Attacks on energy infrastructure continue to escalate, with the Israeli strike on South Pars and the Iranian retaliatory strikes against Qatar's Ras Laffan and the UAE's Habshan Gas Facility marking a potentially dangerous new chapter in the conflict. The energy crisis emanating from the three-week Iran war continues to deepen, with Israel's strike on the South Pars Gas Field sparking a dangerous wave of Iranian retaliatory action. Hours after Iran warned that energy assets are now "legitimate targets," Qatar's Ras Laffan complex was hit by missile fire, with QatarEnergy reporting "extensive damage" at the world's largest LNG facility. Following the attacks on Ras Laffan, Abu Dhabi's Habshan Gas Facility was targeted, with reports indicating multiple missile interceptions. Iran also threatened attacks on the UAE's Al Hasan Gas Field, as well as Saudi Arabia's Jubail Petrochemical Complex and Samref Refinery—the latter is notably located on the Red Sea port of Yanbu, which has become an increasingly important route for exports.

President Trump's policy solutions to date have shown little effectiveness in abating the energy shock emanating from this conflict, and risks continue pointing squarely to continued escalation and higher energy prices. Trump administration officials have spent considerable effort trying to convince market participants that the disruption will be short-lived as the war will soon wind down. Yet nothing points to a limited engagement at this juncture, as an increasing number of military experts insist that ground forces will be required to secure the Strait of Hormuz. Beyond the Strait, Iran has already extended the blast radius to key ports throughout the region using drones and remote-controlled small boats laden with explosives, further complicating the normalization of Middle Eastern energy exports. We think there may be too much emphasis on the "TACO" trade, as Iran could continue attacks, even if President Trump seeks to call time, to restore a measure of deterrence against future American military action. Iran does not need to keep up the furious pace of drone and missile fire to shutter the bulk of energy exports, and there may be a relatively deep bench of IRGC officials willing to step up and take the place of fallen comrades.

"Qatar's LNG exports, which make up 20% of the world's supply, were already offline under force majeure. Depending on the extent of damage, they could extend restart expectations significantly and add to risk premiums."

Helima Croft, Head of Global Commodity Strategy and MENA Research, RBC Capital Markets

As Qatar's LNG exports remain fully offline, the extensive damage at Ras Laffan extends restart timelines and threatens to further elevate global energy prices. As Qatar's LNG exports, which make up 20% of the world's supply, were already offline under force majeure, Wednesday's strikes at Ras Laffan do not take any incremental supply out of the market in the near term. However, depending on the extent of damage (described as "extensive" at the time of writing), they could extend restart expectations, which prior to major damage had already coalesced around a 4-6-week timeline for a full restart assuming crews would work in parallel and the Strait was de-risked. This would add to risk premiums and leave importers, especially those in Asia, looking for cargoes. Spot prices in Asia are expected to continue to outpace TTF, and the risk to the upside for global gas is increasing; as of yesterday, TTF was up 71% versus pre-crisis levels already.

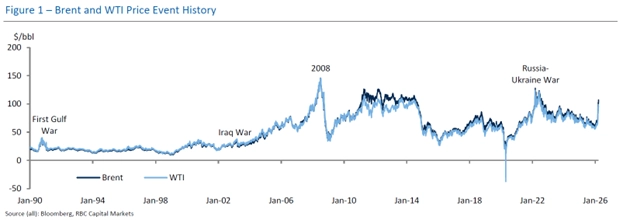

Assuming global gas remains a leading indicator and applying similar risk premiums and potential duration impact laid out for oil markets (using 2008 and 2022 highs as benchmarks), TTF could more than double versus pre-crisis levels (from 31.96 EUR/MWh) and reach the 65-130 EUR/MWh range if outages extend for several more weeks or months with minimal progress on maritime security that would enable the flow of cargoes assuming facilities were operational. This is still well short of the post Russia-Ukraine highs of over 300 EUR/MWh, reflecting a changed market, but factors in higher risk premiums and a longer duration outage. QatarEnergy reportedly was already pushing back the start of its expansion project to at least 2027, and any damage to existing infrastructure would likely add to delays, threatening to push on LNG glut expectations for the coming years.

We continue to watch for any signs that the Houthis may enter the conflict and imperil the Red Sea alternative export route. Currently, our data suggests Saudi Arabia is exporting around 3.8 mb/d from its west coast as it pushes incremental volumes on the East-West pipeline. It has proven to be a more secure alternative than the UAE's Fujairah port, which has been targeted on multiple occasions. For now, the Houthis have stayed on the sidelines, unlike in 2019 when they targeted the East-West pipeline and joined the Iranian strike on Abqaiq following the termination of exemptions for importers of Iranian oil by the US. Of all the Axis of Resistance proxies, the Houthis are viewed as the most independent from Tehran and are not seen as taking orders directly from the IRGC. Some have suggested that their capabilities have been degraded following over a decade of conflict, as well as the loss of key personnel including Prime Minister Ahmed al-Rahawi, who was killed by an Israeli airstrike in August 2025. Nonetheless, others maintain that Iran has a reserve option and the Houthis would enter the conflict if asked or if the IRGC was on the verge of complete "evisceration."

If the Yemeni group does become an active participant, we think it would materially alter risk perceptions about the Red Sea exports, and even just a few missiles or drones fired into the Bab el-Mandeb Strait would push oil prices several legs higher in the current environment. Since the Houthis became involved in the broader Middle East conflict in 2023, the group has conducted around 150 attacks on ships in the Red Sea, Gulf of Aden, and the Arabian Sea. The rate of attacks peaked in December 2023 and January 2024, resulting in the US/UK-led operation to secure the flow of maritime traffic and degrade the Houthis' disruptive capabilities, culminating in a May 2025 ceasefire with the US.

We believe the paper market has been underappreciating the Middle East supply disruption, with the physical crude market having seen a starker reaction over recent weeks as real trade dislocations have driven surging differentials. In fact, Platts saw May cash Dubai at a premium of $62.68/bbl versus same-month Dubai futures on March 17, while Oman cash Dubai versus same-month Dubai futures found the same levels, each at the highest levels observed in recent history. While we saw a slight lag in the broad physical market impacts in the first few days of the conflict, as some participants were in an initial wait-and-see mode and the Strait closure and supply disruption remained, buyers came out in force to begin sourcing alternate cargoes for refineries, such as those from the Americas and Atlantic Basin. In fact, WAF, one beneficiary, has seen differentials further improve of late as freight rates have softened following the initial rearranging of the global fleet.

"We still see a direct strike on [Kharg Island] as unlikely given soaring oil prices. That said, we think an operation to seize the oil operations could still gain traction in Washington."

Helima Croft, Head of Global Commodity Strategy and MENA Research, RBC Capital Markets

On Wednesday, the U.S. issued a 60-day waiver on the Jones Act in an effort to stave off energy price impacts as discussions over potential export bans continue. We view the waiver as having minimal impact on domestic gasoline prices (likely a few cents on the gallon nationally), as the potential transit cost savings pale in comparison to crude input costs. The waiver will allow foreign vessels and crews to transport U.S. oil, natural gas, fertilizer, and refined products, especially for shipments on the east coast. However, though this 60-day duration surpasses the initial 30-day expectation, existing supply chain commitments in place for the near term will constrain how much impact the waiver will have on trades, further supporting our view that pump price relief will be limited.

Easing of Jones Act restrictions would likely be a prerequisite for any export bans enacted by the US, which, if encompassing both crude and product markets, could provide further assistance to domestic fuel prices in the near term. We believe a crude export ban alone could be counterproductive, as refiners would likely still be incentivized to sell refined product to the lucrative global market, which would see price appreciation further exacerbated by a loss of U.S. crude exports and ultimately leave U.S. prices exposed. On the other hand, a product-only ban could reduce domestic fuel prices, but, in leaving crude input costs exposed to the global market, could also threaten subsequent run cuts. In theory, a crude and product export ban may be more effective at blunting pressure at the pump, and the Jones Act waivers would help ease some of the logistical constraints for distributing domestic supplies, though this, in the best-case scenario, would anger allies that are key U.S. energy importers and leave global prices as collateral damage.

The killing of Secretary of the Supreme National Security Council Ali Larijani marks the most significant assassination of IRGC leadership since the initial strike that killed Supreme Leader Ali Khamenei. Alongside Larijani—who was seen as one of the most influential figures in Tehran's leadership—Israeli strikes this week have also killed Basij militia head General Gholamreza Soleimani and Minister of Intelligence Esmail Khatib. While the loss of these prominent figures undoubtedly has ramifications for Tehran, we see little sign of the IRGC stepping back from its hardline stance, with younger and potentially more radical voices assuming elevated positions in the leadership. Moreover, it is worth noting that while Larijani was considered a hardline element in the IRGC, he was also viewed as somewhat of a pragmatist and a potential interlocuter, given his support for the 2015 JCPOA. With the continuing escalations and high-profile assassinations, we wonder who the U.S. would negotiate with if Washington wants to pursue a diplomatic offramp, with no opposition figures emerging thus far in the conflict.

Helima Croft authored “Iran Flashpoints: Throwing Gas on the Fire,” published on March 19, 2026. For more information on the full report, please contact your RBC representative.