While two rounds of talks between the U.S. and Iran have yielded some constructive soundbites, the failure to resolve core areas of contention continues to tip the scales in favor of another military confrontation. Though Iranian representatives have signaled a willingness to return to the negotiating table with a more detailed proposal, there are no indications that the leadership is prepared to end domestic uranium enrichment or its ballistic missile program. The Trump administration for its part seems to be sticking with its maximalist zero-enrichment position and appears unwilling to accept an enhanced version of the 2015 Joint Comprehensive Plan of Action (JCPOA) to avert another kinetic confrontation. Certainly, one side could still blink, but the massive buildup of U.S. military assets in the region as well as the recent Iranian naval exercise in the Strait of Hormuz seem to suggest that the launch sequence for a second military conflict has commenced.

There is a significant risk that round two between Tehran and Washington will be wider and more disruptive than the 12-day war in June. Given the capture of Venezuelan leader Nicolas Maduro, Iranian Supreme Leader Khamenei will likely believe that regime change is the ultimate American/Israeli goal and will take aggressive measures to raise the cost of such an operation. Multiple observers warned that Iran would likely look to target energy facilities and other key economic assets to force Washington to stand down. It remains our understanding that senior officials from the region had warned the White House that a war with Iran in the current environment could send prices to triple-digit levels and hoped that the prospect of such a calamitous outcome would prompt President Trump to seek a Greenland-esque off-ramp.

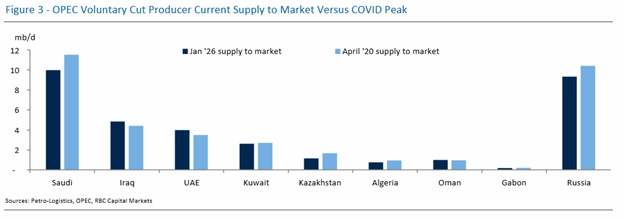

All of this is occurring against a backdrop of thin OPEC spare capacity shock absorbers. One leading regional official noted that the July 2008 run-up in oil prices to $148/bbl was driven by fears of no spare capacity. We continue to contend that the only meaningful spare capacity is sitting in Saudi Arabia, and if OPEC does decide to bring forward more production in the spring, the cupboard will be exceedingly bare if there are any major supply disruptions stemming from a U.S./Iran conflict, especially if Ukraine continues to target Russian (and by extension Kazakh) oil assets. One side may yet back down, but the standoff appears to be approaching an Ides-of-March moment.

Using naval bases in Bandar Abbas and Jask, Iran likely retains the ability to target tankers in the Strait of Hormuz and mine the critical waterway even if they cannot completely close it for an extended period. Similarly, Iran also probably has sufficient short- and medium-range missiles to hit a variety of economic targets across the region. Armed proxies such as Hezbollah and Hamas have indeed been seriously degraded by sustained Israeli action, but the Houthis and Iraqi militias are thought to maintain significant disruptive capabilities, and both were involved in the series of attacks in 2019 across the region that followed Washington's ending of exemptions for importers of Iranian oil.

“If OPEC does decide to bring forward more production in the spring, the cupboard will be exceedingly bare if there are any major supply disruptions stemming from a U.S./Iran conflict.”

Helima Croft, Head of Global Commodity Strategy and MENA Research, RBC Capital Markets

President Trump could certainly opt for a more circumscribed targeted strike and avoid a regime-change effort. If Washington does indeed choose a more limited engagement, Iran could also stick to a more limited set of retaliatory targets and avoid a wider regional escalation. The oil price impact of a more limited exchange would undoubtedly be lower, and any initial price run-up could be unwound once it becomes clear that oil once again will not be caught in the crosshairs. Nonetheless, we think there is a higher risk of a fog-of-war scenario setting in that could lead to an unintended escalation through miscalculation given what transpired in Venezuela as well as the apparent Iranian belief that U.S. and Israeli covert agents were involved in the recent wave of large-scale street protests.

Helima Croft authored "Iran Update: Launch Sequence," published on February 18, 2026. For more information on the full report, please contact your RBC representative.