encouraging clients to review their key buyer and seller trade cycle—order to payment, contract terms and documentation available—and identify opportunities to renegotiate terms. The aim is to maintain long-term relationships and avoid Back-to-School, Black Friday, and Christmas peak sales cycles disruptions. There are a range of solutions available to minimize payment risk, improve cash flow and enable cost/ return efficiencies as new markets, suppliers and buyers are being considered.

Click here to read more from this week’s edition of “The Trade Zone”.

RBC U.S. Equity Capital Markets tariff update

Published May 26, 2025

New tariff threats loom, with President Trump threatening a 50% tariff on the EU and a 25% tariff on Apple. The U.S. dollar dropped to its lowest level since December 2023, making it clear that headline risk and volatility remain. Additionally, the global macro and geopolitical backdrop is volatile, with tensions between Iran and the U.S. at highs at their fifth round of negotiations this week.

On Thursday, May 22nd, the House narrowly passed Trump’s tax bill and will advance to the Senate subject to changes and delays once there. The bill covers topics of tax reform, immigration policy, and spending cuts. If implemented, the bill would make the tax cuts during Trump’s first term permanent. Notable changes would be tax cuts for businesses and wealthy individuals, and the installation of work requirements for food assistance and medical insurance. The market is bracing for the future impact if the bill passes, as the yield on 30-yr Treasury bonds spiked to above 5%.

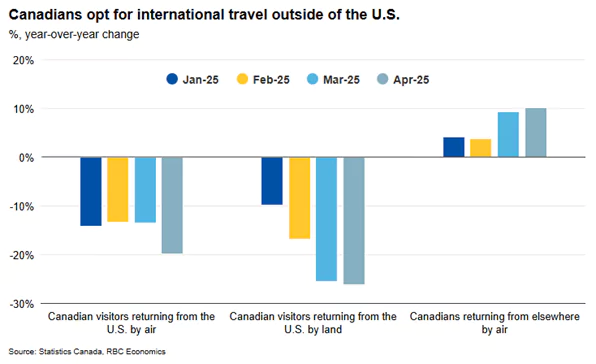

Trade tensions are redrawing Canadians’ travel map

Published May 26, 2025

The decline in U.S. travel isn’t unique to Canada. Arrivals to the U.S. from countries other than Canada and Mexico fell from a 5% increase in January to a 1.6% decline over March and April. Most of that drop come from fewer Asian and Western European visitors.

International travel spending falls under the services trade. When foreigners travel and spend in the U.S., those expenditures become services exports. Expenditures from Americans traveling and spending abroad are then considered services imports.

Lower demand for travel to the U.S. means fewer travel dollar collected. That will shrink total U.S. exports and slow gross domestic product growth (if there aren’t major changes in Americans traveling abroad). But, the impact will be marginal since tourism accounts for a relatively small share of the U.S. economy.

More significantly, it will widen the overall trade deficit—the opposite of what the current U.S. administration is trying to achieve through import tariffs.

Bloomberg Brief: Bond market warns of swelling deficit

Published May 22, 2025

Amy Wu Silverman, Head of Derivatives Strategy at RBC Capital Markets, joined Bloomberg Brief to discuss the potential impact of Trump’s tax bill and looming tariff developments on the market, how fixed income is driving the equities trade right now and more.

Click here to watch Amy in action (24:28).

Trade deal with China won’t get inflation back to target

Published May 12, 2025

The Trump administration announced an agreement with China, lowering tariffs on U.S. exports to China while maintaining a baseline tariff on U.S. imports from China. Importantly it set a path for future negotiations, reducing the risk of further retaliatory actions.

As part of the announcement, effective May 14, both countries will lower tariffs by 115%. The U.S. will slash a staggering 145% tariff burden on Chinese imports down to 30%, a drastic tariff de-escalation that rippled across global markets. By our estimate, this significantly lowers the average effective U.S. tariff rate to 13% from our previously estimated 24%. Still, this announcement does little to help get inflation’s path back to 2% as a 13% effective tariff rate is still nearly 5 times higher than the 2.4% rate seen in 2024.

For now, these are the three core economic takeaways:

- The uncomfortable truth remains – inflation will continue to run above target. The Fed’s 2% target will remain elusive as the passthrough of higher tariffs to consumers remains a risk.

- Uncertainty will persist as trade policy remains subject to revised agreements over the next 90 days. In this uncertain environment, economists have to run multiple scenarios at any given time given the rapid evolution of trade policy.

- We are not out of the woods yet and growth will likely remain sluggish in 2025. For now, we expect the U.S. economy will continue to see below-trend growth throughout 2025. We expect higher prices for goods will weigh on consumer behavior and job losses remain a risk in trade related sectors like retail, wholesale, transportation and warehousing. We do expect some degree of substitution to take place.

Present Trump’s EO unlikely to rattle U.S. biopharma sector

Published May 12, 2025

This morning, President Trump issued the anticipated executive order (EO) on his most favored nation (MFN) pricing policy. Significant uncertainties remain, including implementation challenges due to historical legal hurdles, limited authority to Medicare (and possibly Medicaid), and undisclosed ex-U.S. prices/discounts. The vague language directing HHS to propose target drug prices and consider direct-to-consumer sales or re-importation may not be feasible or have minimal impact on biopharma companies.

The conference's tone appeared much more punitive towards "freeloading" EU countries than to biopharmas, as President Trump hopes to empower biopharmas to bring ex-U.S. drug prices closer to U.S. levels, though the EO does incorporate threats of FDA withdrawal for non-complicit drug companies (though this would be difficult to carry out).

Surprisingly, there were no specifics on if/how MFN could apply to Medicare pricing, such as through a CMMI test model or the IRA negotiation framework. With Medicaid cuts reportedly excluding MFN, the impact on Medicaid may be less than anticipated. However, drug pricing headlines may persist as this and related policies unfold.

Overall, we see reason for relief in the sector alongside improving FDA clarity and limited tariff risk.

For more information on this report, please contact your RBC representative.

Inflation prints expected to be benign on tariff holdout

Published May 9, 2025

Next week promises a whirlwind of economic indicators, headlined by Tuesday's closely watched inflation report. Last month, we stated that it was too soon to see the impact of tariffs show up in the inflation prints — with the 90-day pause on tariffs until early July, this is still largely true. But we do expect to see early signs of slight price-acceleration in specific sectors.

- Tariffs on steel and aluminum and autos are expected to nudge new car prices slightly higher alongside motor vehicles and parts.

- China-exposed categories—particularly apparel, communications equipment, and personal care goods—are similarly vulnerable to price acceleration.

Against this backdrop, we anticipate core inflation will tick up 0.2% m/m, pushing the y/y pace to 2.8% in April. Our headline inflation forecast maintains a 0.2% m/m increase, as retreating natural gas prices likely counterbalanced modest increases in food and fuel costs.