In Budget 2022, the government said the FES would provide details on new clean growth measures, including a green investment tax credit, a $15 billion Canada Growth Fund, and a $1 billion Investment and Innovation Agency. The budget also gave the Canada Infrastructure Bank a mandate adjustment to focus some of its $35 billion in capital on private-led green projects.

Here’s what’s on our minds as we look out to Canada’s green investment into 2023:

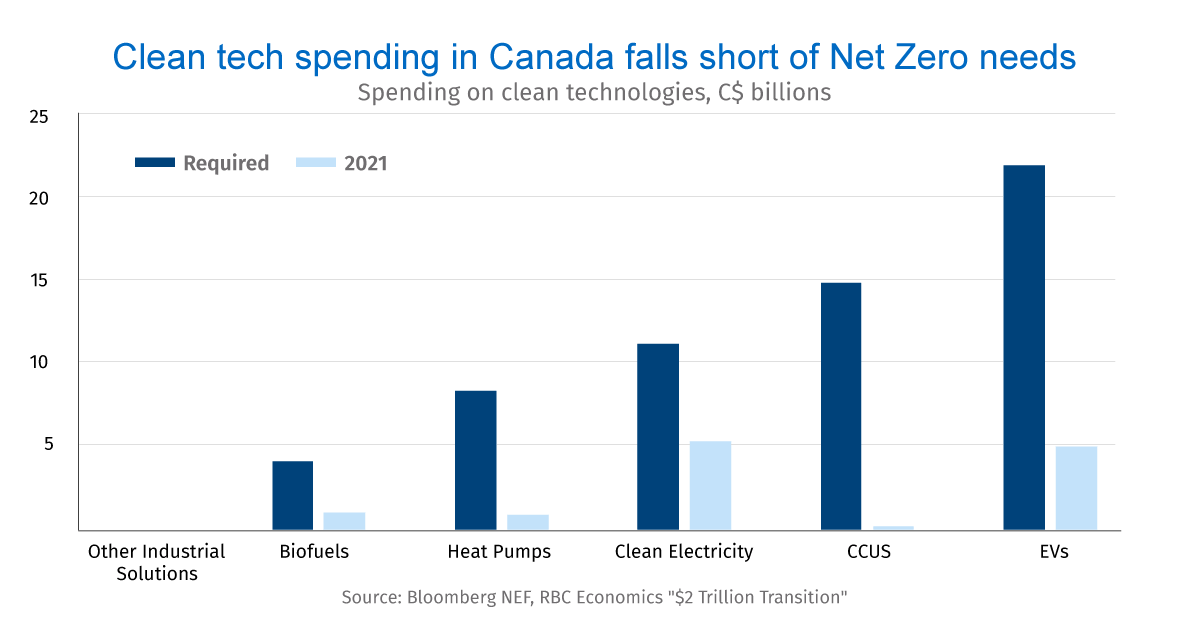

Green investment gaps

- Requirement: Canada needs to invest $2 trillion between now and 2050 to get to Net Zero, or about $80 billion per year.

- Shortfall: At only $10-20 billion per year in current investment, deployment of green technologies needs to rise four to eight times above current levels.

- Where it’s lacking: To meet its 2030 targets, Canada needs to spend about $35 billion per year to 2030, 80% of which is in three sectors: electricity, oil and gas, and transportation. Carbon capture, largely for oil and gas sector emissions, will be one of the most challenging abatement technologies to deploy swiftly given the current policy and economic environment.

- Where it’s needed: Investment must increasingly align with the economy’s abatement pathways. That means more investment in carbon capture, direct air capture, storage, hydrogen, and clean fuel technologies that will increasingly be needed after 2030.

- Venture capital gaps: Technologies still need to be developed for the 25% of emissions that cannot currently be abated, but Canadian venture capital put only 5% of investment toward cleantech companies in 2021 versus 14% globally. And cleantech is particularly underrepresented relative to information technology among active funds focused on early seed or pre-seed funding stages.1

- Green project gaps: Canada is missing sufficient project equity to support the large scale commercialization and deployment of clean technologies, and uncertain project cash flows limit project sponsors’ ability to engage debt markets to improve returns.

Why cleantech is challenging

Four issues continue to be responsible for private capital’s underinvestment in clean technology companies and projects.

- Cleantech projects are capital intensive and involve long payback periods. Risk is high and even when the technology is proven, residual risk emerges around systems integration or reliability in diverse commercial applications.

- Uncertainty about emissions abatement requirements challenges project economics. Canada has forward-looking carbon price regulations and other green incentives to provide some planning assurance for companies looking to cut emissions. But in some cases, these incentives aren’t enough to bridge the investment gap. Moreover, risks remain that carbon prices won’t rise as announced—either because a future government changes course or because immature carbon markets don’t operate as expected.

- Questions remain about whether customers will be willing to pay a so-called “green premium” for Net Zero products and whether a large enough market will materialize for emerging clean technologies, like hydrogen and direct air capture.

- Regulatory uncertainties act as a deterrent to large scale capital investment.

Case study: carbon capture

Technology risk: Carbon capture is a proven technology, but has been less effective with non-concentrated emissions sources. There can also be risks of carbon leakage in sequestration. Most of the capital costs relate to point source capture where there is integration risk with existing systems.

Carbon price uncertainty: Future carbon credit prices can form a significant component of the revenue stream needed to underwrite a major capture project.

Demand risk: Carbon capture could be used in industrial applications like steelmaking or cement, where a high share of the product is exported and differentiated pricing for low-emissions products is niche.

Regulatory risk: Pour space availability, liability for potential escape of sequestered emissions, and environmental assessment or right of way for carbon pipelines are sources of regulatory uncertainty.

IRA: New opportunities and challenges

With $369 billion in broad-based and time-limited incentives, IRA will address key cleantech technology and market risks and improve project economics. While the bill’s provisions face medium-term political risk from the Republicans, it provides enough certainty to spark major U.S. decarbonization investment in the power sector and among other green technologies. Incentives for domestic manufacturing will also help establish U.S.-centric green supply chains.

It’s a big push for climate action, global investment in emerging technologies, and economic opportunities for Canada. Indeed, Canadian cleantech companies will have opportunities to sell their products into the U.S. market and Canada’s proximity to the U.S. improves our potential as a key location for new energy investment in areas like critical minerals. But to rely on U.S. investment to improve green technologies is to risk falling behind on our climate targets. Despite IRA’s size, U.S. public and private investment in key technologies will still only be a fraction of what’s needed globally. And delaying our own decarbonization efforts could render Canadian industry increasingly uncompetitive as the U.S. and Europe steam ahead.

Competition for investment will be most fierce for new energy assets. These include finite hydrogen hubs, critical mineral mines, cleantech company labs and factories, or battery assembly plants that are currently shopping for the best locations to build. The subsidy-based approach engrained in IRA—rather than regulatory incentives—is likely to be a much bigger draw for these firms.

Five actions to accelerate green investment

Canada’s best response to the current environment is to continue to advance decarbonization across economic sectors. Canada already has a core carbon pricing system and almost $15 billion in annual net-zero aligned federal spending.2 To succeed, we’ll need to do even more. This doesn’t mean mimicking the U.S. subsidy-first approach. But Canada’s system can be bolstered in a few areas with more regulatory certainty and a stronger public sector role in addressing clean tech risks and poor project economics.

Here’s how:

1.Address carbon pricing uncertainty through carbon contracts for differences

Canada should make carbon contracts for differences (CCfD) a focus of the Canada Growth Fund. In these bilateral contracts, the government would compensate project sponsor counterparties when carbon prices deviate from those announced. This would help commit the government to taking the actions necessary to uphold carbon prices that support projects. The Netherlands leads the world in employing CCfDs, with a budget of €13 billion in 2022.

CCfDs are not without challenges. Some elements of carbon pricing are easier for the government to control, like raising the fuel charge rate at which heavy emitters can purchase carbon credits from the government. Others may involve greater tradeoffs. Raising the market-set carbon credit price for heavy emitters for instance, could involve imposing stronger performance standards across sectors—including those less prepared to meet them. If governments can’t follow through on actions to raise carbon prices, fiscal liability of CCfDs could be significant. These risks can be limited by focusing on the fuel charge risk the government controls, partial coverage of carbon credit prices, providing greater support to strategic projects or more uneconomic technologies, or providing shorter term contracts until 2030 to bridge to the development of better carbon markets. As sophisticated financial contracts to structure and price, the government will need to move quickly to be able to execute contracts in time for private investment to flow into emissions reductions for 2030.

The federal government can further boost the regulatory system by finalizing regulations like the Clean Electricity Standard, methane regulations, the oil and gas cap, and the heavy emitters’ system review. There should also be concerted efforts to address permitting and other regulatory hurdles to project development, in conjunction with provinces.

2.New tools to address technology and market risks

Technology risk is deterring investors from taking on large-scale projects involving technologies like carbon capture, direct air capture, or hydrogen. What’s needed is an entity to provide guarantees that the engineering, procurement, and construction of these technologies work as planned. This is a common feature in project finance, where the risk allocation helps to both draw in debt investors and improve project returns. The Canada Growth Fund should address this risk, which is too large for most entities to self-insure against. In the U.S., the Department of Energy’s Loan Programs Office provides this type of commercialization support through loans and guarantees, and was given an expanded funding envelope in IRA.

Market risk can be dealt with through offtake agreements, where a customer agrees to take a certain amount of product at a set price for a period of time. Major corporate entities are looking to secure stable supplies of critical minerals, clean hydrogen, or other materials, but may be challenged to fully bear the risks or they may have insufficient regulatory incentive to do so. Government is needed to help bridge the gap and speed the development of enabling infrastructure and technologies enabling critical minerals supply and clean hydrogen production to further decarbonize a range of sectors.

3.More tax-based support for maturing technologies

Major investment is needed now to promote innovation post-2030 to improve technologies and commercial models for decarbonizing hard-to-abate sectors. The government should make it an explicit focus for the Canada Growth Fund (CGF) and Canada Infrastructure Bank (CIB) to support innovative or first-of-their-kind projects in strategic sectors.

Tax-based incentives like the cleantech investment tax credit are equally important. When proven technologies are at an earlier commercialization phase and winning models are unknown, the tax system engages as many private actors and approaches as possible. They’ll be faster and broader-based compared to concessionary finance tools like CGF or CIB, which can complement tax incentives by covering additional project risks in strategic sectors. Concessionary finance tools should emphasize transparency so they can operate like tax tools in firming market expectations, such as around future prevailing carbon prices or market development.

4.Encouraging the provinces to step up

The provinces have an equally important role to play as taxing authorities and direct beneficiaries of their competitive industrial sectors. Yet provinces have been looking to the federal taxpayer to take the lead in decarbonization or for green industrial policy. For instance, the federal taxpayer is being called upon by Nova Scotia and New Brunswick to meet regulations ending coal use in the power sector, Alberta for carbon capture incentives to meet the oil and gas emissions cap, Ontario for development of a battery supply chain, or Newfoundland and Labrador to encourage east coast green hydrogen production. Federal incentives should smooth disparate decarbonization burdens, but provinces need to step up with their own incentives or revenue models and play a larger role in supporting industrial policy projects.

Federal incentives should encourage explicit provincial matching funds and get further traction for advancing regional economic tables. An overarching federal-provincial dialogue should advance discussions around coordinated and politically-saleable approaches to consumer and industry-pay models for decarbonization investment.

5.Strategic prioritization

With so many areas for investment, the federal government will need to prioritize. A key choice is between decarbonizing existing production and pursuing production opportunities in the new energy systems. The first could run the risk of spending too much money to decarbonize early in sectors that could have a diminished role in the future, such as fossil-fuel based industries. The second is a bet on an uncertain energy future: investments in an export-driven sector that may facilitate decarbonization globally at the cost of the Canadian taxpayer, or that doesn’t result in direct cuts in Canadian emissions or long-term economic benefits.

The federal government will need to support the private sector in decarbonizing the current energy system while also building a new one. But it will need to be clear-eyed in pursuing focused industrial policy opportunities, while supporting broad-based decarbonization strategies. Decarbonization investment can advance economic opportunities and Canada’s primary objective: to meet the emissions targets necessary to avoid climate catastrophe. The government should articulate an overarching strategy, with more specific policy objectives across the suite of government policy tools, including programs, procurement, and regulation.

1 https://www.bdc.ca/globalassets/digizuite/36181-report-canada-venture-capital-landscape-2022.pdf

2 Net-zero-Report_102022.pdf (chamber.ca)

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.