As summer demand season approaches, widespread optimism surrounds a potential June reopening of the Strait of Hormuz, but this consensus rests on fragile assumptions about the simplicity of resolution. The tenuous expectation assumes there exists a readily available policy lever that can easily restart maritime traffic. Reality suggests otherwise. Three potential paths forward all fall short of delivering the full Hormuz recovery markets are pricing in.

The most direct option, a comprehensive U.S. military operation deploying over 100,000 ground troops to physically reopen the Strait and remove Iran's regime, could theoretically provide the clearest path to restoration. However, the White House shows little enthusiasm for such an extensive and extended Middle East military commitment, which would directly contradict many America First campaign pledges. While the ceasefire remains exceedingly fragile and fighting could resume, any further U.S. action will likely fall short of the full-scale ground invasion necessary to force a reopening.

Much of the June reopening optimism assumes either a negotiated settlement or a unilateral U.S. exit. We are skeptical of an imminent diplomatic resolution given unresolved sticking points over Iranian enrichment capabilities and uranium stockpiles. Even in the event of a resolution to these nuclear issues, the IRGC will seek to maintain control over the Strait of Hormuz, which has now become arguably even more strategically important to reestablishing deterrence than the nuclear program itself. The regime will be extremely reluctant to relinquish this newfound leverage, which appears critical to its survival.

A third scenario involves Washington simply walking away and declaring the war over, but this would likely leave the Strait under Iranian control. Any outcome ending with Iran determining which ships navigate the waterway will result in flows appreciably below pre-war levels. As long as the IRGC remains a sanctioned entity, Western companies will be wary of paying a toll to access approved shipping lanes, and the risk of renewed maritime attacks will potentially disincentivize an immediate return. Leading shipping industry experts have already indicated that an Iranian-controlled reopening would likely result in restricted volumes and that a clear Iranian military defeat and unrestricted transit access are likely prerequisites for full Hormuz recovery.

If Iran retains operational rights, flows could potentially normalize around reduced rates comparable to those in the Red Sea. Despite the U.S. signing an agreement with the Houthis to end hostilities a year ago, Red Sea traffic is currently running around 56% lower than pre-conflict levels, as many major shipping firms still avoid the route out of concern over security of the Bab el Mandeb chokepoint. Even reaching that level would likely require an extended period of time, given the multi-week vessel logistics operations that would follow any opening irrespective of shipper risk assessments.

"Any scenario that ends with Iran determining which ships navigate the Strait will result in flows appreciably below pre-war levels."

Helima Croft, Head of Global Commodity Strategy and MENA Research, RBC Capital Markets

Throughout the conflict, the White House has cycled through a variety of strategies and timelines. More recently, the administration has signaled a willingness to let the double blockade run its course and cause enough economic pain to compel Iran to loosen its grip on the Strait. There were initial suggestions that Iran would reach storage tank capacity within 13 days and seek immediate settlement. However, Iran appears to have more runway (potentially weeks to months yet) before storage becomes a clear constraint. Moreover, the leadership may be more resilient, having previously weathered extremely challenging economic circumstances. The IRGC maintained its monopoly over the use of force after facing widespread protests in December and January over deteriorating economic conditions, and there are no clear indications of serious fissures in the security services. We will continue watching for signs that the regime's hold on power is becoming more fragile due to heightened financial problems, but we do not see the double blockade changing Tehran's calculus come June.

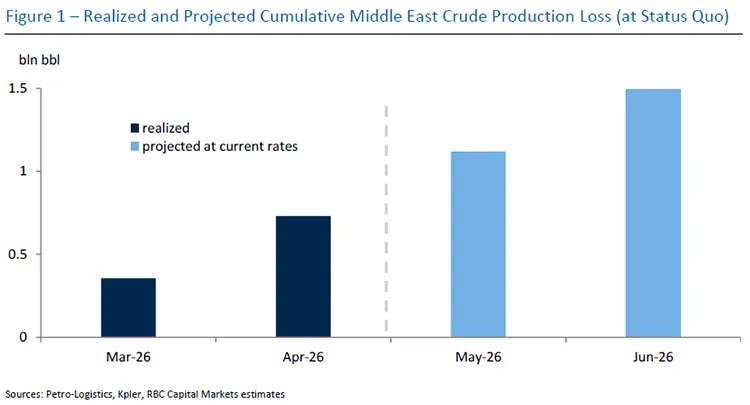

Above all, magical thinking is minimizing the enormous mechanical challenges in restoring flows to pre-February 27 levels, as there is no readily available solution to turn back the clock. Assuming the current crude shut-in rate of 12.5 million barrels per day remains constant, cumulative crude losses will exceed 1 billion barrels by month-end and approach 1.5 billion barrels if the situation remains unchanged through June. Oil prices will likely exceed the Russia-Ukraine highs and close in on the 2008 peak price once summer demand season is in full swing and substantial inventory draws materialize. At that stage, demand destruction will likely be what balances the market.

This bar chart, titled "Figure 1 – Realized and Projected Cumulative Middle East Crude Production Loss (at Status Quo)," illustrates the cumulative loss of crude oil production in the Middle East measured in billion barrels (bln bbl) along the y-axis, spanning from 0 to 1.5. The x-axis represents the timeline from March 2026 to June 2026. A legend distinguishes between "realized" losses, depicted as dark blue bars, and "projected at current rates" losses, shown as light blue bars. The data indicates a realized cumulative loss of approximately 0.35 billion barrels in March 2026, rising to roughly 0.75 billion barrels in April 2026. A vertical dashed line separates the historical data from the projections. The projected cumulative losses continue to climb, reaching an estimated 1.1 billion barrels in May 2026 and 1.5 billion barrels by June 2026. The chart notes its sources as Petro-Logistics, Kpler, and RBC Capital Markets estimates.

Meanwhile, broader geopolitical dynamics further complicate resolution. While headlines from President Trump's Beijing visit indicated Chinese support for reopening the Strait, significant questions remain about how much capital China will actually deploy to resolve the stalemate. Despite the war's ongoing economic costs, it has also served China's strategic interests by compelling Washington to redeploy military assets that would otherwise support Taiwan's defense to the Middle East. Additionally, China has been able to deploy its vast conventional and renewable energy stockpiles to bolster relations with neighbors, further reducing incentives for immediate resolution.

The fundamental reality is that expectations for a near-term, full Hormuz recovery rest on unrealistic assumptions about the ease of resolution and the strategic calculations of all parties involved. The convergence of structural constraints — mechanical challenges in restarting flows, Iranian determination to retain chokepoint control, Western sanctions on the IRGC, and broad geopolitical competition among major powers — suggests that even optimistic scenarios will require far more time and carry substantially greater risks than current market pricing reflects.

Helima Croft authored "Iran Update: Magical Thinking," published on May 14, 2026. For more information on the full report, please contact your RBC representative.