Similar to past years, participants included representatives from the Canadian Federal Government, federal agencies, provincial issuers, non-agent crown issuers, municipal issuers, offshore SSA maple issuers, and institutional investors.

The discussions focused on the current economic environment in Canada, trends in borrowing by public sector issuers in 2023 and expectations for 2024. This publication summarizes these conversations along with key insights and takeaways from issuers and investors in the Canadian public sector. We thank all the participants who dedicated the time to share their views and experiences.

Canadian Borrowers Roundtable - Full Report

Public Sector Issuers Roundtable Report

1. Economic Growth Expected to Slow:

The combination of high rates and household leverage is having the expected effect of depressing economic activity. The question is about the degree of weakness, not the direction of travel; a spontaneous growth rebound is highly unlikely until there is a catalyst (i.e. easing financial conditions or a positive fiscal impulse). RBC growth forecasts assume a shallow recession and below trend growth persisting through 2024. Risks are skewed to a hard landing which could involve either: (i) an unforeseen shock related to crisis/liquidity or (ii) a classic deep growth recession from underestimating the impact of tighter policy on rate sensitive sectors.

2. Inflation

Inflation should moderate gradually alongside slack in the product and labour markets, but there are question marks on how quickly this will occur. If the Bank of Canada is correct and the economy is entering excess supply, coupled with further loosening in labour market conditions, downward forces on inflation should become more acute and push towards the Bank’s target zone. RBC Economics expects headline inflation to reach 1.5% by end of 2024 and core inflation to subside toward the BoC 2% target. The risk scenario is slanted to prices remaining elevated. Current wage trends are inconsistent with inflation reaching target. Similarly, corporate pricing behavior and inflation expectations continue to be higher than normal. These combine to give a higher risk that elevated inflation becomes embedded.

3. Bank of Canada starts cutting rates in 2024

The RBC Rates Strategy team’s base case for monetary policy in Canada projects 100bp of interest rate cuts in 2024 starting in late Q2, followed by another 100bp in 2025. The memory effect of a policy error (tightening too late) combined with sticky inflation/wages should see the BoC hold off longer than in past cycles. With core inflation measures still stubbornly high, the BoC should remain on hold for a while.

4. Housing Market Challenges

The housing market is caught between opposing cyclical and structural forces. The cyclical impact from higher rates is decidedly negative: (i) housing affordability is problematic, (ii) debt servicing ratios will rise from lofty levels, and (iii) ongoing mortgage resets. However, the structural forces – immigration, land supply, housing shortage, insufficient multi-dwelling units – prevent a larger downturn. The outlook for housing would worsen if job losses became more widespread than the base case scenario. A prolonged period of stagnation in housing activity/prices is most likely.

5. Steady ESG Issuance with Increased Investor Focus

Canadian public sector ESG issuance volumes retraced to ~C$16.0 billion in 2023 after reaching a record high of C$22.7 billion in 2022. The Government of Canada did not issue in the ESG space in 2023. Canada however did update its Framework to include nuclear as a use of proceeds and is committed to being a regular issuer in the domestic green bond market. Public Sector ESG issuances represent the majority of total ESG issuance in CAD, consisting of 65% of the total CAD ESG issues. Provinces who have not yet issued an ESG bond emphasized that they would like to eventually embed ESG into all their programs, aiming to champion ESG with a holistic approach and not just for specific issuances that they complete. Issuers are also focused on the liquidity of the ESG bonds, with consideration of offshore ESG issuances if their program is large enough to be able to show commitment in those specific markets.

6. Overall Issuance Levels Expected to Grow in 2024

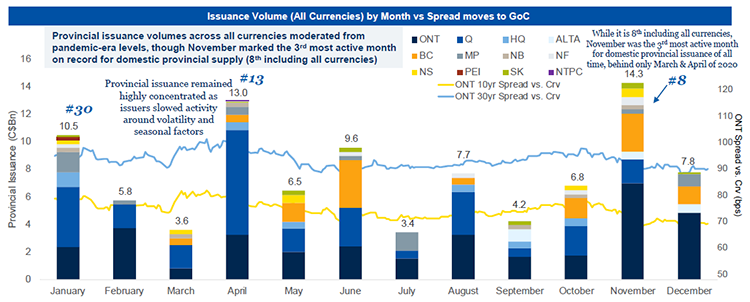

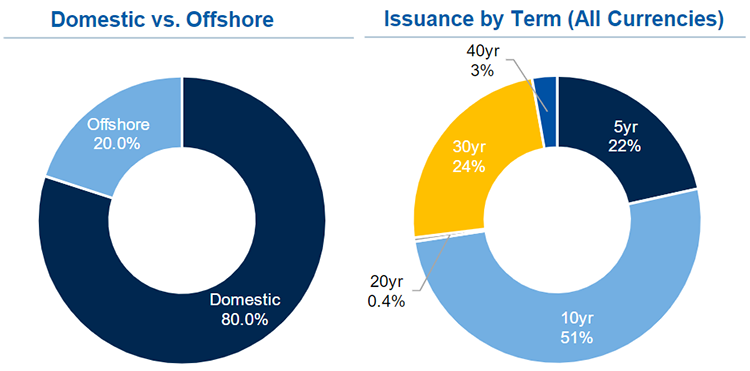

Issuance from Canadian Public Sector issuers totaled ~C$212.3 billion across all currencies in 2023, up 11.9% from the C$189.7 billion completed in 2022. C$150.0 billion (70.7%) of Public Sector Issuance was completed in the domestic market in 2023, a 10.0% increase from the C$136.5 billion (72.0% of total funding) in 2022. Provincial issuers completed C$93.0 billion in 2023 across all currencies, an increase of 14.1% from the C$81.5 billion seen in 2022 with the majority (80%) completed in the domestic market, in line with historical trends. The outlook for debt issuance by the Canadian public sector in 2024 is expected to be at a modestly higher level to the volume seen in 2023 given: (i) provinces are expected to increase borrowing to address higher fiscal deficit and capital spending needs; (ii) the expansion of the Canada Mortgage Bond (CMB) program to C$60.0 million in 2024; and (iii) expectations of continued growth in the borrowing programs for the pension asset manager/pension fund sector.

7. Heightened Risk of a Weakening of Credit Spreads in 2024

The prospect of increased issuance levels combined with a scenario where economic growth deteriorates and/or there is some type of risk-off event in financial markets tilts the balance of risks towards the potential for a weakening of credit spreads in 2024. Conversely, an economic soft-landing scenario combined with stable and positive tone in credit markets would be expected to be supportive for spread product in the year ahead.

8. International Markets Expected to Remain a Key Component of Financing

Offshore issuance was up 17% year-over-year in 2023 with the Canadian SSA sector (incl. GoC) completing C$43.7 billion equiv. or 72% of its funding in offshore markets, while provincial issuers completed C$18.6 billion equiv. (20%) outside of Canada, for aggregate offshore public sector supply of C$62.3 billion equiv. Provincial issuers noted that they are still committed to issuing in core international markets (USD/EUR/GBP) to diversify their funding base and will continue to actively monitor relative financing levels for offshore issuance opportunities in 2024. Pension Fund/Pension Asset Manager issuers also remain committed to finding strong execution opportunities in offshore markets like USD, EUR and AUD in 2024.

SSA Maple Roundtable Report

Download1. Steady Funding Programs and Diversification in Currencies

SSA Funding requirements remained mostly steady in 2023 compared to the year prior and issuers were able to navigate the continued challenging conditions of ongoing market volatility and central bank rate hikes. Market participants noted the underperformance of EUR relative to USD in late 2023 and that such continued underperformance has the potential to impact funding strategy in 2024. However, they remain focused on a diversified funding strategy which includes markets away from their core currencies of USD and EUR and would also seek to push for duration where possible.

2. Market Volatility and Investor Demand

Navigating a volatile market backdrop in 2023, SSA issuers tended to rely on their home currencies for most of their funding. While currency diversification remains a common goal, the final currency mix of SSA issuers’ funding programs were ultimately determined by investor demand as well as cost of funds. In addition, more challenging execution conditions and timing constraints around central bank events and economic data releases made for narrower and more crowded issuance windows.

3. ESG Themed Bonds Driven by Investor Demand

ESG issuance continues to be favored among Maple SSA issuers and investors in the Canadian market; 13 out of the 16 benchmark CAD SSA transactions in 2023 have been in ESG format, ranging across Gender, Green, Health, Sustainable and Social bonds, and issuers noted that the space has also reached maturity in Europe. Market participants noted that they have a healthy pipeline of ESG projects that could support further themed bond issuance as well as sustainability-linked offerings.

4. Maple SSA Issuance Saw a Record High in 2023

The CAD Maple SSA primary market has seen an all-time high of C$10.0bn print across 16 transactions in 2023, a 61% increase from 2022 (C$6.2bn). Bank Treasuries remain the most active investor type in the Canadian Maple SSA primary market (~40% in 2023), with Central Banks / Official Institutions increasing from previous years driven by relative value to CMBs. Issuers were also able to extend duration in 2023 as the average maturity of new CAD SSA Benchmarks in 2023 was 4.5-years, up from the 3.7-years seen in 2022.

Municipal Treasurers Roundtable Report

1. Cautious Outlook

Municipalities are approaching the 2024 budget planning process with higher inflation cost, affordable housing and social services expense top of mind. 2023 spendings have been generally on track with anticipation of a modest FY surplus. Ridership surprised on the upside which boosted revenue, though how to fund affordable housing under higher inflation driven costs remains a major concern into 2024. The uncertainty on Bill 23’s trajectory continues to pose additional burden for the municipalities.

2. Inflation Cost

The most critical factors on the operating side are cost inflation and expense related to social programs, which persisted throughout 2023 and are expected to continue into 2024. Development expense, facility operation and maintenance costs have risen significantly due to surging inflation. Furthermore, Social services such as police and fire department also experienced heightened demand fueled by a combination of mental health issue, addiction and homelessness.

3. Housing

Affordable housing has remained a focal point this year with persistent gap between buyer and seller pricing expectations. In response, municipalities have boosted their investments in housing -related infrastructure during 2023 to meet affordable housing goals. However, as inflation eroded purchasing power, municipalities are seeking additional funding from senior government for a more comprehensive housing accountability structure. The municipalities foresaw a positive trajectory as all 3 levels of governments are concentrating their efforts on this issue.

4. Transit

Transit fare revenue has been the most variable compared to budget. Ridership surpassed expectations in 2023 and even exceeded pre-covid level in some regions, generating extra revenue which provided additional financial flexibility. This momentum is expected to carry into 2024 on the back of population growth. Meanwhile, parking revenue remains below pre-covid level. The municipalities are also developing housing alongside transit hubs to enhance efficiency and support expansion demands.

5. Borrowing Program

Canadian municipalities continue to offer investors attractive value relative to other government credits as local governments must balance their operating budgets. There was a total of C$2.8 billion Canadian municipal issuance in 2023, moderated from the C$4.4 billion in 2022 and the record high of C$5.9 billion in 2021. Issuers sidelined under rising interest rate environment and sufficient pre-funding during covid. Large Canadian municipal issuers are expected to continue to focus on 10-year, 20-year, and 30-year bullet maturity issuance, while smaller municipal issuers are expected to issue via 1-10 year and 1-20 year serial debenture issuance.

6. ESG

ESG continues to be an integral part of the business for municipalities given the nature of the funded capital projects. While some issuers have issued labeled sustainable bonds, others aspire to potentially issue these in the future. The Sustainable bond issues were very well received and while the pricing benefit was marginal given the challenging market backdrop globally, the demand from investors with specific ESG mandates was instrumental in the success of these transactions.

In addition, we encourage you to view the RBC Government Finance Public Sector Debt Market update that is published monthly. The December 2023 edition includes a year-end recap of issuance trends by the Canadian governments in 2023.

- 2023 saw C$150 billion of domestic funding across all public sector issuers which represents an increase of 10% from the C$136.5 billion seen in 2022

- Issuance across all sectors and currencies meanwhile reached C$212.3 billion in 2023, 12% above levels seen in 2022

- Canadian SSA volumes reached C$60.4 billion equiv., ~4% higher than the C$57.9 billion equiv. seen in 2022 and marked the most active year on record

- Maple SSA reached their most active year on record at C$10.1 billion, up 63% from the C$6.2 billion seen in 2022

- Public Sector ESG issuance in 2023 reached ~C$15.9 billion, ~43% behind the C$22.7 billion priced in 2022

Source: RBC Capital Markets as at December 29, 2023

Government Finance Public Sector Debt Market update

Contact info:

RBCCM Government Finance

RBCCMGovernmentFinance@rbccm.com

416-842-7756