Energy is now clearly in the crosshairs of the Iran war, with the Strait of Hormuz effectively closed and key facilities directly targeted including Qatar's LNG operations. The ultimate price trajectory will hinge on the duration and degree of disruption posed by the conflict, but Iran's drone capabilities and missile stockpiles suggest that market participants should potentially prepare for cascading outages.

Tanker traffic through the Strait of Hormuz has collapsed dramatically. While Iran has not yet officially stated its aim to close the waterway, flows have been reduced to a mere seven tankers and one gas carrier on March 1, compared to 56 tankers on February 27. The Iranian Revolutionary Guard Corps may not be able to physically close the Strait of Hormuz, but they are able to adequately deploy small boats, mines, drones, and missiles to ensure insurers and shipping companies continue to avoid the waterway until the cessation of hostilities. Most major insurers will reportedly officially terminate war risk coverage for the waterway on March 5 at midnight London time.

Though there are some oil pipeline outlets that could theoretically moderate the full impact of Strait closure, such as Saudi's East-West pipeline (7 mb/d capacity) and UAE's ADCOP pipeline (1.5 mb/d capacity), significant risks and limiting factors exist. Both assets remain at serious risk of being caught in the crosshairs of the conflict themselves, in which case damage could eliminate this option entirely. There is precedent for such attacks: in 2019, Houthi drones damaged two pumping stations on the East-West pipeline and temporarily downed crude flows. Furthermore, rerouted exports via the Red Sea would similarly be vulnerable. Some regional producers lack any potential alternative routes, such as Kuwait and southern Iraq.

“The lack of secure alternative export routes could render the majority of the Middle East's energy exports stranded assets if there is no viable plan to incentivize shipping companies and insurers to move tankers through the Strait.”

Helima Croft, Head of Global Commodity Strategy and MENA Research, RBC Capital Markets

Saudi Arabia's Ras Tanura refinery, one of the Middle East's largest, has halted processing following an Iranian drone strike at a storage facility. Two drones were intercepted overhead, with debris falling on the storage infrastructure. The refinery is a key supplier of transport fuels like diesel for European buyers and produces smaller quantities of gasoline.

Meanwhile, Qatar LNG ceased production at Ras Laffan, the world's largest LNG facility, following attacks on both Ras Laffan and Mesaieed. Qatar supplies about a fifth of the world's LNG, making this disruption among the most consequential. While the extent and duration of the damage remains unclear, there is no viable derisking infrastructure for these volumes. Even if facilities were operating, viable sea lanes are necessary regardless. The majority of Qatar's exports head to Asia, with its top five importers being China, India, Taiwan, South Korea, and Pakistan; yet global gas prices in import markets like TTF are bearing the burden too.

Because of its lack of adequate outlet infrastructure, Iraq appears to be one of the most vulnerable regional oil producers to the prospect of production shut-ins alongside Strait disruption. Iraq's Foreign Minister spoke with his Saudi counterpart about the material risks of the Strait remaining closed. As the country cannot route displaced volumes through the ITP pipeline and it simultaneously faces material oil storage limitations, Iraq would likely have to start curtailing production if it cannot utilize the waterway for its 3.5 mb/d of southern exports for a prolonged period. Like many other producers in the region, Iraq sees the majority of its crude head to Asia.

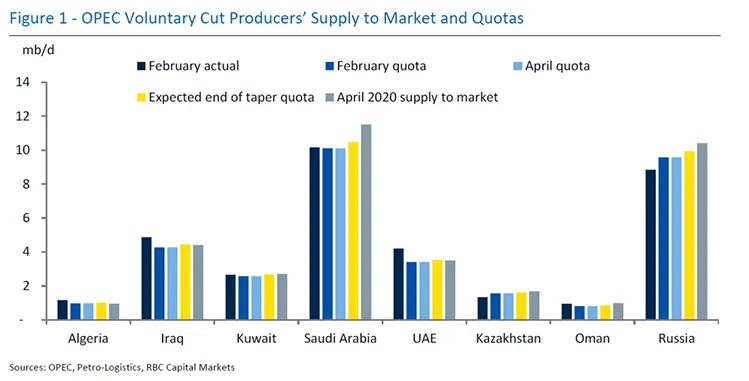

Against the backdrop of an escalating crisis in the Middle East, OPEC's V8 producers announced a headline increase of 206 kb/d for April. The actual volumes coming onto the market will fall well short of this announced production target, likely rising by less than 70 kb/d, with nearly all the voluntary producers having essentially reached their near-term production ceilings. The announced 62 kb/d increase from Russia appears especially dubious since the country's production has been trending downward due to sanctions and ongoing Ukrainian attacks on its energy infrastructure.

The absence of serviceable sea lanes essentially renders any production increase an entirely moot point, as the lion's share of OPEC barrels in the region could become stranded assets in an extended war scenario. Iran's extensive unmanned aerial vehicle (UAV) capabilities may provide it bandwidth to continue asymmetric attacks and move the conflict up the escalation ladder. Some leading military experts are already drawing comparisons to the Russia-Ukraine conflict, with both sides deploying UAVs to conduct disruptive infrastructure attacks and to make up for missile stockpile shortfalls. Tehran has already launched its cheap and domestically produced Shahed family of one-way drones against a variety of targets across the Middle East, including U.S. bases and civilian sites in Bahrain, Iraq, Kuwait, Qatar, and the UAE.

In a prolonged conflict scenario, oil prices could reach into the $100s per barrel, and global gas prices may at least hit their highest since Q1 2023 (post the 2022 highs after Russia's invasion of Ukraine). The rise in European gas prices, particularly TTF, is a more accurate reflection of the true risk profile from this conflict than the more modest run-up in oil prices currently. At this stage, we view oil prices as a lagging rather than a leading indicator of the potential supply shock risk posed by an extended conflict.

Helima Croft authored "Iran Flashpoints: Cross-Commodity Monitor," published on March 2, 2026, and "OPEC/Iran Update: Stranded Assets?" published on March 1, 2026. For more information on these reports, please contact your RBC representative.