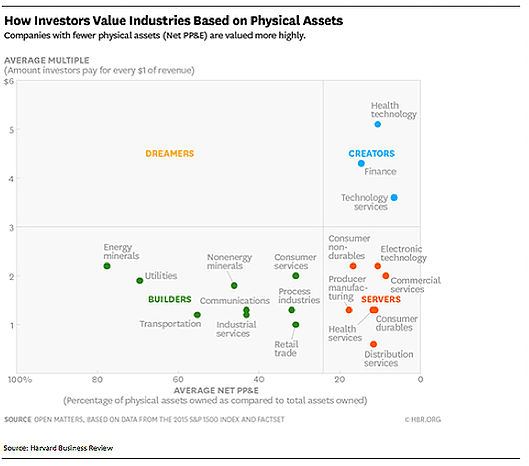

Ownership of physical fixed assets will be more of a liability than a competitive advantage in future. Asset-light models thrive in the ever-increasing digital world and the shared and gig economies.

In the logistics sector, there is a massive disparity in asset overheads between the mature FedEx and well-known disruptor Uber. While FedEx has more than 600 airplanes, and more than 45,000 vehicles, whereas Uber does not own any of its vehicles. FedEx also employs over 300,000 people, whereas Uber has about 6,000 staff. Yet, both companies have similar valuations and market capitalizations of $60–70 billion.

UK-based online-only grocer, Ocado, has no physical stores, runs automated warehouses that do the work of picking the items for online orders, utilizing the cloud, artificial intelligence, robotics, and machine learning. Aside from groceries, including some own-brand/private label items, it also provides sells its technological capability and advantage to competitors such as rival British grocer Morrisons.

In the last decade digital assets have overtaken physical bricks-and-mortar assets in their long-term strategic value. With the advent of Software as a Service (SaaS) and data analytics, original equipment manufacturers and capital equipment customers alike have learned to produce more with less.

Depreciation is much less of an issue and companies are not locked in to entrenched networks of physical assets that act as barriers to rapid and agile change. Both investors and management teams are embracing asset-light business models as a means of generating attractive cash flows with relatively low capex and working capital needs.

Roper Technologies reached a negative working capital milestone in 1Q17 thanks to its prescient and early embrace of SaaS and asset-light businesses. It generates, rather than consumes, cash as it operates.

Faster pace of change will force more companies to provide a portfolio of services rather than merely just selling goods. Pricing the initial equipment sale as a “loss-leader” allows the company to tap into the profitable aftermarket stream of parts, maintenance, and servicing. GE’s aftermarket revenues for its aircraft engines are eight times the initial purchase price of the original equipment sale.

Spotting emerging growth trends and then acquiring businesses with existing strengths in those areas is a route to agility. Software companies – with expertise in predictive analytics and data insights – are popular portfolio additions. Such acquisitions can be a proxy for accelerated research and development (R&D) spending.

Decentralized operating models foster agility by enabling smaller, more entrepreneurial business units to focus on their core strengths. Lean, autonomous operations can adapt much more easily and quickly to new threats and opportunities. This is particularly true of companies where teams operate independently but share a common ideology and operating culture.

Investing in industrial automation will be increasingly necessary but it must be capable of being upgraded as technology evolves. From the initial focus on increasing productivity, control systems and information technologies are now driving improvements in quality, flexibility and safety.