As the war enters its third month with no end in sight, the contagion effect is spreading westward and setting the stage for a cruel summer. From the conflict's outset, market participants seized on any headline suggesting an imminent conclusion and reopening of the Strait of Hormuz. Yet despite a tenuous ceasefire, the diplomatic divide between Tehran and Washington remains stark. Iran maintains it will not relinquish its right to uranium enrichment, though it may accept lower levels consistent with civilian programs. The country has signaled willingness to dilute highly enriched material stockpiles but refuses to ship them outside its borders. With face-to-face negotiations failing to materialize in Islamabad despite optimistic market headlines, neither side appears sufficiently pressured to make serious concessions.

For eight weeks, the White House successfully deployed an "over soon" message to cap front-month prices. However, leading physical traders warn this message management short-circuits the necessary price signaling needed to curb consumer demand relative to the colossal supply reduction. The constrained price response to history's largest supply shock may be fostering overconfidence in Washington that costs are manageable, especially given abundant U.S. production. Yet even a breakthrough in negotiations would mean extremely protracted Middle Eastern production recovery given damage to facilities, fields, and logistic bottlenecks. The best-case scenario sees significant quantities returning within three to six months in moderate damage situations, extending much longer if Iranian missile and drone strikes prove more devastating than satellite imagery initially indicated. Up to 1 billion barrels of crude and products have been displaced from markets according to industry leaders. The ever-present optimism bias may be blinding market participants and policymakers to the iceberg looming under the surface as we close in on peak summer demand season.

"Even a breakthrough in negotiations would mean extremely protracted Middle Eastern production recovery given damage to facilities, fields, and logistic bottlenecks."

Helima Croft, Head of Global Commodity Strategy and MENA Research, RBC Capital Markets

The physical market remains exceptionally tight with expectations for further upside into summer demand season as incremental demand converges with durable supply constraints. Though differentials have softened modestly from conflict peaks as some Asia-Pacific refineries reduced purchasing due to margin pressures and Chinese refinery throughput declined, the convergence of unchanged supply, drawing inventories, and incremental demand will inevitably push product prices higher in summer. This should bolster refinery margins and surge crude prices, easing only when serious demand destruction occurs at the consumer level, which carries significant economic risks. Near-term refinery throughput reductions, government-induced product export bans, and potential new Middle East or Russian facility damage threaten to further constrict product supplies and exacerbate the summertime shock.

China maintains strategic distance from diplomatic efforts, retaining comparatively robust shock absorbers, having aggressively stockpiled energy and commodities for strategic purposes. With over half its imports from the Middle East, China faces supply pressures from the two-month conflict and global economic impact given its export emphasis. However, Beijing shows little eagerness to become a significant diplomatic player in the Iran war at this stage. China maintains strong diplomatic relations across the region and prioritizes its East Asian position and advancing U.S. bilateral relations, even as the conflict weighs on Washington ties. Compared to much of East Asia, China's more secure energy picture has created diplomatic advantages, with countries like Vietnam and the Philippines still receiving Chinese exports.

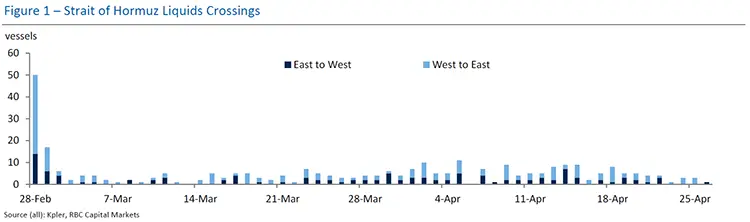

Figure 1 displays a bar chart titled "Strait of Hormuz Liquids Crossings" that visualizes vessel traffic carrying liquid cargo through this strategic waterway. The vertical axis measures the number of vessels (ranging from 0 to 60), while the horizontal axis shows dates spanning from February 28, 2026, to April 25, 2026.

The chart uses two distinct colors to represent directional flow: dark blue bars indicate vessels traveling East to West, and light blue bars represent vessels moving West to East.

Key data points include:

February 28: A notable spike showing approximately 50 West to East vessels and roughly 5 East to West vessels.

March 1-6: Sharp decline to approximately 17 West to East vessels on March 1, then dropping to 5-7 vessels, with East to West traffic at 3-5 vessels.

March 7 through April 25: Significantly reduced traffic with most days showing 0-10 vessels in either direction, with occasional peaks reaching approximately 10-11 vessels.

The pattern suggests substantially lower traffic levels after the initial late-February period, with both directional flows remaining relatively balanced at low volumes.

The source attribution states "Source (all): Kpler, RBC Capital Markets," indicating the data originates from Kpler's vessel tracking system as compiled by RBC Capital Markets.

Demand ripple effects are migrating westward toward Europe. While Asia has been the epicenter of the energy crisis, pain is radiating westward, with Europe increasingly feeling the two-month war's impact. The crisis has already cost the EU an additional €24 billion (€587 million daily) on fossil fuel imports since February, with aviation emerging as a particularly vulnerable sector. Lufthansa announced 20,000 flight cancellations through October, KLM canceled 80 return flights from Amsterdam citing route unviability, and Scandinavian Airlines scrapped approximately 1,000 flights in April alone. Some European airlines have warned they only have guaranteed fuel supplies through mid to late May, suggesting more carriers may curtail routes.

The crisis is accelerating consumer behavior shifts, with second-hand EV sales in the Netherlands up 99% year-over-year in March, while European battery-electric vehicle registrations surged 29.4% in Q1 2026, with a 51.4% gain in March alone. Meanwhile, Asia continues implementing severe demand destruction measures, with South Korea freezing its fuel price ceiling system through late April, India imposing a 20% cut to industrial LNG supplies, Bangladesh beginning fuel rationing, and multiple countries including the Philippines, Vietnam, and Sri Lanka reinstating work-from-home mandates and introducing driving restrictions. Consumption and policy responses are expected to continue as the crisis spreads heading toward summer demand season, with longer-term implications of these behavior changes warranting close monitoring.

Helima Croft authored "Iran Flashpoints: Summer Shock," published on April 26, 2026. For more information on the full report, please contact your RBC representative.