The consumer staples sector stands at a crossroads. After decades of predictable growth built on global supply chains and mass-market appeal, companies now confront challenges that demand strategic responses traditional playbooks cannot address. Over the past two decades, consumer staples have lagged the S&P 500 by approximately 187 percentage points on a cumulative basis. The companies that create value in the near future will be those that have the courage to make decisive decisions that others are not willing to make.

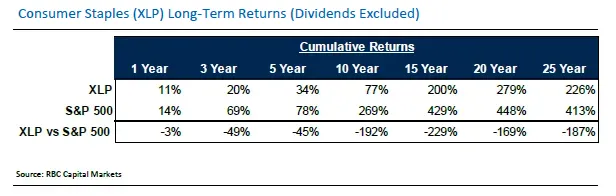

The table, titled "Consumer Staples (XLP) Long-Term Returns (Dividends Excluded)," compares the cumulative returns of XLP against the S&P 500 across seven timeframes. The data shows that the S&P 500 consistently outperformed XLP across all measured periods.

The cumulative returns are broken down as follows:

One year: XLP returned 11% compared to the S&P 500’s 14%, resulting in a difference of -3%.

Three year: XLP returned 20% compared to the S&P 500’s 69%, resulting in a difference of -49%.

Five year: XLP returned 34% compared to the S&P 500’s 78%, resulting in a difference of -45%.

10 year: XLP returned 77% compared to the S&P 500’s 269%, resulting in a difference of -192%.

15 year: XLP returned 200% compared to the S&P 500’s 429%, resulting in a difference of -229%.

20 year: XLP returned 279% compared to the S&P 500’s 448%, resulting in a difference of -169%.

25 year: XLP returned 226% compared to the S&P 500’s 413%, resulting in a difference of -187%.

The source of the data is cited as RBC Capital Markets.

The end of "the average consumer"

Stratified Society reflects a fundamental split: high-income consumers seek experience, convenience, and wellness through closed ecosystems and memberships; lower-income households prioritize value maximization and functional sufficiency. Unlike traditional cyclical inequality, today's stratification is reinforced by technology, housing scarcity, education asymmetry, healthcare cost inflation, and algorithmic segmentation. This creates a bifurcated demand environment in which "the average consumer" no longer exists.

The old days of trading down in a downturn in the economy are over. The K-shaped economy is structural and global. For consumer companies, this implies portfolio architectures that resemble barbells rather than ladders. Growth will accrue at the extremes, not the middle. Companies that fail to embrace this reality risk chronic volume leakage and margin compression.

"Portfolio architectures must resemble barbells rather than ladders. Growth will accrue at the extremes, not the middle. Companies that fail to embrace this reality risk chronic volume leakage and margin compression."

—Nik Modi, Co-Head of Global Consumer and Retail Research, RBC Capital Markets

"Synthetic everything" as operating backbone

Synthetic alternatives will reach a tipping point, permeating nearly every aspect of life, from food and materials to biology, data, emotion and even identities. Driven by breakthroughs in synthetic biology, autonomous code, AI-generated content, and programmable matter, the global economy will increasingly rely on systems that are faster, cheaper and more scalable, but also more artificial. The cost of AI inference dropped over 280-fold between November 2022 and October 2024.

Synthetic research and development will significantly compress innovation cycles. Traditional formulation depends on iterative testing constrained by seasonality, crop quality, and supply availability. Synthetic platforms allow companies to simulate, test, and deploy formulations continuously, reducing time-to-market and increasing SKU optionality. Leading consumer companies will bifurcate offerings – core SKUs leveraging synthetic inputs for efficiency, while premium lines emphasize craftmanship and heritage. As AI systems increasingly act on behalf of consumers, agentic commerce represents a structural break in how consumer demand is generated and allocated.

The rise of the 8th continent

Digital platforms command user bases larger than most countries, creating self-contained economic systems where commerce, content, and community converge. The global creator economy's revenue by end use was approximately $205 billion in 2024 and is projected to surpass $1.3 trillion by 2033. In this environment, cultural relevance increasingly outweighs traditional scale advantages. Value accrues to brands that are culturally relevant and algorithmically favored.

In the future, brands will increasingly design products for platforms, not shelves. Packaging, price points, and messaging are optimized for scroll velocity and shareability. Consumer companies need to allocate marketing budgets toward platform-native content rather than linear media, acknowledging that platforms now function as demand exchanges. Products, ideas, and identities spread through replication, remixing, and social reinforcement rather than paid reach.

Shifting superpowers: the rise of fragmented sovereignty

The world does not have one center, it has many. Superpowers are no longer defined by flags, but by flows – of data, talent, capital, culture, and trust. In this new matrix, the ability to adapt, convene, and connect matters more than dominating. A new era of state capitalism and techno-nationalism emerges over the next 3-5 years. After decades of global integration, governments around the world reassert control over core industries, from semiconductors to energy. The most important superpower shift is demographic. Aging, capital-rich economies coexist with young, labor-rich but capital-constrained regions.

Global consumer companies will have to increasingly operate as federated entities: local in appearance, global in capability. IP, capital, and systems remain centralized, while branding, governance, and community engagement decentralize. This creates a premium for organizational modularity. Companies that can appear culturally native everywhere retain access. Those that cannot face shrinking addressable markets despite global scale. Companies that train workers, deploy AI efficiently, and tap into global digital labor pools will outperform.

Crisis as default operating environment

The world no longer operates under illusions of stability. Climate volatility, cyber threats, pandemics, and supply chain upheavals are becoming permanent features. The system no longer returns to equilibrium; it oscillates between shocks. Success in this era is not about avoiding failure, but about building the capacity to absorb shocks, innovate on the fly, and thrive in an environment defined by disruption.

For consumer companies, this fundamentally alters the objective function. Efficiency, just-in-time logistics, and cost minimization are no longer optimal. The dominant competitive advantage becomes continuity. Consumer staples companies are in the process of executing a pivot from cost optimization to continuity architecture — regionalizing product facilities and deliberately multi-sourcing critical ingredients as climate volatility renders just-in-time models very risky. In Crisis Capitalism, trust becomes the most valuable currency for consumer staples companies, more durable than brand recognition and more monetizable than distribution scale.

Nik Modi authored "The Great Recalibration - Consumer Staples Edition," published on February 9, 2026. For more information on the full report, please contact your RBC representative.