Washington faces three possible policy paths forward, none offering easy solutions. President Trump could withdraw U.S. forces, but Iran would retain control of the Strait of Hormuz and market concerns about maritime freedom would persist. Alternatively, escalation through a U.S. troop surge could attempt to physically reopen the Strait or seize Kharg Island to change Tehran's calculus, though Iran's asymmetric "survive and exhaust" doctrine offers no guarantee of swift victory, and American public opinion could constrain action ahead of midterms. A third option would pursue negotiated settlement prioritizing freedom of navigation in Middle Eastern waters. At present, Washington and Tehran remain far apart with competing peace proposals, and while a negotiated path may be the clearest route to reopening the Strait, the ongoing U.S. troop buildup suggests the administration has not yet adopted this as its preferred option.

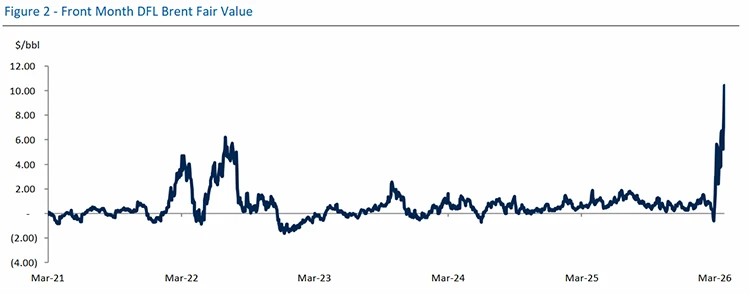

The physical market tells a stark story of ongoing tightness. Despite Brent pushing as high as $115/bbl, energy executives across the region have indicated that the delta between physical and paper markets is unsustainable. Buyers have come out in force since early March to source alternate cargoes from Latin America and West Africa, with differentials climbing steadily. Bonny Light now trades at a premium of $7.15/bbl compared to a pre-war differential of $0.25/bbl. European refineries emerging from maintenance have bolstered physical appetite, supporting Dated Brent strength and pushing front-month DFL spreads and Brent CFDs to fresh records. Easing of sanctions on Russia and Iran has done little to relieve the tightness. The magnitude of disruption leaves this short-term relief as just a drop in the bucket, and the market continues to appear exceptionally short.

The Houthis represent a major wildcard that could fundamentally alter market dynamics. The group formally entered the conflict on March 27, posing yet another escalation risk by potentially imperiling the region's principal alternative energy export route. From the start of the war, the Houthis have been identified as one of the biggest wildcards, with their involvement having the potential to change shipper calculus about the security of the beleaguered Bab al Mandeb and Saudi Arabia's Yanbu port, which is currently exporting over 5 mb/d of crude. Historical precedent underscores this threat: in 2019, the Houthis attacked pumping stations along the East-West Pipeline and joined the Iranian assault on Abqaiq. While the group has only directly targeted Israel thus far and made verbal warnings about impending action targeting the Bab al Mandeb, some analysts suggest the Houthis might be reticent about openly antagonizing Saudi Arabia given their domestic governing priorities in Yemen. Nonetheless, even a relatively small show of force from the Houthis would be enough to cause real market concerns about the Red Sea export route and push crude another leg higher.

The Houthis' track record of maritime disruption demonstrates their operational capability. Since becoming involved in the broader Middle East conflict in 2023, the group has conducted around 150 attacks on ships in the Red Sea, Gulf of Aden, and the Arabian Sea. Attack rates peaked in December 2023 and January 2024, prompting the US/UK-led operation to secure maritime traffic flow and degrade the Houthis' disruptive capabilities, culminating in a May 2025 ceasefire with the U.S. Saudi Arabia's investment in the strategic East-West pipeline has proven to be one of the few bright spots in the ongoing crisis. As the pipeline reaches its maximum capacity of 7 mb/d, it remains the most viable route for significant Middle Eastern exports, providing much-needed price relief as the Strait remains closed and production shut-ins in the region top 11.4 mb/d. Unfortunately, the ongoing security of that critical exit route does seemingly hinge on Houthi restraint or lack thereof.

Production constraints will persist long after the conflict ends. Kuwait Petroleum Corporation CEO Shaikh Nawaf Al-Sabah highlighted that it would take months for Kuwait to return to full production capacity once operations restart. Other regional producers, particularly Iraq with its aging infrastructure, will similarly require prolonged ramp-up periods. Energy infrastructure remains in the crosshairs of the conflict, extending restart timelines through damage. The IEA has reported that at least 40 energy facilities in the region have been severely damaged thus far, while refinery capacity cuts of over 2.5 mb/d further hinder production recovery. A gradual climb toward 12 mb/d in production cuts is anticipated as regional producers walk down output toward domestic refinery consumption levels, with only slight incremental production to feed viable alternate outlets like the East-West and ADNOC pipelines, assuming those assets remain uninterrupted.

“The return of supply even in the best-case scenario will be a longer process than many market participants expect.”

Helima Croft, Head of Global Commodity Strategy and MENA Research, RBC Capital Markets

Asian economies are bearing the brunt of supply disruption. Import-dependent nations across Southeast Asia are disproportionately feeling the energy shock, forcing emergency measures as domestic reserves of oil and LNG typically last only 20 to 50 days. Pakistan and Bangladesh have closed schools and universities, Myanmar has implemented fuel rationing, China cut product exports, and India announced levies on diesel and jet fuel exports while cutting domestic taxes on fuels. Most Southeast Asian nations are encouraging working from home or introducing 4-day work weeks to reduce consumption. The Philippines became the first Asian country to declare a national energy emergency, remaining in effect for a year and providing subsidies to transport-dependent workers as fuel prices soar. These near-term measures should help mitigate supply impact, but the situation could become critical once reserves are depleted.

Ukrainian strikes on Russian energy infrastructure continue to escalate. Kyiv aims to pressure Moscow's profits from the global supply shock through intensified targeting of export capabilities. While some refineries including Saratov, Kirishi, and Yanos have been struck, exports have become a more central focus. Over the past week, Ukraine has hit the ports of Primorsk and Ust-Luga multiple times, with operations currently impacted at both facilities. Primorsk has shown some signs of activity, but Ust-Luga appears fully halted with sustained new damage. Combined with the ongoing interruption of Druzhba flows following earlier drone strikes, Reuters reports that Primorsk and Ust-Luga outages have brought roughly 40% of Russia's exports offline. Analysts expect Ukraine will continue to disrupt Russian supplies to the market, impeding any moderating impact the country could provide.

Helima Croft authored "Iran Flashpoints: No Easy Way Out," published on March 29, 2026. For more information on the full report, please contact your RBC representative.