Royal Bank of Canadahttps://www.rbcroyalbank.com/personal.htmlhttps://www.rbcroyalbank.com/personal.htmlInsights1200630enCA

Datum[@Name='Source DCR']

2020-05-26New business models emergeWill genetics usher in a new era of healthcare? Is the entire health ecosystem ready for reinvention? Can digital healthcare in life sciences exceed patient expectations?Expanding Ecosystems3/assets/rbccm/images/gib/healthcare/article_3_thumbnail_sm.jpg/assets/rbccm/images/gib/healthcare/article_3_thumbnail.jpg<h3>Shifting Paradigms</h3>

<p>As the convergence of healthcare and technology has accelerated, new business models are rapidly emerging. </p>

<p>In the traditional biopharma model, the customer would be a physician, R&D tools would be chemical or biological, the end product a pill or vial, and the competitors pharma and biotech players.</p>

<p>The digital revolution in healthcare is shifting this long-established paradigm. Today, biopharma companies’ customer groups have grown to include patients of all ages, providers and payers—all equipped with smartphones and apps that generate a vast amount of digital information to empower their decision-making. R&D has added genetic information and digital capability to its toolset. The end product has broadened beyond the pill to include health outcomes enabled by digital devices and therapeutics. And the competitive set has seen the addition of technology players, including consumer-focused apps and online services, as well as digital health and digital therapeutics firms.</p>

<p class="photo-frame text-center"><img style="width: 100%;" src="/assets/rbccm/images/gib/healthcare/Healthcare-Article-3-Graph-1.png" alt="" /></p>

<h3>A Changing Ecosystem</h3>

<p>Indeed, digital and AI applications are radically changing key areas of the biopharma ecosystem and how patients manage their healthcare.</p>

<p>In pre-clinical research, technology is enabling everything from a deeper mining of literature, to predictive modeling and gene-function annotation. Digital apps are simulating molecular dynamics and pushing the limits of cellular imaging.</p>

<p>In clinical trials, digital transformation is helping to automate testing procedures, build global patient databases and collect real-world data.</p>

<p>In diagnostics, tech powers digital pathology, home-based body diagnosis, and computational analysis of tissue arrays. Just like your car leaves the factory with hundreds of sensors that can trigger the check engine light, humans will have wearable and/or implantable sensors to alert them when something is not functioning properly. Another burgeoning area is immune cell monitoring and digital analysis through just a finger prick.</p>

<p>At the point of patient care, digital applications are already delivering virtual consultations, remote monitoring, VR-based cognitive therapy and digital Rx. Demand for telehealth services and health-based social platforms is also increasing and especially vital in a world facing new challenges such as the COVID-19 pandemic.</p>

<p><img src="/assets/rbccm/images/gib/healthcare/healthcare-article-3-graph-2.png" alt="AI and Digital applications are changing key areas of the Healthcare Ecosystem" /></p>

<div id="similar-to-this" style="border-top: 2px #E6E6E7 dotted; border-bottom: 2px #E6E6E7 dotted; margin: 35px 0; padding: 25px;">

<h4 style="font-size: 18px; letter-spacing: 0.5px; border-bottom: 3px #FEDF01 solid; padding: 0 0 8px 0; margin-bottom: 15px;">Similar to this</h4>

</div>

<h3>Digital Transformation</h3>

<p>The digital revolution presents both threats and opportunities to incumbent biopharma companies. Tech is powering efficiencies in all stages of the current ecosystem and is also enabling healthcare providers to expand their capabilities from treatment to prevention.</p>

<div class="quotebox">

<p>“Tech is powering efficiencies in all stages of the current ecosystem and is also enabling healthcare providers to expand their capabilities.”</p>

<p class="attribution" style="color: #0070a3;">– Greg Wiederrecht, Ph.D.</p>

<div class="quote-share">

<p style="display: inline-block;"><span style="margin-right: 15px;">Share </span><a class="blue-circle-outline-sm" href="https://www.linkedin.com/shareArticle?mini=true&url=https%3A//www.rbccm.com/en/gib/healthcare/episode/new_healthcare_business_models_emerge&title=New%20healthcare%20business%20models%20emerge&source=www.rbccm.com" target="_blank" rel="noopener" aria-label="Connect by LinkedIn"><em class="fa fa-linkedin" style="color: #0051a5; margin-left: 3px;"> </em></a> <a class="blue-circle-outline-sm" href="https://twitter.com/home?status=New%20business%20models%20emerge%20https%3A//www.rbccm.com/en/gib/healthcare/episode/new_healthcare_business_models_emerge" target="_blank" rel="noopener" aria-label="Connect by X"><em class="fa fa-twitter" style="color: #0051a5; margin-left: 3px;"> </em></a> <a class="blue-circle-outline-sm" href="mailto:?subject=New%20business%20models%20emerge&body=I%20found%20this%20insights%20piece%20from%20RBC%20Capital%20Markets%20informative%20and%20thought%20it%20might%20be%20of%20interest%20to%20you%3A%0D%0Dhttps%3A//www.rbccm.com/en/gib/healthcare/episode/new_healthcare_business_models_emerge&title=New business models emerge" aria-label="Connect by Email"><em class="fa fa-envelope" style="color: #0051a5; margin-left: 3px;"> </em></a></p>

</div>

</div>

<p> </p>

<p>The increased digitization of human experiences gives access to a wealth of information and knowledge that could help intervene before disease has a chance to strike. A prime example of this is collating data from an Apple Watch to screen for irregular heart rhythms and detect undiagnosed atrial fibrillation. At the other end of the spectrum, digital transformation allows a completely new class of therapies such as digital therapeutics to support specific disorders.</p>

<p>McKinsey and Company’s international survey shows that more than 75% of patients expect to use digital healthcare services in the future.<sup>1</sup> Patients are seeking technology that delivers a level of care they can rely on and trust. Ultimately, the aim of the digital revolution is to develop healthier societies and lower the cost of care.</p>

<p style="word-wrap: break-word;"><sup>1 Source: McKinsey and Company, Healthcare’s Digital Future, July 2014. https://www.mckinsey.com/~/media/McKinsey/Industries/Healthcare%20Systems%20and%20Services/Our%20Insights/Healthcares%20digital%20future/Healthcares%20digital%20future.ashx</sup></p><ul>

<li>Customer groups, R&D and competitors are all rapidly expanding</li>

<li>Tech is reinventing every facet of the biopharma ecosystem</li>

<li>Innovations in patient care is driving adoption of digital services</li>

</ul>text2 min1 minHealthcare Models, Digital Healthcare, Digital Healthcare Apps, Digital Health Diagnostics, Expanding R&D, Healthcare & Tech Convergence, Healthcare Services, Clinical Trials, Remote Patient Monitoring, Digital Therapeutics, Biopharma ecosystem, Cost of CareN/templatedata/rbccm/episode/data/healthcare/amazon_cvs_and_google_healthcare_reimagined/templatedata/rbccm/episode/data/healthcare/big_tech_vs_big_pharma/templatedata/rbccm/episode/data/healthcare/the_healthcare_data_explosionGreg Wiederrecht, Ph.D./assets/rbccm/images/gib/healthcare/greg-wiederrecht.jpgManaging Director, Healthcare Investment Bankinggreg.wiederrecht@rbccm.comhttps://www.linkedin.com/in/gregwiederrecht/Sasson Darwish/assets/rbccm/images/gib/healthcare/sasson-darwish.jpgManaging Director, AI, Analytics and IoT & Israel Country Coverage, Global Technology Investment Bankingsasson.darwish@rbccm.com https://www.linkedin.com/in/sassdarwish/Andrew Callaway/assets/rbccm/images/gib/healthcare/andrew-callaway.jpgManaging Director, Global Head of Healthcare Investment Bankingandrew.callaway@rbccm.comhttps://www.linkedin.com/in/andrew-cal-callaway

DEBUG: DCR

DCR

Royal Bank of Canadahttps://www.rbcroyalbank.com/personal.htmlhttps://www.rbcroyalbank.com/personal.htmlInsights1200630enCA

DCR

2020-05-26New business models emergeWill genetics usher in a new era of healthcare? Is the entire health ecosystem ready for reinvention? Can digital healthcare in life sciences exceed patient expectations?Expanding Ecosystems3/assets/rbccm/images/gib/healthcare/article_3_thumbnail_sm.jpg/assets/rbccm/images/gib/healthcare/article_3_thumbnail.jpg<h3>Shifting Paradigms</h3>

<p>As the convergence of healthcare and technology has accelerated, new business models are rapidly emerging. </p>

<p>In the traditional biopharma model, the customer would be a physician, R&D tools would be chemical or biological, the end product a pill or vial, and the competitors pharma and biotech players.</p>

<p>The digital revolution in healthcare is shifting this long-established paradigm. Today, biopharma companies’ customer groups have grown to include patients of all ages, providers and payers—all equipped with smartphones and apps that generate a vast amount of digital information to empower their decision-making. R&D has added genetic information and digital capability to its toolset. The end product has broadened beyond the pill to include health outcomes enabled by digital devices and therapeutics. And the competitive set has seen the addition of technology players, including consumer-focused apps and online services, as well as digital health and digital therapeutics firms.</p>

<p class="photo-frame text-center"><img style="width: 100%;" src="/assets/rbccm/images/gib/healthcare/Healthcare-Article-3-Graph-1.png" alt="" /></p>

<h3>A Changing Ecosystem</h3>

<p>Indeed, digital and AI applications are radically changing key areas of the biopharma ecosystem and how patients manage their healthcare.</p>

<p>In pre-clinical research, technology is enabling everything from a deeper mining of literature, to predictive modeling and gene-function annotation. Digital apps are simulating molecular dynamics and pushing the limits of cellular imaging.</p>

<p>In clinical trials, digital transformation is helping to automate testing procedures, build global patient databases and collect real-world data.</p>

<p>In diagnostics, tech powers digital pathology, home-based body diagnosis, and computational analysis of tissue arrays. Just like your car leaves the factory with hundreds of sensors that can trigger the check engine light, humans will have wearable and/or implantable sensors to alert them when something is not functioning properly. Another burgeoning area is immune cell monitoring and digital analysis through just a finger prick.</p>

<p>At the point of patient care, digital applications are already delivering virtual consultations, remote monitoring, VR-based cognitive therapy and digital Rx. Demand for telehealth services and health-based social platforms is also increasing and especially vital in a world facing new challenges such as the COVID-19 pandemic.</p>

<p><img src="/assets/rbccm/images/gib/healthcare/healthcare-article-3-graph-2.png" alt="AI and Digital applications are changing key areas of the Healthcare Ecosystem" /></p>

<div id="similar-to-this" style="border-top: 2px #E6E6E7 dotted; border-bottom: 2px #E6E6E7 dotted; margin: 35px 0; padding: 25px;">

<h4 style="font-size: 18px; letter-spacing: 0.5px; border-bottom: 3px #FEDF01 solid; padding: 0 0 8px 0; margin-bottom: 15px;">Similar to this</h4>

</div>

<h3>Digital Transformation</h3>

<p>The digital revolution presents both threats and opportunities to incumbent biopharma companies. Tech is powering efficiencies in all stages of the current ecosystem and is also enabling healthcare providers to expand their capabilities from treatment to prevention.</p>

<div class="quotebox">

<p>“Tech is powering efficiencies in all stages of the current ecosystem and is also enabling healthcare providers to expand their capabilities.”</p>

<p class="attribution" style="color: #0070a3;">– Greg Wiederrecht, Ph.D.</p>

<div class="quote-share">

<p style="display: inline-block;"><span style="margin-right: 15px;">Share </span><a class="blue-circle-outline-sm" href="https://www.linkedin.com/shareArticle?mini=true&url=https%3A//www.rbccm.com/en/gib/healthcare/episode/new_healthcare_business_models_emerge&title=New%20healthcare%20business%20models%20emerge&source=www.rbccm.com" target="_blank" rel="noopener" aria-label="Connect by LinkedIn"><em class="fa fa-linkedin" style="color: #0051a5; margin-left: 3px;"> </em></a> <a class="blue-circle-outline-sm" href="https://twitter.com/home?status=New%20business%20models%20emerge%20https%3A//www.rbccm.com/en/gib/healthcare/episode/new_healthcare_business_models_emerge" target="_blank" rel="noopener" aria-label="Connect by X"><em class="fa fa-twitter" style="color: #0051a5; margin-left: 3px;"> </em></a> <a class="blue-circle-outline-sm" href="mailto:?subject=New%20business%20models%20emerge&body=I%20found%20this%20insights%20piece%20from%20RBC%20Capital%20Markets%20informative%20and%20thought%20it%20might%20be%20of%20interest%20to%20you%3A%0D%0Dhttps%3A//www.rbccm.com/en/gib/healthcare/episode/new_healthcare_business_models_emerge&title=New business models emerge" aria-label="Connect by Email"><em class="fa fa-envelope" style="color: #0051a5; margin-left: 3px;"> </em></a></p>

</div>

</div>

<p> </p>

<p>The increased digitization of human experiences gives access to a wealth of information and knowledge that could help intervene before disease has a chance to strike. A prime example of this is collating data from an Apple Watch to screen for irregular heart rhythms and detect undiagnosed atrial fibrillation. At the other end of the spectrum, digital transformation allows a completely new class of therapies such as digital therapeutics to support specific disorders.</p>

<p>McKinsey and Company’s international survey shows that more than 75% of patients expect to use digital healthcare services in the future.<sup>1</sup> Patients are seeking technology that delivers a level of care they can rely on and trust. Ultimately, the aim of the digital revolution is to develop healthier societies and lower the cost of care.</p>

<p style="word-wrap: break-word;"><sup>1 Source: McKinsey and Company, Healthcare’s Digital Future, July 2014. https://www.mckinsey.com/~/media/McKinsey/Industries/Healthcare%20Systems%20and%20Services/Our%20Insights/Healthcares%20digital%20future/Healthcares%20digital%20future.ashx</sup></p><ul>

<li>Customer groups, R&D and competitors are all rapidly expanding</li>

<li>Tech is reinventing every facet of the biopharma ecosystem</li>

<li>Innovations in patient care is driving adoption of digital services</li>

</ul>text2 min1 minHealthcare Models, Digital Healthcare, Digital Healthcare Apps, Digital Health Diagnostics, Expanding R&D, Healthcare & Tech Convergence, Healthcare Services, Clinical Trials, Remote Patient Monitoring, Digital Therapeutics, Biopharma ecosystem, Cost of CareN/templatedata/rbccm/episode/data/healthcare/amazon_cvs_and_google_healthcare_reimagined/templatedata/rbccm/episode/data/healthcare/big_tech_vs_big_pharma/templatedata/rbccm/episode/data/healthcare/the_healthcare_data_explosionGreg Wiederrecht, Ph.D./assets/rbccm/images/gib/healthcare/greg-wiederrecht.jpgManaging Director, Healthcare Investment Bankinggreg.wiederrecht@rbccm.comhttps://www.linkedin.com/in/gregwiederrecht/Sasson Darwish/assets/rbccm/images/gib/healthcare/sasson-darwish.jpgManaging Director, AI, Analytics and IoT & Israel Country Coverage, Global Technology Investment Bankingsasson.darwish@rbccm.com https://www.linkedin.com/in/sassdarwish/Andrew Callaway/assets/rbccm/images/gib/healthcare/andrew-callaway.jpgManaging Director, Global Head of Healthcare Investment Bankingandrew.callaway@rbccm.comhttps://www.linkedin.com/in/andrew-cal-callaway

12025-02-132024 Canadian Public Sector Issuers Roundtable SeriesRBC Capital Markets Government Finance team was pleased to facilitate three separate virtual Canadian Public Sector Debt Issuance roundtable discussions in late November and early December 2024.noneInsights<li><a href="/en/">Home</a></li><li><a href="/en/insights.page">Insights </a></li>Home | Insights/assets/rbccm/images/insights/2025/20250123-can-public-sector-th.jpg/assets/rbccm/images/insights/2025/20250123-can-public-sector-banner.jpghttps://www.rbccm.com/en/story/story.page?dcr=templatedata/article/story/data/2025/01/2024-canadian-public-sector-issuers-roundtable-seriesnone<p>Similar to past years, participants included representatives from the Canadian Federal Government, federal agencies, provincial issuers, non-agent crown issuers, municipal issuers, offshore SSA maple issuers, and institutional investors.</p>

<p>The discussions focused on the current economic environment in Canada, trends in borrowing by public sector issuers in 2024 and expectations for 2025. This publication summarizes these conversations along with key insights and takeaways from issuers and investors in the Canadian public sector. We thank all the participants who dedicated the time to share their views and experiences.</p>

<div id="accordion1" class="accordion" style="padding: 0;">

<div class="panel-group" aria-multiselectable="true">

<div class="accordion-item">

<div id="heading1" class="panel-heading">

<div class="panel-title"><a class="accordion-toggle collapsed" style="font-family: 'RBCDisplay',Georgia,Times,serif; font-size: 24px; line-height: 28px;" href="#collapse1" aria-controls="collapse1" aria-expanded="false" data-parent="#accordion1" data-toggle="collapse">Public Sector Roundtable Key Themes <!--<div class="fa fa-chevron-down rotate pull-right"></div>--> </a></div>

</div>

<div id="collapse1" class="panel-collapse collapse" style="height: 0px;" aria-labelledby="heading1" aria-expanded="false">

<div class="panel-body">

<div class="row" style="border: 1px solid #c4c8cc; margin: 0; margin-bottom: 20px;">

<div class="col-xs-4" style="display: inline-block; vertical-align: top; padding: 0;"><img class="alignleft size-full wp-image-23215" style="max-width: 100%;" src="/assets/rbccm/images/insights/2025/public-sector-roundtable-th.jpg" alt="Image of mountain for the Public Sector Issuers Roundtable Report"></div>

<div class="col-xs-8" style="display: inline-block; vertical-align: top; padding: 15px !important;">

<h3 style="margin-top: 5px;">Public Sector Issuers Roundtable Report</h3>

<!--<strong>Coming soon</strong> -->

<p><a class="btn btn-blue" title="Link to Public Sector Issuers Roundtable Report" href="/assets/rbccm/docs/insights/2025/public_sector_roundtable.pdf" target="_blank" rel="noopener noreferrer">Download</a></p>

</div>

</div>

<p><strong>1. Canada Outlook: economic growth, inflation, and Bank of Canada policy rate all to move lower in 2025:</strong> Growth is widely expected to underwhelm in 2025 as the effects of mortgage renewals, reduced immigration growth, and potential trade tariffs weigh on the general outlook</p>

<p><strong>2. U.S. Tariffs pose a looming challenge for the Canadian economy:</strong> The effects of trade tariffs and retaliatory measures pose a significant risk to the Canadian economy, casting a shadow of uncertainty on growth forecasts</p>

<p><strong>3. Declining immigration levels expected to provide relief on capacity pressures and contribute to lower growth:</strong> The plan to slow the growth in immigration levels is expected to be a headwind for economic growth, while allowing time to alleviate recent pressures on capacity. The effects of these policies will likely be felt over a number of years</p>

<p><strong>4. 2024 was a record year for domestic and offshore public sector debt issuance; the pace of issuance is expected to moderate in 2025:</strong> Canadian Public Sector issuance across all currencies reached C$288.0 billion in 2024, 36% higher than 2023 and a new record for aggregate issuance</p>

<p><strong>5. Year of firsts for Canadian public sector issuers:</strong> Canadian provinces issued a record C$51 billion equivalent in offshore markets; with many issuers expanding their borrowing programs into new currencies and tenors</p>

<p><strong>6. Credit spreads near the tights, is the trend sustainable?</strong> With global credit spreads at the tighter end of the range, risks are tilted towards a retracement in 2025</p>

<div style="background: #fee100; margin: 25px 0px; height: 4px; clear: both; max-width: 75px;"> </div>

</div>

</div>

</div>

<div class="accordion-item">

<div id="heading2" class="panel-heading">

<div class="panel-title"><a class="accordion-toggle collapsed" style="font-family: 'RBCDisplay',Georgia,Times,serif; font-size: 24px; line-height: 28px;" href="#collapse2" aria-controls="collapse2" aria-expanded="false" data-parent="#accordion1" data-toggle="collapse">SSA Maple Roundtable Key Themes</a></div>

</div>

<div id="collapse2" class="panel-collapse collapse" style="height: 0px;" aria-labelledby="heading2" aria-expanded="false">

<div class="panel-body">

<div class="row" style="border: 1px solid #c4c8cc; margin: 0; margin-bottom: 20px;">

<div class="col-xs-4" style="display: inline-block; vertical-align: top; padding: 0;"><img class="alignleft size-full wp-image-23215" style="max-width: 100%;" src="/assets/rbccm/images/insights/2025/ssa_maple_roundtable-th.jpg" alt="Image of mountain for the SSA Maple Roundtable Report"></div>

<div class="col-xs-8" style="display: inline-block; vertical-align: top; padding: 15px !important;">

<h3 style="margin-top: 5px;">SSA Maple Roundtable Report</h3>

<!--<strong>Coming soon</strong> -->

<p><a class="btn btn-blue" title="Link to SSA Maple Roundtable Report" href="/assets/rbccm/docs/insights/2025/ssa_maple_roundtable.pdf" target="_blank" rel="noopener noreferrer">Download</a></p>

</div>

</div>

<p><strong>1. Slightly Increased Funding Programs from Higher Disbursements<br></strong>SSA funding requirements saw a slight increase throughout 2024 compared to 2023 to reflect stronger disbursements, despite continued challenging conditions with geopolitical concerns and a various number of global elections towards the end of the year. Market participants noted challenging EUR markets and the expectation that the trend may persist in the new year. However, their focus remains in core currencies such as USD for Supranationals and EUR for European issuers, while continuing to seek for opportunities in other currencies where funding levels are attractive.</p>

<p><strong>2. ESG Themed Bonds Driven by Investor Demand<br></strong>ESG is still a main part of SSA funding programs globally. ESG issuance continues to be favored among Maple SSA issuers and investors in the Canadian market; all 4 benchmark CAD SSA transactions in 2024 have been in ESG format, ranging across Gender, Green, and Sustainable bonds. Issuers noted that they are continuing to the explore theme bonds, and that sustainability debt will continue to be a focal point for SSA issuers if there is a healthy pipeline of projects and sufficient investor interest.</p>

<p><strong>3. Awaiting the Right Timing To Return To the Maple Market<br></strong>Market participants value the CAD Maple market as a currency to diversify their funding program, however in 2024 due to swap level movements they have not been able to access the market for a prolonged period of time due to being offside versus their core funding currencies such as USD. All C$3.7 billion of the Maple supply in 2024 has been in the first 4 months of the year and quiet for the remainder of the year. SSA issuers remain positive about the CAD market, and noted if there are investor demand for longer dated issuances, they can go for duration if levels are attractive compared to their core funding levels.</p>

<p><strong>4. Forward Looking/Challenges<br></strong>Looking ahead to 2025, SSA issuers anticipate having to navigate higher funding costs, compressed issuance windows and competing supply across core issuance currencies. Market participants however are cautious but optimistic, and will continue to be nimble about their funding program heading into the new year.</p>

<div style="background: #fee100; margin: 25px 0px; height: 4px; clear: both; max-width: 75px;"> </div>

</div>

</div>

</div>

<div class="accordion-item">

<div id="heading3" class="panel-heading">

<div class="panel-title"><a class="accordion-toggle collapsed" style="font-family: 'RBCDisplay',Georgia,Times,serif; font-size: 24px; line-height: 28px;" href="#collapse3" aria-controls="collapse3" aria-expanded="false" data-parent="#accordion1" data-toggle="collapse">Municipal and Agency Roundtable <!--<div class="fa fa-chevron-down rotate pull-right"></div>--> </a></div>

</div>

<div id="collapse3" class="panel-collapse collapse" style="height: 0px;" aria-labelledby="heading3" aria-expanded="false">

<div class="panel-body">

<div class="row" style="border: 1px solid #c4c8cc; margin: 0; margin-bottom: 20px;">

<div class="col-xs-4" style="display: inline-block; vertical-align: top; padding: 0;"><img class="alignleft size-full wp-image-23215" style="max-width: 100%;" src="/assets/rbccm/images/insights/2025/municipal-agency-roundtable-th.jpg" alt="Image of mountain for the Municipal and Agency Roundtable Report"></div>

<div class="col-xs-8" style="display: inline-block; vertical-align: top; padding: 15px !important;">

<h3 style="margin-top: 5px;">Municipal and Agency Roundtable Report</h3>

<!--<strong>Coming soon</strong> -->

<p><a class="btn btn-blue" title="Link to Municipal and Agency Roundtable Report" href="/assets/rbccm/docs/insights/2025/muni_roundtable.pdf" target="_blank" rel="noopener noreferrer">Download</a></p>

</div>

</div>

<p><strong>1. Affordable Housing Remains the Most Significant Issue</strong> <br>The demand for affordable housing has been outpacing supply, largely driven by the immigration growth and place pressure on the City’s resources to deliver. This issue hit the hardest at the lowest income group, with a particularly large gap in housing supply for purpose built rental and community housing. Housing delivery continues to be a priority for all level of governments, there are various provincial and federal housing funds expected to be delivered in 2025 to meet housing starts targets and accelerate constructions. Meanwhile municipalities are actively planning housing projects and homeless remedy plan for 10-year or longer.</p>

<p><strong>2. Public Transits Revenue Not Fully Recovered<br></strong>While transit ridership recovered near 80% of pre-pandemic levels at most regional governments, revenue shortfalls persisted due to slow returns to offices in downtown. The increasing adoption in zero-emission vehicles also posed a challenge as it decreased fuel-tax revenue, although it is beneficial for the society in the long term, it is not easy to replace the fuel-tax part of the revenue source. Municipalities have received temporary funding from provincial governments to cover for transit revenue shortage, and implementing projects on expanding transit network. Overall ridership is expected to improve in 2025.</p>

<p><strong>3. Immigration Acted as A Double-Edged Swords<br></strong>Immigration has been a key part of economic growth and culture diversity, however the rapid unplanned increase in population led do a significant growth in demand and adding pressure for the municipalities to provie sufficient access to public health, housing, and social services.</p>

<p><strong>4. Inflation Driven Cost Eased but Still Persist</strong> <br>While the rate of consumer price inflation has slowed in 2024, labour and supply-cost inflation still reside, fueling challenges to both operating budgets and capital project costs, particularly for transit s and housing infrastructure. Municipalities have to be careful and innovative on fiscal management and strategically prioritize projects to maintain essential services. Some cities have pivot to increasing non-tax revenue such as advertisements and sponsorship.</p>

<p><strong>5. Borrowings Expected to Elevate in 2025<br></strong>municipal and agency issuers continue to offer investors attractive value relative to other government credits as local governments must balance their operating budgets. Total municipal and agency supply reached C$5.799 billion in 2024, making this year the 2nd most active on record with supply just below the record high of C$5.892 billion seen in 2021. Municipal and agency borrowings are effected by the scope, scale and timing of projects, as well as interest rates and investor sentiment. As capital growth spending accelerates and the increasing number of ESG projects, municipal and agency borrowers are expected to have a slightly larger funding program than 2024.</p>

<p><strong>6. Increased Involvement in ESG</strong> <br>Total Green, Social and Sustainable bond offerings from municipal and agency issuers reached C$2.4 billion in 2024, up from the C$1.8 billion seen in 2023 and accounted for more than 40% of the aggregate municipal and agency debt offerings in 2024. Of note, Ottawa printed their inaugural sustainability bond this year which followed the City’s development of their sustainable debenture framework. Many municipalities and agencies issue ESG bonds based off their sustainable bond framework, with majority of the UoP flowing into reducing carbon pollution, building affordable housing and raising community awareness.</p>

<div style="background: #fee100; margin: 25px 0px; height: 4px; clear: both; max-width: 75px;"> </div>

</div>

</div>

</div>

<div class="accordion-item">

<div id="heading4" class="panel-heading">

<div class="panel-title"><a class="accordion-toggle collapsed" style="font-family: 'RBCDisplay',Georgia,Times,serif; font-size: 24px; line-height: 28px;" href="#collapse4" aria-controls="collapse4" aria-expanded="false" data-parent="#accordion1" data-toggle="collapse">Government Finance Canadian Public Sector Debt Market Update <!--<div class="fa fa-chevron-down rotate pull-right"></div>--> </a></div>

</div>

<div id="collapse4" class="panel-collapse collapse" style="height: 0px;" aria-labelledby="heading4" aria-expanded="false">

<div class="panel-body">

<p>In addition, we encourage you to view the RBC Government Finance Public Sector Debt Market update that is published monthly. The December 2024 edition includes a year-end recap of issuance trends by the Canadian governments in 2024.</p>

<ul>

<li>Domestic public sector supply reached C$188.5 billion in 2024 following C$12.1 billion of total supply in December 2024, 26% higher than the C$150 billion seen in 2023</li>

<li>Issuance across all currencies and sectors reached C$288.0 billion in 2024, 36% higher than the C$211.8 billion seen in 2023</li>

<li>Total Canadian Public Sector Entities supply finished at C$40.4 billion, 8.6% higher than the C$37.2 billion through 2023 and representing a record year for the sector</li>

<li>The Maple SSA market had its lightest year since 2017 as C$3.7 billion in total supply was completed during the year, ~50% lower than the C$10.1 billion seen during 2023 which was a record setting year</li>

<li>Total municipal supply reached C$5.799 billion in 2024, making this year the 2nd most active on record with supply just below the record high of C$5.892 billion seen in 2021</li>

<li>ESG issuance remained comparable to volumes seen in 2023 with C$16.5 billion of supply priced during 2024 across Green, Social, Gender and Sustainability bonds</li>

</ul>

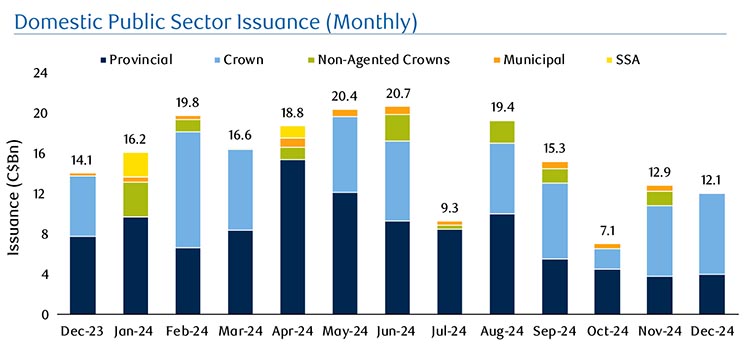

<p><img src="/assets/rbccm/images/insights/2025/roundtable-public-sector-graph-3.jpg" alt="Domestec Public Sector Issuance (Monthly) by Issuance (C$Bn) vs Month. Source: RBC Capital Markets as at December 29, 2023"></p>

<p style="font-size: 12px;">Source: RBC Capital Markets as at December 29, 2023</p>

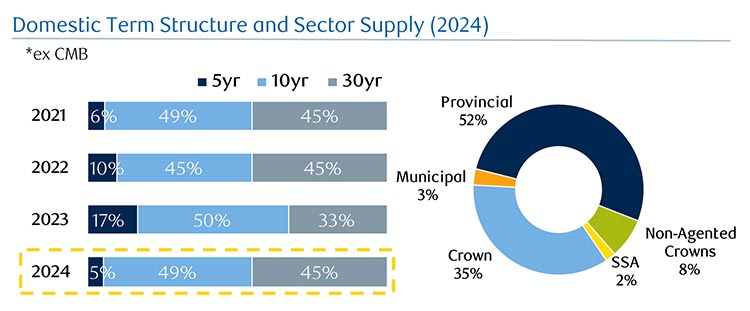

<p><img src="/assets/rbccm/images/insights/2025/roundtable-public-sector-graph-4.jpg" alt="Domestic Term Structure and Sector Supply (2024) image"></p>

<div style="background: #fee100; margin: 25px 0px; height: 4px; clear: both; max-width: 75px;"> </div>

</div>

</div>

</div>

<div class="accordion-item">

<div id="heading5" class="panel-heading">

<div class="panel-title"><a class="accordion-toggle collapsed" style="font-family: 'RBCDisplay',Georgia,Times,serif; font-size: 24px; line-height: 28px;" href="#collapse5" aria-controls="collapse5" aria-expanded="false" data-parent="#accordion1" data-toggle="collapse">Select RBC-led Transactions in 2024</a></div>

</div>

<div id="collapse5" class="panel-collapse collapse" style="height: 0px;" aria-labelledby="heading5" aria-expanded="false">

<div class="panel-body">

<p><strong>Transactions for Canadian Public Sector Issuers – Domestic</strong></p>

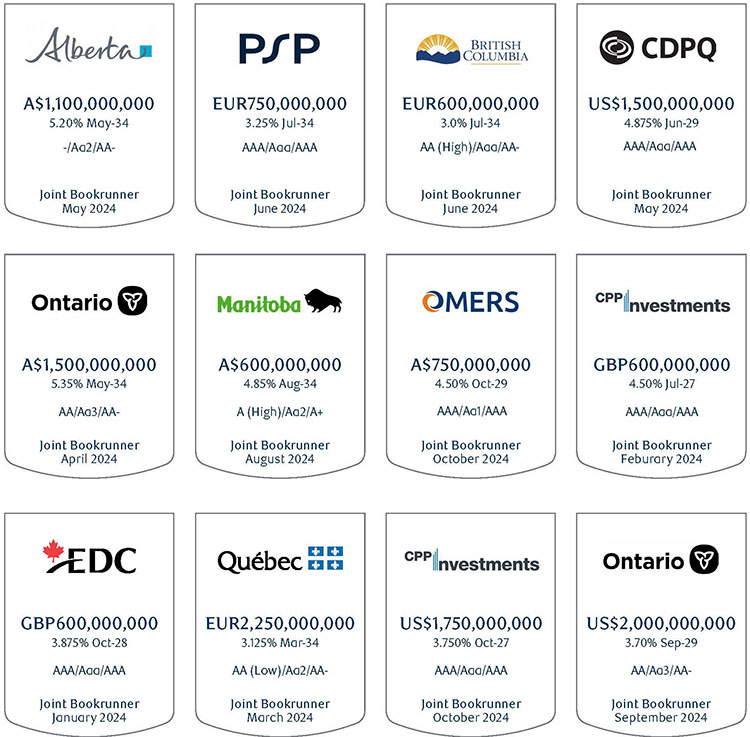

<p><img src="/assets/rbccm/images/insights/2025/canadian-borrowers-roundtable-1.jpg" alt="Select RBC-Led Transactions in 2024 tombstones: Transactions for Canadian Public Sector Issuers – Domestic image"></p>

<p><strong>Transactions for Canadian Public Sector Issuers - Offshore</strong></p>

<p><img src="/assets/rbccm/images/insights/2025/canadian-borrowers-roundtable-2.jpg" alt="Select RBC-Led Transactions in 2024 tombstones: Canadian Public Sector Issuers - Offshore Image"></p>

<p><strong>Transactions for Maple Offerings</strong></p>

<p><img src="/assets/rbccm/images/insights/2025/canadian-borrowers-roundtable-3.jpg" alt="Select RBC-Led Transactions in 2024 tombstones: Maple Offerings image"></p>

<hr></div>

</div>

</div>

<p style="margin-top: 25px;">Contact info: <br>RBCCM Government Finance<br><a title="Link to RBCCM Government Finance email" href="mailto:RBCCMGovernmentFinance@rbccm.com">RBCCMGovernmentFinance@rbccm.com</a><br>416-842-7756</p>

</div>

</div>

<hr><!--<div id="related-content-panel">

<div class="social-share hidden-xs">

<div style="margin-top: 25px;">

<div class="row">

<div class="col-lg-2">

<div class="display-iblock" style="padding-left: 0px; padding-bottom: 10px;"><span id="shareheader" class="uppercase" style="color: #424242; line-height: 45px;">Share</span></div>

</div>

<div class="col-lg-10"><a class="blue-circle-outline" style="margin-left: 0;" href="https://www.linkedin.com/shareArticle?mini=true&url=https%3A//www.rbccm.com/en/insights/story.page%3Fdcr%3Dtemplatedata/article/insights/data/2022/12/2022_canadian_public_sector_issuers_roundtable_series&title=2022%20Canadian%20Public%20Sector%20Issuers%20Roundtable%20Series&source=www.rbccm.com" target="_blank" rel="noopener" aria-label="Share to LinkedIn"><em class="fa fa-linkedin" style="color: #0051a5; margin-left: 13px;" aria-hidden="true"> </em></a><a class="blue-circle-outline" href="https://twitter.com/intent/tweet?url=https%3A//www.rbccm.com/en/insights/story.page%3Fdcr%3Dtemplatedata/article/insights/data/2022/12/2022_canadian_public_sector_issuers_roundtable_series&text=2022%20Canadian%20Public%20Sector%20Issuers%20Roundtable%20Series" target="_blank" rel="noopener" aria-label="Share to Twitter"><em class="fa fa-twitter" style="color: #0051a5; margin-left: 12px;" aria-hidden="true"> </em></a></div>

</div>

</div>

</div>

</div>

<div> </div>

</div>-->

<p> </p>text5 minenglobal1NRBCCM Government FinanceRBCCM Government Finance1/templatedata/article/story/data/2024/01/2023-canadian-public-sector-issuers-roundtable-seriesinsightsRBC Capital Markets Government Finance team was pleased to facilitate three separate virtual Canadian Public Sector Debt Issuance roundtable discussions in late November and early December 2024.RBCCM Government Finance, Canadian Public Sector Issuers Roundtable SeriesRBCCM Government Finance, Canadian Public Sector Issuers Roundtable Series

2024 Canadian Public Sector Issuers Roundtable Series

RBC Capital Markets Government Finance team was pleased to facilitate three separate virtual Canadian Public Sector Debt Issuance roundtable discussions in late November and early December 2024.

RBCCM Government Finance Published | 5 min

read

Similar to past years, participants included representatives from the Canadian Federal Government, federal agencies, provincial issuers, non-agent crown issuers, municipal issuers, offshore SSA maple issuers, and institutional investors.

The discussions focused on the current economic environment in Canada, trends in borrowing by public sector issuers in 2024 and expectations for 2025. This publication summarizes these conversations along with key insights and takeaways from issuers and investors in the Canadian public sector. We thank all the participants who dedicated the time to share their views and experiences.

1. Canada Outlook: economic growth, inflation, and Bank of Canada policy rate all to move lower in 2025: Growth is widely expected to underwhelm in 2025 as the effects of mortgage renewals, reduced immigration growth, and potential trade tariffs weigh on the general outlook

2. U.S. Tariffs pose a looming challenge for the Canadian economy: The effects of trade tariffs and retaliatory measures pose a significant risk to the Canadian economy, casting a shadow of uncertainty on growth forecasts

3. Declining immigration levels expected to provide relief on capacity pressures and contribute to lower growth: The plan to slow the growth in immigration levels is expected to be a headwind for economic growth, while allowing time to alleviate recent pressures on capacity. The effects of these policies will likely be felt over a number of years

4. 2024 was a record year for domestic and offshore public sector debt issuance; the pace of issuance is expected to moderate in 2025: Canadian Public Sector issuance across all currencies reached C$288.0 billion in 2024, 36% higher than 2023 and a new record for aggregate issuance

5. Year of firsts for Canadian public sector issuers: Canadian provinces issued a record C$51 billion equivalent in offshore markets; with many issuers expanding their borrowing programs into new currencies and tenors

6. Credit spreads near the tights, is the trend sustainable? With global credit spreads at the tighter end of the range, risks are tilted towards a retracement in 2025

1. Slightly Increased Funding Programs from Higher Disbursements SSA funding requirements saw a slight increase throughout 2024 compared to 2023 to reflect stronger disbursements, despite continued challenging conditions with geopolitical concerns and a various number of global elections towards the end of the year. Market participants noted challenging EUR markets and the expectation that the trend may persist in the new year. However, their focus remains in core currencies such as USD for Supranationals and EUR for European issuers, while continuing to seek for opportunities in other currencies where funding levels are attractive.

2. ESG Themed Bonds Driven by Investor Demand ESG is still a main part of SSA funding programs globally. ESG issuance continues to be favored among Maple SSA issuers and investors in the Canadian market; all 4 benchmark CAD SSA transactions in 2024 have been in ESG format, ranging across Gender, Green, and Sustainable bonds. Issuers noted that they are continuing to the explore theme bonds, and that sustainability debt will continue to be a focal point for SSA issuers if there is a healthy pipeline of projects and sufficient investor interest.

3. Awaiting the Right Timing To Return To the Maple Market Market participants value the CAD Maple market as a currency to diversify their funding program, however in 2024 due to swap level movements they have not been able to access the market for a prolonged period of time due to being offside versus their core funding currencies such as USD. All C$3.7 billion of the Maple supply in 2024 has been in the first 4 months of the year and quiet for the remainder of the year. SSA issuers remain positive about the CAD market, and noted if there are investor demand for longer dated issuances, they can go for duration if levels are attractive compared to their core funding levels.

4. Forward Looking/Challenges Looking ahead to 2025, SSA issuers anticipate having to navigate higher funding costs, compressed issuance windows and competing supply across core issuance currencies. Market participants however are cautious but optimistic, and will continue to be nimble about their funding program heading into the new year.

1. Affordable Housing Remains the Most Significant Issue The demand for affordable housing has been outpacing supply, largely driven by the immigration growth and place pressure on the City’s resources to deliver. This issue hit the hardest at the lowest income group, with a particularly large gap in housing supply for purpose built rental and community housing. Housing delivery continues to be a priority for all level of governments, there are various provincial and federal housing funds expected to be delivered in 2025 to meet housing starts targets and accelerate constructions. Meanwhile municipalities are actively planning housing projects and homeless remedy plan for 10-year or longer.

2. Public Transits Revenue Not Fully Recovered While transit ridership recovered near 80% of pre-pandemic levels at most regional governments, revenue shortfalls persisted due to slow returns to offices in downtown. The increasing adoption in zero-emission vehicles also posed a challenge as it decreased fuel-tax revenue, although it is beneficial for the society in the long term, it is not easy to replace the fuel-tax part of the revenue source. Municipalities have received temporary funding from provincial governments to cover for transit revenue shortage, and implementing projects on expanding transit network. Overall ridership is expected to improve in 2025.

3. Immigration Acted as A Double-Edged Swords Immigration has been a key part of economic growth and culture diversity, however the rapid unplanned increase in population led do a significant growth in demand and adding pressure for the municipalities to provie sufficient access to public health, housing, and social services.

4. Inflation Driven Cost Eased but Still Persist While the rate of consumer price inflation has slowed in 2024, labour and supply-cost inflation still reside, fueling challenges to both operating budgets and capital project costs, particularly for transit s and housing infrastructure. Municipalities have to be careful and innovative on fiscal management and strategically prioritize projects to maintain essential services. Some cities have pivot to increasing non-tax revenue such as advertisements and sponsorship.

5. Borrowings Expected to Elevate in 2025 municipal and agency issuers continue to offer investors attractive value relative to other government credits as local governments must balance their operating budgets. Total municipal and agency supply reached C$5.799 billion in 2024, making this year the 2nd most active on record with supply just below the record high of C$5.892 billion seen in 2021. Municipal and agency borrowings are effected by the scope, scale and timing of projects, as well as interest rates and investor sentiment. As capital growth spending accelerates and the increasing number of ESG projects, municipal and agency borrowers are expected to have a slightly larger funding program than 2024.

6. Increased Involvement in ESG Total Green, Social and Sustainable bond offerings from municipal and agency issuers reached C$2.4 billion in 2024, up from the C$1.8 billion seen in 2023 and accounted for more than 40% of the aggregate municipal and agency debt offerings in 2024. Of note, Ottawa printed their inaugural sustainability bond this year which followed the City’s development of their sustainable debenture framework. Many municipalities and agencies issue ESG bonds based off their sustainable bond framework, with majority of the UoP flowing into reducing carbon pollution, building affordable housing and raising community awareness.

In addition, we encourage you to view the RBC Government Finance Public Sector Debt Market update that is published monthly. The December 2024 edition includes a year-end recap of issuance trends by the Canadian governments in 2024.

Domestic public sector supply reached C$188.5 billion in 2024 following C$12.1 billion of total supply in December 2024, 26% higher than the C$150 billion seen in 2023

Issuance across all currencies and sectors reached C$288.0 billion in 2024, 36% higher than the C$211.8 billion seen in 2023

Total Canadian Public Sector Entities supply finished at C$40.4 billion, 8.6% higher than the C$37.2 billion through 2023 and representing a record year for the sector

The Maple SSA market had its lightest year since 2017 as C$3.7 billion in total supply was completed during the year, ~50% lower than the C$10.1 billion seen during 2023 which was a record setting year

Total municipal supply reached C$5.799 billion in 2024, making this year the 2nd most active on record with supply just below the record high of C$5.892 billion seen in 2021

ESG issuance remained comparable to volumes seen in 2023 with C$16.5 billion of supply priced during 2024 across Green, Social, Gender and Sustainability bonds

Source: RBC Capital Markets as at December 29, 2023