Financial Markets Monthly - August 2021

Advanced economies generally continued to regain their footing with July reports showing a strong increase in growth and improving labour market conditions. Elevated vaccination rates and falling case counts saw the US, UK, parts of Europe and, more recently, Canada reopen broader swaths of their economies. Low interest rates and government stimulus, with more in the pipeline from the US, underpin forecasts that conditions will normalize in the latter part of 2021 and improve further in 2022. That said, a surge of Delta variant cases in the US and UK reignited worries that the return to normal may not be smooth. Government bond yields across the major markets we cover drifted lower in July as investors weighed the odds of another round of virus-related disruption, though the bond rally lost steam in early-August.

Second quarter increases in GDP in the US, UK and euro area were impressive with the US recovering all its pandemic-related losses while the latter two aren’t expected to do so until the fourth quarter. Canada’s economy lagged its peers in the second quarter as lockdowns remained in place however June’s rebound as the reopening began sets up for strong third quarter. Central banks are staying the course with only the BoC tapering their asset purchases although others are expected to start later this year. Rate increases however are unlikely in 2021 as policymakers give the economy and labour markets time to fully recover. Further, central banks remain confident that the recent jump in inflation—a product of base year ef-fects, supply chain disruptions and reopening pressures—will prove temporary allaying the need for aggressive action.

While the Delta variant increases the downside risk to our forecasts, we expect that elevated vaccination rates in most advanced economies will limit the scope of future lockdown measures allowing the economic recovery to continue. In its July update, the IMF retained its forecast for the global economy to expand by 6% this year and marked up its 2022 growth forecast to 4.9%. Prospects for advanced economies improved in both years reflecting high rates of vaccination and increased US government stimulus. Conversely, low vaccination rates will keep emerging market economies under pressure.

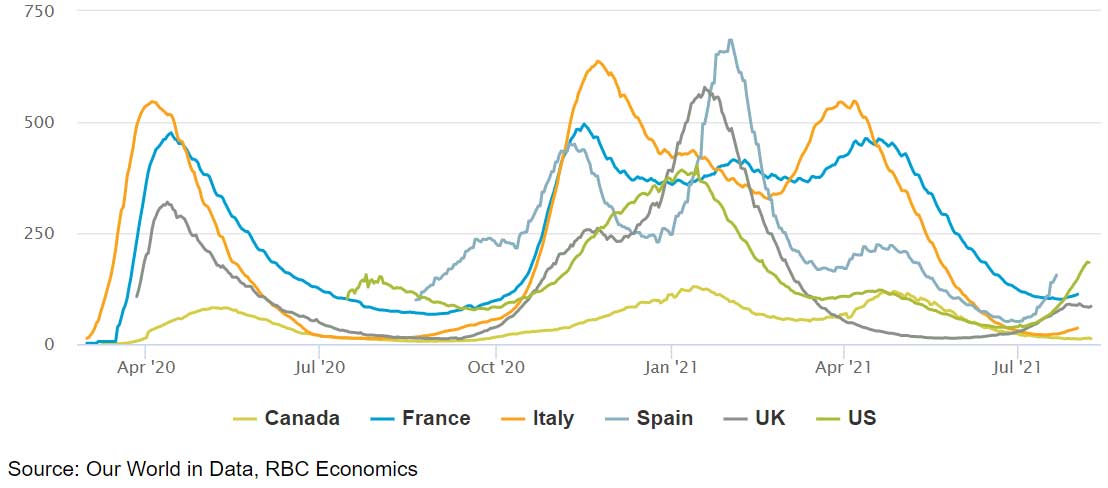

Some countries seeing a renewed increase in hospitalizations

COVID-related hospitalizations per million population

Highlights:

- The US’s vaccine rollout has slowed and the Delta variant is gaining ground, pushing hospitalizations higher. A number of European countries are also seeing accelerating case growth and an uptick in hospitalizations. But unlike Australia (where vaccination rates are much lower) authorities aren’t re-instating lockdown measures.

- A strong consumer sector helped US GDP return to its pre-pandemic level in Q2. Job gains are picking up but the employment shortfall relative to pre-pandemic remains sizeable. Notwithstanding Delta risks, we think the Fed will see enough progress toward its objectives in September to signal a forthcoming QE taper.

- The BoC continues to gradually taper its bond buying and should switch to re-investment only as of next year. Canada’s Q2 GDP growth was slower than in other advanced economies but looks set to pick up in Q3.

- With economic activity picking up, the BoE is more confident that the UK labour can absorb the end of the government’s furlough program at the end of September. Assuming a relatively modest increase in unemployment through year end, we now see the BoE raising rates in May and November 2022.

- We don’t see the ECB or RBA raising interest rates in our forecast horizon. The former will re-evaluate its pandemic-era QE program in September while the latter is primed for another round of QE, albeit at a slightly slower pace than currently.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.