Once again, another pre-market headline based on White House sourcing has sent oil sharply lower. However, it remains far from clear that there is any material movement toward reopening the Strait of Hormuz, or if we are instead stuck in a rebranded "ceasefire with no oil" purgatory for the time being.

The latest "over-soon" messaging comes days after a salvo of Iranian drones and missiles targeted Emirati ships and the UAE's critical Hormuz bypass facility in Fujairah. The fact that the White House was quick to insist that these attacks did not constitute a ceasefire violation may signal that President Trump is still looking to extricate himself from Operation Epic Fury before the official start of summer. But as we have repeatedly stated since the start of the war, it takes two to TACO, and the IRGC is highly unlikely to agree to any deal that does not include a right to enrich uranium.

"Though the regular release of positive headlines about an imminent conflict conclusion is keeping paper prices contained, they are also impeding the curtailment of demand necessary to balance the colossal supply disruption ahead of summer."

Helima Croft, Head of Global Commodity Strategy and MENA Research, RBC Capital Markets

That said, the IRGC may be amenable to concessions on enrichment levels and a possible moratorium on this activity for a period that would conveniently coincide with the time needed to repair the nuclear sites damaged by joint U.S./Israeli airstrikes. Tehran may also continue to resist calls to ship out its stockpiles of highly enriched material, though it has already signaled a willingness to dilute the uranium to levels consistent with a civilian nuclear program. In short, Iran is still seemingly willing to accept something akin to the 2015 nuclear agreement, with the added bonus of Strait of Hormuz operator rights.

Hence, we think the critical variable remains whether Washington is prepared to make concessions on enrichment and the uranium stockpile. Even in the event of a diplomatic breakthrough on the nuclear front, we would anticipate opposition to such a deal from the regional "finish the job" camp and therefore still think there is a risk of a return to active fighting.

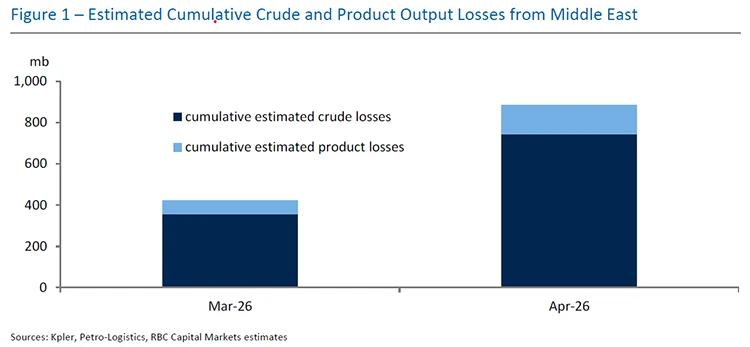

This stacked bar chart, titled "Figure 1 – Estimated Cumulative Crude and Product Output Losses from Middle East," illustrates the volume of lost oil production in million barrels (mb) for March and April 2026. The y-axis ranges from 0 to 1,000 mb. The chart features two categories: cumulative estimated crude losses (dark blue) and cumulative estimated product losses (light blue). In March 2026, total losses reached approximately 420 mb, with crude losses accounting for roughly 350 mb and product losses making up the remainder. By April 2026, total cumulative losses more than doubled to approximately 900 mb, driven by roughly 750 mb in crude losses and 150 mb in product losses. The data is sourced from Kpler, Petro-Logistics, and RBC Capital Markets estimates.

There is also the issue of the U.S. Congress, which continues to exercise a chokehold over the most punitive sanctions. Though the President does have the ability to allow Iran access to its billions of funds blocked in overseas accounts, he cannot vacate congressionally mandated sanctions, which include restrictions on oil sales, the financial sector, and many other pillars of the Iranian economy. In this regard, the Iran sanctions fundamentally differ from those imposed on Russia and Venezuela, which primarily originate in the Executive branch, allowing the White House latitude to repeal those measures. Moreover, as long as the IRGC remains on sanctions lists, it will be exceedingly challenging for any Western shipping company to pay the Tehran toll to ensure safe passage through the Strait of Hormuz.

A corner of the market will undoubtedly view a one-page memorandum to resume negotiations over the next thirty days as significant progress. However, an MoU is unlikely to translate into an immediate resumption of shipping traffic and major production restarts. Instead, our estimates on current outages, if unchanged, would imply another 450 mb of crude and refined products to be lost over that negotiating period.

We continue to call back to the comments about an impending supply reckoning made by the world's leading physical market traders at the FT Commodities Global Summit in Lausanne. Though the regular release of positive headlines about an imminent conflict conclusion is keeping paper prices contained, they are also impeding the curtailment of demand necessary to balance the colossal supply disruption ahead of summer. As the economic fallout spreads from Asia westward, it will likely become more difficult for positive Axios headlines to paper over the unprecedented physical outage.

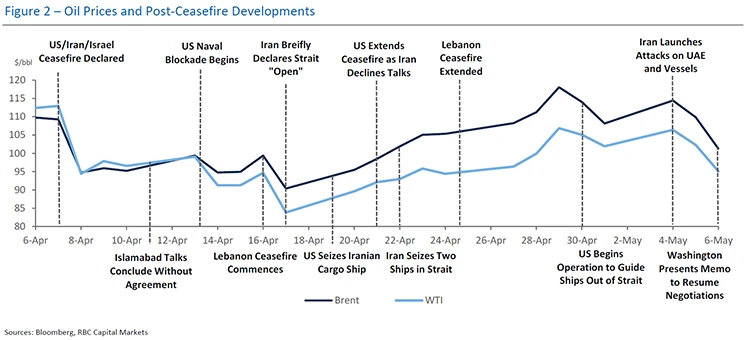

This line chart, titled "Figure 2 – Oil Prices and Post-Ceasefire Developments," tracks the daily prices of Brent (dark blue line) and WTI (light blue line) crude oil in dollars per barrel ($/bbl) from April 6 to May 6. The y-axis ranges from $80 to $120/bbl. The chart overlays significant geopolitical events onto the price trends. Prices initially drop sharply from above $110/bbl following a "US/Iran/Israel Ceasefire Declared" around April 7. Prices hit their lowest point near April 17 (Brent at ~$90/bbl, WTI at ~$84/bbl) when "Iran Briefly Declares Strait 'Open'". Subsequently, prices steadily climb amid escalating tensions, including "US Seizes Iranian Cargo Ship" (April 19) and "Iran Seizes Two Ships in Strait" (April 23). Prices peak around April 29-30 (Brent nearing $118/bbl) as the "US Begins Operation to Guide Ships Out of Strait". Following "Iran Launches Attacks on UAE and Vessels" on May 4, prices begin to decline again. The data is sourced from Bloomberg and RBC Capital Markets.

Helima Croft authored "Iran Update: Like Clockwork," published on May 6, 2026. For more information on the full report, please contact your RBC representative.