As widely anticipated, the U.S. and Israel launched another round of strikes on Iran, with the aftershocks felt more widely across the region than in June and the Iranian leadership suffering heavier losses, including Supreme Leader Ali Khamenei. The ultimate oil price impact of military action will likely hinge on whether the IRGC folds in the face of the aerial onslaught or if it pursues further escalatory actions to appreciably raise the costs of Washington's second regime change operation in a little less than two months.

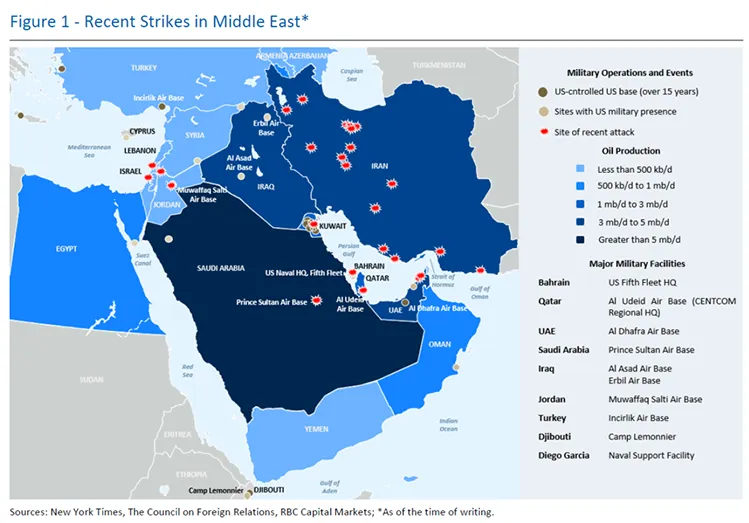

The situation remains extremely fluid, and it is unclear who exactly is calling the shots in Tehran. Iran has already targeted U.S. bases across the region, as well as high-profile airports, ports, and landmark buildings throughout the Gulf. Though there is no confirmation of any major oil facilities being targeted at the time of writing, tanker traffic through the all-important Strait of Hormuz has already been significantly curtailed.

“Though the IRGC may not be able to physically close the Strait of Hormuz, they could potentially still deploy small boats, mines, drones, and missiles to compel insurers and shipping companies to avoid the waterway.”

Helima Croft, Head of Global Commodity Strategy and MENA Research, RBC Capital Markets

The Houthis in Yemen and the Iraqi Axis of Resistance still likely have enough residual firepower to target critical economic assets across the region. Dubai seems to have been on the receiving end of Iranian retaliation, with the iconic Burj Al Arab, Palm Jumeirah, Dubai International Airport, and Jebel port already impacted by incoming fire.

It is our understanding that regional leaders warned Washington about the contagion risks of another confrontation with Iran and indicated that $100+/bbl oil was a clear and present danger. With Washington having declared a maximalist regime change goal, the IRGC may believe it can prevail in a war of attrition if President Trump is not prepared to commit ground forces. Some military planners have warned that air power alone has rarely yielded a complete regime change outcome.

This is all taking place against a backdrop of minimal OPEC shock absorbers. Every OPEC+ producer appears maxed out with the sole exception of Saudi Arabia. Hence, the barrel impact of any headline OPEC+ increase will be limited by the lack of actual production capabilities. Moreover, any surge above levels produced in the April 2020 price war peak would likely necessitate tapping storage. Even then, the utilization of any spare barrels will be severely limited if critical waterways are rendered inoperable. Spare barrels serve little purpose if there are no serviceable sea lanes.

Officials in Washington may come to regret not refilling the Strategic Petroleum Reserve if this proves to be a longer duration conflict. China, by contrast, has been aggressively filling its strategic reserves, potentially due to supply disruption concerns. Again, if this proves to be a short exchange of fire, any oil price increase will likely prove fleeting, and market participants will refocus on the fundamentals. Conversely, prices will likely move materially higher if this conflict extends beyond a few days and if the IRGC pursues a survival strategy predicated on exploiting President Trump's economic pain points.

Helima Croft authored "Iran War Update: Regional Ripple Effect," published on February 28, 2026. For more information on the full report, please contact your RBC representative.