Dealmaking in disrupted times

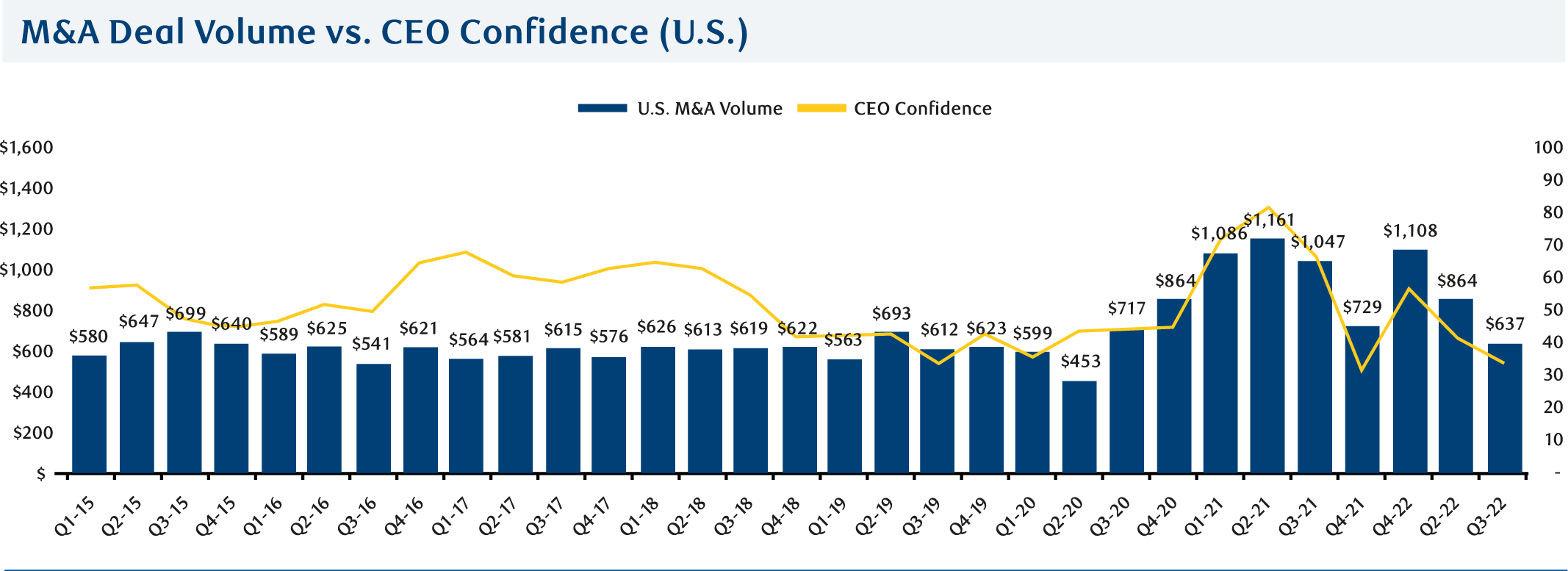

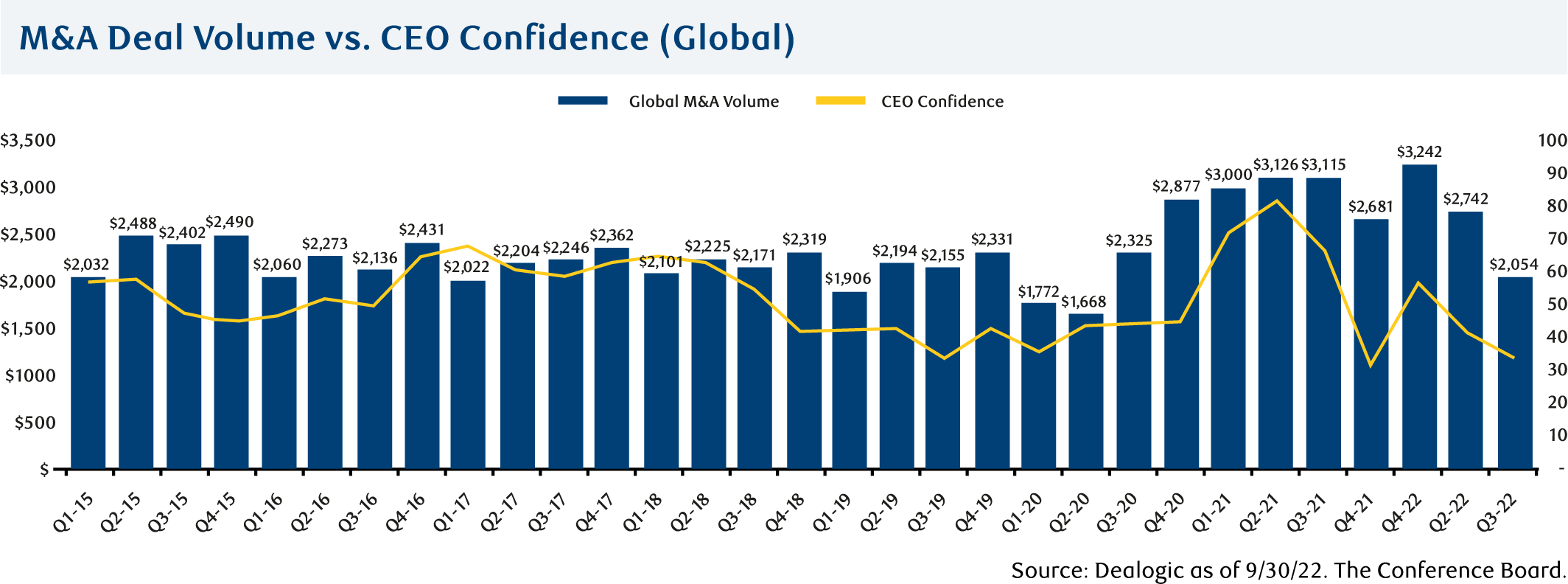

In 2022, geopolitical turmoil, rampant inflation, and rising interest rates all converged to cool the record levels of M&A we saw in 2021. However, despite a marked year-on-year deceleration in M&A activity, 2022 remains, by most standards, a strong year for deal volume and value.

It is easy to lose sight of how resilient activity has actually been compared to previous pre-COVID cycles. But it’s also clear that a year of unprecedented uncertainty weakened executive confidence – a key factor in dealmaking momentum.

With fears of a global recession now weighing heavily on confidence, today’s uncertain landscape will make it difficult for acquirers to confidently predict the profitability of potential targets in 2023, creating a disconnect between buyer and seller valuations that’s causing dealmakers to pause and reflect.

The higher cost of acquisition financing will also continue to make M&A transactions more challenging, pushing buyers that rely on leverage to the sidelines. Conversely, the current environment will also give well-capitalized strategics with solid balance sheets the upper hand.

In 2022, some private equity firms slowed their purchasing activity as access to capital became challenged, interest rates jumped and increased the cost of leveraged finance. However, we expect firms with high levels of dry powder to become more active in 2023 and take advantage of market opportunities that develop.

Dealmakers face an unprecedented number of disruptive forces, but with valuations moderating, those looking to make strategic acquisitions may find better-priced opportunities for growth. Undoubtedly, the operating environment for 2023 will lead to divestitures of noncore assets, as companies look to shore up balance sheets.

The nature of cross-border deals is also changing to reflect geopolitical tensions on the world stage. While cross-border activity decreased in 2022, deals among ‘closely affiliated’ countries increased, signalling a shift to more selective ‘friend-shoring’ transactions in 2023.

“Important windows are going to emerge around financing in the year ahead, and we’re supporting clients now to make sure they're aware of those in advance.”

Ben Mandell

Head of Canadian Mergers and Acquisitions, RBC Capital Markets

On a go-forward basis, we expect higher volumes of smaller transaction sizes for more established companies. A weakening economy should lead more companies to focus on balance sheets, as executives seek to sell or prepare assets for divestiture via corporate carve-outs.

The search for stability and certainty will continue, but despite severe macro headwinds, M&A will continue to be a strategic path forward and volatility could present its own impetus for activity. For many companies, this era of unprecedented disruption will heighten the need for transformational growth to remain both relevant and resilient in today’s fast-changing world.

Navigating the new normal

A return to the record highs of 2021 may not be on the near-term horizon, but 2023 will bring a ‘new normal’ to M&A. Macro volatility should continue to lead dealmakers to take a more cautious approach, particularly given the threat of a recession. But even in the current environment, we see trends that are conducive to deal activity.

Given recent market conditions, now is an opportune moment for dealmakers to redefine how their M&A playbook achieves strategic growth and value. This point is especially true today, given that the current cycle is strongly driven by inflation and interest rate movements, which can have a disproportionate impact on valuations.

The nature and breadth of transaction risks are also changing. The outlook varies depending on sector or region, but we expect M&A transactions to become more complex, more scrutinized, and more specialized. The ‘new normal’ means buyers will take a harder look at potential targets and become more selective in the companies they pursue.

Buyers will also become more creative in terms of how transactions are structured, looking to acquire the right kinds of targets for the right terms. For private company transactions, earnouts will be a useful tool for both buyers and sellers with different views on the future value of the business. Along with contingent consideration, we expect an uptick in equity rollovers, buybacks, continuation funds and partial acquisitions.

Getting the fundamentals of deal execution right is more important than ever. In recent years, boards could expect that an accretive deal would automatically lead to a rise in stock price. Now we’re back to an environment where any acquirer who pays a premium can expect stricter scrutiny.

The rollout of transaction announcements will become critically important. Fundamentally, dealmakers need a stronger thesis behind every acquisition and an airtight rationale to communicate to the market. In less volatile times, there is more leeway in terms of what that investor outreach looks like, but in this environment investors will expect a more compelling narrative.

“The architecture of a transaction and the fundamentals of deal execution will be more important than ever.”

Larry Grafstein

Deputy Chairman, Global Investment Banking, RBC Capital Markets

Extra levels of care will also be taken when looking at how much debt to put in a cash and stock deal, or how much to pay in an all cash deal. More time will be required to complete due diligence on risks, including those related to supply chains and ESG.

It has been a tough equity market for most of 2022. Stock prices have been under pressure, so companies have had to think about buying back stock, not just putting money to work. For many, the macro cycle impacts M&A’s attractiveness versus other uses of capital (although this will apply less to industries where strategic consolidation is necessary for competitive reasons, which will always have its own cycle).

Finally, when the leveraged finance markets do stabilize, we expect to see a snapback in activity among private equity firms, who were unable to invest as much as they would like in 2022. In the current environment, dry powder is harder to put to work. Deals will still be financed, but the quality bar will be higher, and financing is likely to be pricier.

Regulation and activism on the rise

The year ahead will see major shifts in how regulators evaluate M&A transactions. Globally, there are a lot of jurisdictions to appease, which could put a limit on larger deals. Until recently, regulators placed a special focus on the technology sector, but the lens is moving to a broader application which will see more deals challenged across a range of industries and issues.

Regulators are looking beyond strict antitrust issues to also focus on environmental concerns. This trend is unlikely to dissipate as nations pay more attention to issues such as energy security, climate change, critical minerals and resource efficiency. Many of these regulatory pressures have become exacerbated by the war in Ukraine and other geopolitical tensions that have pushed governments to become more inward looking.

For example, in Canada, regulators are is taking a harder line on certain types of transactions, including actions to protect critical minerals. They are restricting foreign state-owned enterprises from acquiring critical mineral companies and have forced the divestiture of some lithium-based companies (important battery metal). If foreign corporates are divesting out of core industries, that creates selling opportunities.

There has always been a degree of regulatory risk to navigate in any deal. But in the current climate, things are going to take longer. Even if you have a very strong position, or a high degree of conviction that a deal should happen now, you must be prepared for certain deals to take longer to complete.

“The very best deals often get done in an environment like this.”

Vito Sperduto

Global Head of M&A, RBC Capital Markets

You might think expanded enforcement of corporate market share offers an advantage to private equity firms. They are often buying multiple companies within a domain, but are not seen to compete against each other directly or reach antitrust market share thresholds. However, it’s clear that regulatory authorities now have private equity in their cross-hairs.

However, there’s an increasing regulatory awareness of the power of dry powder and how private equity-led “roll up” acquisitions in any sector can build market share. Going forward, private equity funds will need to be more thoughtful about the potential regulatory implications of their transactions.

Activists are also getting more involved in M&A decision-making, whether it’s encouraging companies to pursue M&A for value creation or seeking to compel divestiture. In the first three quarters of 2022, the number one commentary by activists or active investors was around M&A. Every quarter, the voice of activists gets progressively louder.

Active fund managers are now using activist techniques, whether it's public or private, to make their views clear to boards. And those active fund investors are under a lot of pressure as it's been very hard to outperform the passive indexes in recent years. Companies have to be cognizant not just of a ubiquitous activist agenda, but of their own shareholders and active fund managers as well.

Conviction is important in M&A and will be tested. If you know you're in a tougher financing environment, with increased regulatory and activist pressure, and you know it is going to take longer to get a deal closed but you still want to proceed with the transaction, that usually means the deal makes sense.